As per Intent Market Research, the Optical Satellite Market was valued at USD 142.6 Billion in 2024-e and will surpass USD 285.2 Billion by 2030; growing at a CAGR of 12.2% during 2025-2030.

The optical satellite market is experiencing robust growth as advancements in satellite technologies and increasing demand for high-resolution imagery drive adoption across various applications. Optical satellites, equipped with advanced imaging systems, offer superior image quality, real-time data collection, and precision, making them indispensable for applications in earth observation, surveillance, communication, and scientific research. The market is further fueled by the rising adoption of optical satellite technologies in commercial, defense, and governmental sectors. As the cost of satellite manufacturing decreases and launches become more accessible, the adoption of microsatellites, minisatellites, and nanosatellites has accelerated, expanding the overall optical satellite market.

Governments and private players worldwide are investing heavily in optical satellite technologies to support climate monitoring, urban planning, disaster management, and national security. Innovations in satellite design, miniaturization, and optical systems are expected to play a significant role in shaping the market’s future.

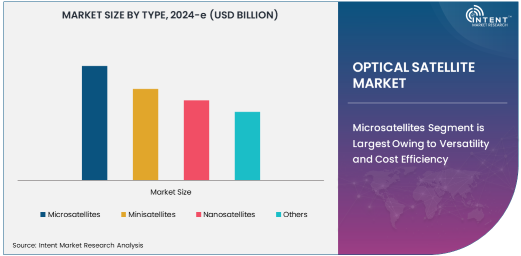

Microsatellites Segment is Largest Owing to Versatility and Cost Efficiency

The microsatellites segment dominates the optical satellite market due to its versatility and cost efficiency. Microsatellites, typically weighing between 10 kg and 100 kg, offer an optimal balance between functionality and affordability, making them ideal for a wide range of applications such as earth observation, communication, and scientific research. These satellites are particularly valuable in scenarios requiring a constellation of satellites for global coverage or continuous monitoring.

The growing demand for real-time data for environmental monitoring, disaster management, and urban development has significantly boosted the deployment of microsatellites. Additionally, advancements in satellite technology have enabled the development of high-performance microsatellites capable of capturing high-resolution imagery and processing data efficiently. The cost-effectiveness of microsatellite manufacturing and deployment, combined with their increasing functionality, ensures their continued dominance in the market.

Communication Application is Fastest Growing Owing to Rising Demand for Global Connectivity

The communication application segment is the fastest-growing area within the optical satellite market, driven by the increasing need for global connectivity. Optical satellites play a crucial role in providing high-speed, reliable communication services, particularly in remote and underserved regions. With the expansion of satellite-based internet services and the rise of IoT-enabled devices, the demand for optical satellites in communication has grown exponentially.

Moreover, optical satellites offer significant advantages, such as reduced latency and enhanced bandwidth, over traditional radio frequency communication systems. These benefits are particularly appealing for sectors like maritime, aviation, and military communication, where reliability and speed are paramount. The continued development of satellite constellations, such as Starlink and OneWeb, further fuels growth in this segment, as these initiatives aim to provide seamless internet connectivity worldwide.

Defense & Intelligence End-User Segment is Largest Owing to Security and Surveillance Needs

The defense and intelligence segment represents the largest end-user group in the optical satellite market, driven by the critical need for real-time surveillance, reconnaissance, and secure communication. Optical satellites are widely used for monitoring border areas, tracking troop movements, and collecting intelligence on potential threats. Their ability to provide high-resolution imagery and near-real-time updates makes them indispensable tools for defense and intelligence agencies.

The increasing geopolitical tensions and rising investments in military modernization have further propelled the adoption of optical satellites in defense applications. Governments worldwide are prioritizing the deployment of advanced optical satellite systems to enhance their intelligence-gathering and strategic decision-making capabilities. The ongoing advancements in optical imaging technology, such as improved resolution and night vision capabilities, continue to strengthen the appeal of optical satellites in the defense and intelligence sector.

North America is Largest Region Owing to Strong Infrastructure and Investment

North America is the largest region in the optical satellite market, supported by the presence of leading space agencies like NASA and private players such as SpaceX and Planet Labs. The region benefits from a well-established satellite manufacturing and launch infrastructure, coupled with significant investments in space technology. The U.S. government’s focus on expanding space-based defense capabilities and enhancing climate monitoring systems further drives growth in the North American optical satellite market.

The commercial sector in North America has also seen rapid growth, with companies deploying satellite constellations for applications like global communication and earth observation. The region's strong R&D ecosystem, coupled with supportive government policies, ensures that North America remains at the forefront of optical satellite technology innovation.

Competitive Landscape and Key Players

The optical satellite market is highly competitive, with key players including Airbus, Lockheed Martin, Maxar Technologies, Planet Labs, and Thales Alenia Space. These companies are focusing on technological innovation, strategic partnerships, and expanding their portfolios to maintain a competitive edge.

Emerging players and startups are also entering the market, leveraging advancements in miniaturization and optical imaging technologies to develop cost-effective and high-performance satellites. As competition intensifies, companies are prioritizing R&D to enhance the capabilities of optical satellites, including improving resolution, reducing latency, and increasing operational lifespans. The competitive landscape is further shaped by collaborations between government agencies and private firms, which continue to drive innovation and market expansion.

Recent Developments:

- Airbus SE launched a new high-resolution optical satellite designed for Earth observation and environmental monitoring.

- Planet Labs PBC introduced advanced imaging technologies for their nanosatellite constellation, enhancing data acquisition for agriculture and urban planning.

- Lockheed Martin Corporation secured a contract to develop optical payloads for next-generation reconnaissance satellites.

- Maxar Technologies unveiled a new optical satellite designed for communication and Earth observation, featuring enhanced payload capacity.

- ICEYE expanded its satellite constellation with an optical imaging system for disaster management and infrastructure monitoring.

List of Leading Companies:

- Airbus SE

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- The Boeing Company

- Thales Alenia Space

- L3Harris Technologies, Inc.

- OHB SE

- Ball Aerospace & Technologies Corp.

- Maxar Technologies

- Surrey Satellite Technology Limited

- Planet Labs PBC

- Rocket Lab USA, Inc.

- Capella Space

- ICEYE

- Spire Global, Inc.

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 142.6 Billion |

|

Forecasted Value (2030) |

USD 285.2 Billion |

|

CAGR (2025 – 2030) |

12.2% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Optical Satellite Market By Type (Microsatellites, Minisatellites, Nanosatellites), By Application (Earth Observation, Communication, Surveillance & Reconnaissance, Scientific Research, Navigation), and By End-User (Commercial, Defense & Intelligence, Government & Civil) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Airbus SE, Lockheed Martin Corporation, Northrop Grumman Corporation, The Boeing Company, Thales Alenia Space, L3Harris Technologies, Inc., OHB SE, Ball Aerospace & Technologies Corp., Maxar Technologies, Surrey Satellite Technology Limited, Planet Labs PBC, Rocket Lab USA, Inc., Capella Space, ICEYE, Spire Global, Inc. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Optical Satellite Market, by Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Microsatellites |

|

4.2. Minisatellites |

|

4.3. Nanosatellites |

|

4.4. Others |

|

5. Optical Satellite Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Earth Observation |

|

5.2. Communication |

|

5.3. Surveillance & Reconnaissance |

|

5.4. Scientific Research |

|

5.5. Navigation |

|

5.6. Others |

|

6. Optical Satellite Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Commercial |

|

6.2. Defense & Intelligence |

|

6.3. Government & Civil |

|

6.4. Others |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Optical Satellite Market, by Type |

|

7.2.7. North America Optical Satellite Market, by Application |

|

7.2.8. North America Optical Satellite Market, by End-User |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Optical Satellite Market, by Type |

|

7.2.9.1.2. US Optical Satellite Market, by Application |

|

7.2.9.1.3. US Optical Satellite Market, by End-User |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Airbus SE |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Lockheed Martin Corporation |

|

9.3. Northrop Grumman Corporation |

|

9.4. The Boeing Company |

|

9.5. Thales Alenia Space |

|

9.6. L3Harris Technologies, Inc. |

|

9.7. OHB SE |

|

9.8. Ball Aerospace & Technologies Corp. |

|

9.9. Maxar Technologies |

|

9.10. Surrey Satellite Technology Limited |

|

9.11. Planet Labs PBC |

|

9.12. Rocket Lab USA, Inc. |

|

9.13. Capella Space |

|

9.14. ICEYE |

|

9.15. Spire Global, Inc. |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Optical Satellite Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Optical Satellite Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Optical Satellite Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA