As per Intent Market Research, the Ophthalmic Viscoelastic Devices Market was valued at USD 0.7 billion in 2024-e and will surpass USD 1.2 billion by 2030; growing at a CAGR of 9.3% during 2025 - 2030.

The ophthalmic viscoelastic devices market is experiencing notable growth as a result of advancements in surgical techniques, increased demand for cataract surgeries, and innovations in viscoelastic formulations that improve surgical outcomes. Viscoelastic devices, which are used to maintain the anterior chamber of the eye during surgery, are critical in procedures such as cataract, glaucoma, and retina surgeries. These devices help in protecting delicate ocular tissues, facilitating easier lens insertion, and minimizing intraoperative complications. With growing surgical volumes, especially cataract surgeries due to the aging population, the demand for ophthalmic viscoelastic devices is poised to rise.

Ophthalmic viscoelastic devices are essential in ensuring the success of ocular surgeries by creating a stable environment within the eye during procedures. These devices, which include a variety of products such as Healon, Viscoat, and Ocucoat, offer a wide range of viscosities and characteristics to meet the needs of different surgical techniques. The continued innovation in viscoelastic technologies, such as the development of new formulations and biodegradable solutions, is expected to further fuel market growth. As eye surgeries become more advanced, with a shift towards minimally invasive approaches, the role of these devices in enhancing surgical precision and improving recovery times will continue to expand.

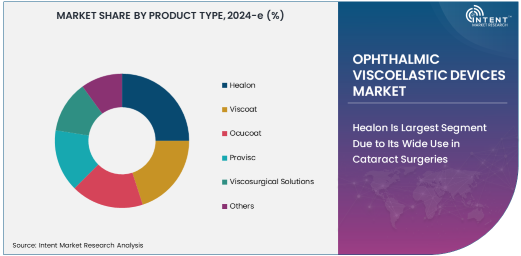

Healon Is Largest Segment Due to Its Wide Use in Cataract Surgeries

Healon, a widely used ophthalmic viscoelastic device, holds the largest share of the market due to its extensive application in cataract surgeries. This viscoelastic is favored for its ability to provide optimal support during lens insertion, reduce trauma to ocular tissues, and facilitate clear visibility during surgery. Healon's effectiveness in stabilizing the anterior chamber of the eye has made it a preferred choice among ophthalmic surgeons, particularly in cataract procedures, which are among the most common surgeries performed worldwide. As cataract surgeries continue to rise, particularly with the growing elderly population, the demand for Healon is expected to remain strong.

Healon is also known for its biocompatibility and ease of use during surgeries, making it a versatile product in a variety of ophthalmic procedures beyond cataract surgeries. Its formulation helps in maintaining the shape and stability of the eye during surgery while protecting the delicate endothelial cells from trauma. These attributes have contributed to Healon’s dominant position in the ophthalmic viscoelastic devices market and will likely sustain its leadership as the demand for cataract surgeries continues to grow.

Oculoplastic Surgery Drives Growth in Ophthalmic Viscoelastic Devices Market

Oculoplastic surgery is one of the fastest-growing applications in the ophthalmic viscoelastic devices market, as these procedures are increasingly performed to correct or reconstruct the eye and surrounding structures. The use of viscoelastic devices in oculoplastic surgeries has become more common as they help surgeons maintain optimal eye shape, protect delicate tissues, and prevent complications during reconstructive procedures. With advancements in cosmetic and reconstructive ophthalmic surgery, viscoelastic devices have proven to be invaluable in enhancing surgical precision and ensuring better outcomes for patients undergoing these procedures.

The rise in demand for oculoplastic surgeries, driven by both medical necessity and cosmetic considerations, has led to increased utilization of viscoelastic solutions like Healon and Viscoat, which are suitable for use in these delicate surgeries. As awareness and availability of these procedures increase, especially in developed regions, oculoplastic surgeries are expected to continue driving demand for ophthalmic viscoelastic devices. Surgeons increasingly rely on these devices to facilitate easier manipulation of tissues and improve overall surgical efficacy.

Hospitals Are Largest End-User Segment Due to High Surgical Volume

Hospitals remain the largest end-user segment in the ophthalmic viscoelastic devices market due to their central role in conducting a high volume of eye surgeries. Hospitals, particularly those with dedicated ophthalmic departments, routinely perform complex surgeries, such as cataract and glaucoma surgeries, that require the use of ophthalmic viscoelastic devices to ensure optimal surgical conditions. The growing number of surgical procedures, combined with the increasing adoption of advanced surgical techniques, continues to drive the demand for these devices in hospital settings.

Hospitals are typically equipped with state-of-the-art surgical equipment and devices, including ophthalmic viscoelastic solutions, to provide high-quality care for patients undergoing eye surgeries. Given the high volume of cataract surgeries and other ophthalmic procedures performed in hospitals, this segment is expected to maintain its dominant share in the market. Furthermore, the increasing trend toward improving surgical outcomes and minimizing recovery times has reinforced the importance of viscoelastic devices in hospital-based ophthalmic surgeries.

Ophthalmic Viscoelastic Devices Used Across Various Applications

Ophthalmic viscoelastic devices are used across a wide range of applications, including cataract surgery, glaucoma surgery, retina surgery, and oculoplastic surgery. These devices play a critical role in maintaining the eye's structure during surgery, protecting ocular tissues, and ensuring clear visibility for the surgeon. In cataract surgeries, for example, viscoelastic solutions such as Healon and Viscoat are used to stabilize the anterior chamber, making it easier to insert the intraocular lens and minimizing the risk of complications.

In addition to cataract surgery, these devices are also used in glaucoma and retina surgeries, where their ability to protect delicate tissues and facilitate surgical precision is crucial. The role of viscoelastic devices in oculoplastic surgeries has also expanded, as these procedures increasingly rely on these solutions for reconstructing and repairing the eye and its surrounding structures. As the demand for advanced ophthalmic surgical procedures continues to grow, the use of viscoelastic devices will continue to expand across these various applications.

North America Is Largest Region Due to Advanced Healthcare Infrastructure

North America holds the largest share of the ophthalmic viscoelastic devices market, driven by its well-established healthcare infrastructure, high levels of technological adoption, and a significant number of eye surgeries performed annually. The United States, in particular, leads the region with its large aging population and high demand for cataract surgeries, which require the use of viscoelastic devices for optimal outcomes. Additionally, North America benefits from advanced medical technologies and a high number of skilled surgeons, which together create an ideal environment for the widespread adoption of ophthalmic viscoelastic devices.

The region also boasts strong reimbursement policies, facilitating the adoption of high-quality ophthalmic devices, including viscoelastic solutions, in both hospital and clinical settings. As the number of eye surgeries continues to increase, particularly in the elderly population, North America is expected to retain its position as the largest market for ophthalmic viscoelastic devices.

Leading Companies and Competitive Landscape

The ophthalmic viscoelastic devices market is highly competitive, with leading companies such as AbbVie (maker of Healon), Johnson & Johnson Vision (Viscoat), and Bausch + Lomb (Ocucoat) at the forefront. These companies are prominent players, offering a range of ophthalmic viscoelastic products that cater to different types of eye surgeries. Their focus on innovation and the development of new formulations has strengthened their market presence, with companies constantly seeking to improve the performance, safety, and biocompatibility of their products.

The competitive landscape is marked by continuous product innovation, with companies investing in research and development to introduce new viscoelastic solutions that meet the evolving needs of ophthalmic surgeons. Strategic collaborations, acquisitions, and the expansion of product portfolios are common strategies employed by market leaders to strengthen their competitive position. As the demand for ophthalmic surgeries continues to rise, the competition within the ophthalmic viscoelastic devices market is expected to intensify, leading to further advancements in product offerings and a wider range of surgical applications.

Recent Developments:

- In December 2024, Alcon Inc. introduced a new line of viscoelastic solutions designed to provide better corneal protection during cataract surgeries.

- In November 2024, Bausch + Lomb launched an upgraded version of its Healon product with improved stability and biocompatibility for more effective ocular surgeries.

- In October 2024, Johnson & Johnson Vision announced the release of a new viscoelastic device tailored for glaucoma surgeries, offering better control during procedures.

- In September 2024, Carl Zeiss Meditec AG expanded its portfolio by introducing an advanced viscoelastic material for retinal surgeries, providing enhanced precision and safety.

- In August 2024, Oculus Surgical Inc. developed a new viscoelastic solution designed to reduce post-operative complications and enhance surgical outcomes in cataract surgeries.

List of Leading Companies:

- Alcon Inc.

- Bausch + Lomb

- Johnson & Johnson Vision

- Carl Zeiss Meditec AG

- Oculus Surgical Inc.

- Abbott Laboratories

- Medtronic

- Katalyst Surgical Inc.

- FCI Ophthalmics

- Rayner Intraocular Lenses Ltd.

- Santen Pharmaceutical Co., Ltd.

- Eyepoint Pharmaceuticals

- Hoya Corporation

- LensCrafters

- Hanita Lenses

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 0.7 billion |

|

Forecasted Value (2030) |

USD 1.2 billion |

|

CAGR (2025 – 2030) |

9.3% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Ophthalmic Viscoelastic Devices Market By Product Type (Healon, Viscoat, Ocucoat, Provisc, Viscosurgical Solutions), By Application (Cataract Surgery, Glaucoma Surgery, Retina Surgery, Oculoplastic Surgery, Corneal Surgery), By End-User (Hospitals, Ophthalmic Clinics, Eye Centers) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Alcon Inc., Bausch + Lomb, Johnson & Johnson Vision, Carl Zeiss Meditec AG, Oculus Surgical Inc., Abbott Laboratories, Medtronic, Katalyst Surgical Inc., FCI Ophthalmics, Rayner Intraocular Lenses Ltd., Santen Pharmaceutical Co., Ltd., Eyepoint Pharmaceuticals, Hoya Corporation, LensCrafters, Hanita Lenses |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Ophthalmic Viscoelastic Devices Market, by Product Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Healon |

|

4.2. Viscoat |

|

4.3. Ocucoat |

|

4.4. Provisc |

|

4.5. Viscosurgical Solutions |

|

4.6. Others |

|

5. Ophthalmic Viscoelastic Devices Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Cataract Surgery |

|

5.2. Glaucoma Surgery |

|

5.3. Retina Surgery |

|

5.4. Oculoplastic Surgery |

|

5.5. Corneal Surgery |

|

5.6. Others |

|

6. Ophthalmic Viscoelastic Devices Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Hospitals |

|

6.2. Ophthalmic Clinics |

|

6.3. Eye Centers |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Ophthalmic Viscoelastic Devices Market, by Product Type |

|

7.2.7. North America Ophthalmic Viscoelastic Devices Market, by Application |

|

7.2.8. North America Ophthalmic Viscoelastic Devices Market, by End-User |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Ophthalmic Viscoelastic Devices Market, by Product Type |

|

7.2.9.1.2. US Ophthalmic Viscoelastic Devices Market, by Application |

|

7.2.9.1.3. US Ophthalmic Viscoelastic Devices Market, by End-User |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Alcon Inc. |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Bausch + Lomb |

|

9.3. Johnson & Johnson Vision |

|

9.4. Carl Zeiss Meditec AG |

|

9.5. Oculus Surgical Inc. |

|

9.6. Abbott Laboratories |

|

9.7. Medtronic |

|

9.8. Katalyst Surgical Inc. |

|

9.9. FCI Ophthalmics |

|

9.10. Rayner Intraocular Lenses Ltd. |

|

9.11. Santen Pharmaceutical Co., Ltd. |

|

9.12. Eyepoint Pharmaceuticals |

|

9.13. Hoya Corporation |

|

9.14. LensCrafters |

|

9.15. Hanita Lenses |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Ophthalmic Viscoelastic Devices Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Ophthalmic Viscoelastic Devices Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Ophthalmic Viscoelastic Devices Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA