As per Intent Market Research, the Onshore Wind Energy Market was valued at USD 67.6 Billion in 2024-e and will surpass USD 133.8 Billion by 2030; growing at a CAGR of 12.0% during 2025-2030.

The onshore wind energy market is experiencing rapid growth as the global shift towards renewable energy sources intensifies. Wind energy, particularly from onshore wind farms, has emerged as a key player in the transition to a low-carbon economy. Onshore wind turbines are widely deployed across regions with strong wind resources, providing a cost-effective and sustainable energy solution for both developed and developing economies. The ongoing drive for energy independence, reduced carbon emissions, and long-term sustainability has led to increased investments in onshore wind energy projects, supported by favorable government policies, tax incentives, and renewable energy targets.

Technological advancements, cost reductions in wind turbine production, and improved efficiency of wind farms have further fueled the growth of the onshore wind energy market. As governments, businesses, and consumers alike seek greener alternatives to traditional energy sources, onshore wind energy continues to play a crucial role in global energy strategies. With the integration of digital technologies such as predictive maintenance and real-time monitoring, the onshore wind energy sector is expected to see significant innovations, improving both energy generation capacity and operational efficiencies.

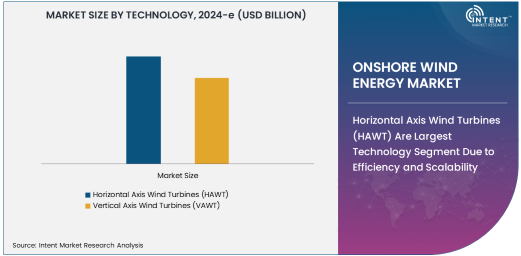

Horizontal Axis Wind Turbines (HAWT) Are Largest Technology Segment Due to Efficiency and Scalability

Horizontal Axis Wind Turbines (HAWT) dominate the onshore wind energy market due to their superior efficiency and scalability. HAWTs are the most commonly used type of wind turbine globally, with their three-blade design and ability to capture wind from any direction making them ideal for large-scale energy generation. These turbines are highly efficient, capable of generating more electricity at lower wind speeds compared to other types of turbines, making them particularly suitable for the diverse wind conditions found in onshore locations. The widespread adoption of HAWTs is a result of their robust performance, high energy output, and established technological maturity.

HAWTs are especially favored for utility-scale wind farms and independent power producer (IPP) projects, where large-scale energy production is required. Their design allows for a high level of customization, enabling turbines to be tailored to specific geographic conditions. As onshore wind farms continue to expand, the market for HAWTs is expected to grow even further, driven by advancements in turbine technology, larger blade sizes, and enhanced aerodynamic designs that increase power output and efficiency.

Wind Turbines Are Largest Component Segment Due to Core Role in Energy Generation

In the onshore wind energy market, wind turbines represent the largest component segment, as they are the primary technology used to convert wind energy into electricity. A wind turbine consists of several key components, including the blades, tower, generator, and control system, all of which work together to harness wind energy efficiently. The turbine’s size, capacity, and design play a crucial role in determining the overall energy production capacity of a wind farm. As such, wind turbines are the foundational component in any onshore wind energy project.

The demand for wind turbines continues to increase as countries and companies invest heavily in wind energy infrastructure to meet renewable energy targets. Additionally, turbine manufacturers are focusing on producing more efficient, cost-effective, and durable turbines, with innovations such as larger rotor diameters and higher hub heights contributing to the increased energy generation capabilities of modern turbines. As the market continues to expand, wind turbines will remain at the core of the onshore wind energy sector, powering the transition to renewable energy.

Utilities Are Largest End-User Industry Due to Large-Scale Deployment and Energy Production

Utilities are the largest end-user industry in the onshore wind energy market, owing to the large-scale deployment of wind farms for electricity generation. Utility companies invest in onshore wind energy projects to diversify their energy portfolios, reduce reliance on fossil fuels, and meet government-mandated renewable energy targets. The scale of investment and infrastructure required to build wind farms aligns with the capabilities of utility companies, which have the resources to fund and manage large renewable energy projects. Additionally, utilities are well-positioned to integrate wind energy into the existing grid infrastructure, facilitating the efficient distribution of generated power.

The ongoing global push for clean energy and decarbonization is further accelerating the demand for onshore wind energy from utilities. Many countries are adopting policies that require a significant increase in the share of renewable energy within their national grids, driving utilities to invest in renewable sources such as wind. As utility-scale projects grow in size and complexity, utilities are expected to continue to dominate the end-user industry, shaping the future of onshore wind energy.

Greenfield Projects Are Largest Installation Segment Due to New Capacity Expansion

Greenfield projects represent the largest installation segment in the onshore wind energy market, as they involve the development of entirely new wind farms in areas with strong wind resources. Greenfield projects are typically located in rural or remote regions where land is available for large-scale wind farms. The development of greenfield projects is often driven by the need to expand renewable energy capacity, particularly in regions where wind energy potential has been identified but remains underutilized. As the demand for clean energy continues to rise, the construction of new wind farms through greenfield projects is crucial for meeting long-term energy goals.

Greenfield projects often benefit from government incentives, such as subsidies and tax breaks, designed to promote the construction of new renewable energy infrastructure. These projects are also attractive to independent power producers (IPPs) and utilities looking to build new generation capacity. While greenfield projects require substantial upfront investment, they provide the opportunity to develop modern, large-scale wind farms with the latest turbine technologies, ensuring a high level of efficiency and long-term energy production. As the demand for renewable energy grows, the number of greenfield projects in the onshore wind energy market is expected to increase significantly.

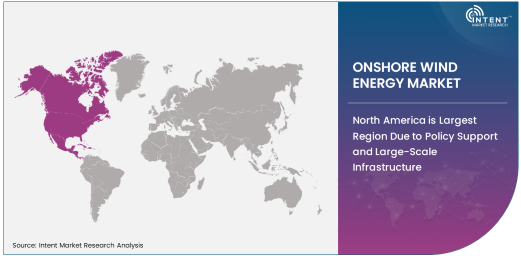

North America is Largest Region Due to Policy Support and Large-Scale Infrastructure

North America is the largest region in the onshore wind energy market, driven by strong policy support for renewable energy, particularly in the United States. The U.S. has been a leader in the development of onshore wind energy, with several states such as Texas, Iowa, and Oklahoma boasting large-scale wind farms that contribute a significant share of the country’s renewable energy output. The expansion of wind energy is supported by federal and state-level incentives, including the Production Tax Credit (PTC), which has significantly lowered the cost of wind power and encouraged further investments in wind farms.

In addition to favorable policies, North America benefits from abundant wind resources, particularly in the central U.S. and Canada, where vast, flat landscapes are ideal for large-scale wind farm development. The growing demand for clean, renewable energy to replace fossil fuels and meet emission reduction targets further supports the region's dominance in the onshore wind energy market. As the renewable energy transition accelerates globally, North America is expected to maintain its position as a leading region for onshore wind energy development.

Leading Companies and Competitive Landscape

The onshore wind energy market is competitive, with several major players operating in the space, including Vestas Wind Systems, Siemens Gamesa Renewable Energy, GE Renewable Energy, and Nordex SE. These companies are leaders in the design, manufacturing, and installation of wind turbines, and they compete based on technology, efficiency, and cost-effectiveness. The market is also characterized by innovation, as companies work to develop larger, more efficient turbines with higher capacity factors to drive down the cost of energy generation.

In addition to turbine manufacturers, developers and operators of wind farms, such as NextEra Energy and Iberdrola, play a significant role in the competitive landscape. These companies are involved in the construction, operation, and maintenance of wind farms, helping to bring renewable energy projects to fruition. The competitive landscape in the onshore wind energy market is expected to continue evolving, with advancements in turbine technology and increased investment in global wind energy infrastructure driving market growth.

Recent Developments:

- In December 2024, Vestas Wind Systems A/S announced the completion of a new onshore wind farm in the U.S. with a capacity of 500 MW.

- In November 2024, GE Renewable Energy signed a deal with a European utility to install 150 MW of onshore wind power capacity.

- In October 2024, Siemens Gamesa Renewable Energy revealed its new wind turbine model with enhanced efficiency for onshore applications.

- In September 2024, Nordex SE secured a contract to supply turbines for a large-scale wind project in India.

- In August 2024, Suzlon Energy Ltd. completed a 200 MW wind power project in the Indian subcontinent.

List of Leading Companies:

- Siemens Gamesa Renewable Energy

- GE Renewable Energy

- Nordex SE

- Vestas Wind Systems A/S

- Suzlon Energy Ltd.

- Senvion S.A.

- Goldwind

- Envision Energy

- Ming Yang Smart Energy Group

- Siemens AG

- Nordex Acciona

- Suzlon

- Enercon GmbH

- Shanghai Electric Wind Power Group

- Bergey Windpower Co.

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 67.6 Billion |

|

Forecasted Value (2030) |

USD 133.8 Billion |

|

CAGR (2025 – 2030) |

12.0% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Onshore Wind Energy Market by Technology (Horizontal Axis Wind Turbines (HAWT), Vertical Axis Wind Turbines (VAWT)), Component (Wind Turbines, Blades, Towers, Generators, Control Systems), End-User Industry (Utilities, Independent Power Producers (IPPs), Commercial & Industrial Buildings, Residential), Installation (Greenfield Projects, Repowering Projects) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Siemens Gamesa Renewable Energy, GE Renewable Energy, Nordex SE, Vestas Wind Systems A/S, Suzlon Energy Ltd., Senvion S.A., Goldwind, Envision Energy, Ming Yang Smart Energy Group, Siemens AG, Nordex Acciona, Suzlon, Enercon GmbH, Shanghai Electric Wind Power Group, Bergey Windpower Co. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Onshore Wind Energy Market, by Technology (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Horizontal Axis Wind Turbines (HAWT) |

|

4.2. Vertical Axis Wind Turbines (VAWT) |

|

5. Onshore Wind Energy Market, by Component (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Wind Turbines |

|

5.2. Blades |

|

5.3. Towers |

|

5.4. Generators |

|

5.5. Control Systems |

|

6. Onshore Wind Energy Market, by End-User Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Utilities |

|

6.2. Independent Power Producers (IPPs) |

|

6.3. Commercial & Industrial Buildings |

|

6.4. Residential |

|

7. Onshore Wind Energy Market, by Installation (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Greenfield Projects |

|

7.2. Repowering Projects |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Onshore Wind Energy Market, by Technology |

|

8.2.7. North America Onshore Wind Energy Market, by Component |

|

8.2.8. North America Onshore Wind Energy Market, by End-User Industry |

|

8.2.9. North America Onshore Wind Energy Market, by Installation |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Onshore Wind Energy Market, by Technology |

|

8.2.10.1.2. US Onshore Wind Energy Market, by Component |

|

8.2.10.1.3. US Onshore Wind Energy Market, by End-User Industry |

|

8.2.10.1.4. US Onshore Wind Energy Market, by Installation |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Siemens Gamesa Renewable Energy |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. GE Renewable Energy |

|

10.3. Nordex SE |

|

10.4. Vestas Wind Systems A/S |

|

10.5. Suzlon Energy Ltd. |

|

10.6. Senvion S.A. |

|

10.7. Goldwind |

|

10.8. Envision Energy |

|

10.9. Ming Yang Smart Energy Group |

|

10.10. Siemens AG |

|

10.11. Nordex Acciona |

|

10.12. Suzlon |

|

10.13. Enercon GmbH |

|

10.14. Shanghai Electric Wind Power Group |

|

10.15. Bergey Windpower Co. |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Onshore Wind Energy Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Onshore Wind Energy Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Onshore Wind Energy Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA