As per Intent Market Research, the Oncology Molecular Diagnostics Market was valued at USD 5.2 billion in 2024-e and will surpass USD 11.2 billion by 2030; growing at a CAGR of 13.8% during 2025 - 2030.

The oncology molecular diagnostics market is experiencing significant growth, driven by the rising prevalence of cancer and the increasing demand for personalized medicine. This market involves the use of advanced molecular technologies to diagnose, monitor, and treat cancer, enabling more precise and effective therapies. Key segments within the market include consumables, technologies like Next-Generation Sequencing (NGS) and PCR, applications in cancer screening and companion diagnostics, and end-users such as hospitals and diagnostic laboratories. Among these, consumables and companion diagnostics are the largest segments, with NGS emerging as the fastest-growing technology due to its ability to provide detailed genetic profiling for targeted treatments. North America leads the market, owing to its advanced healthcare infrastructure, high adoption of molecular diagnostic technologies, and strong regulatory support. Key players, including Roche Diagnostics, Thermo Fisher Scientific, and Abbott Laboratories, dominate the market with continuous innovation, strategic acquisitions, and partnerships to drive growth. As personalized medicine becomes increasingly prevalent, the oncology molecular diagnostics market is poised for continued expansion, offering advanced diagnostic solutions for cancer care.

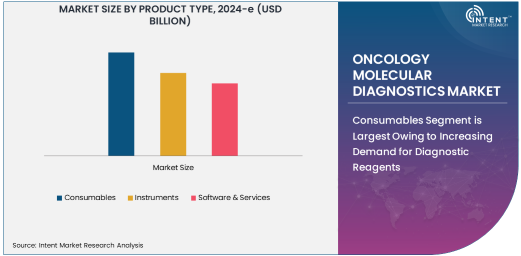

Consumables Segment is Largest Owing to Increasing Demand for Diagnostic Reagents

The oncology molecular diagnostics market has witnessed significant growth driven by advancements in personalized medicine, increasing cancer prevalence, and the rising demand for early-stage cancer detection. Among the various product types, consumables have emerged as the largest segment within this market. Consumables, which include diagnostic reagents, test kits, and other single-use products, are essential for performing molecular tests. The growing prevalence of cancer worldwide and the increasing adoption of molecular diagnostics in clinical settings are key factors contributing to the dominance of this segment.

The demand for consumables is fueled by the high frequency of testing required for diagnosing and monitoring cancer progression, especially in companion diagnostics. These consumables are critical for conducting accurate molecular tests, which provide insights into genetic mutations and tumor markers. As a result, hospitals, diagnostic laboratories, and research centers rely heavily on consumables to meet the growing demand for cancer diagnostics and treatment monitoring. The increasing focus on personalized cancer treatment, which requires frequent testing for specific biomarkers, further boosts the consumables segment’s market share.

Next-Generation Sequencing (NGS) Technology is Fastest Growing Due to Precision in Cancer Diagnosis

The technology segment of oncology molecular diagnostics is experiencing rapid advancements, with Next-Generation Sequencing (NGS) emerging as the fastest-growing technology. NGS enables high-throughput sequencing of DNA and RNA, making it an invaluable tool for identifying genetic mutations and alterations associated with cancer. This technology allows for comprehensive genetic profiling of tumors, facilitating the development of personalized cancer therapies tailored to individual patients. NGS offers a high level of accuracy and precision, which is why it is increasingly being adopted in both research and clinical settings.

The ability of NGS to simultaneously analyze multiple genes and detect mutations that may not be picked up by traditional methods such as PCR has made it a preferred choice for cancer diagnosis and treatment. Additionally, NGS is integral to the growing field of liquid biopsy, allowing for non-invasive cancer detection and monitoring. The decreasing cost of sequencing and the increasing availability of NGS platforms have contributed to its rapid adoption, further driving its growth in the oncology molecular diagnostics market.

Companion Diagnostics Application is Largest Due to Its Role in Personalized Medicine

Among various applications, companion diagnostics is the largest segment in the oncology molecular diagnostics market, primarily due to its crucial role in personalized cancer treatment. Companion diagnostics involves the use of molecular tests to identify specific biomarkers in cancer patients, enabling clinicians to choose the most appropriate treatment based on the genetic characteristics of the tumor. This application is integral to the growing trend of precision medicine, where treatments are tailored to individual patients for improved efficacy and reduced side effects.

The increasing prevalence of cancer and the rising demand for targeted therapies have driven the need for companion diagnostics. Pharmaceutical companies are increasingly relying on companion diagnostics to develop drugs that are tailored to specific genetic profiles, which has led to regulatory approvals for several targeted cancer therapies. The use of companion diagnostics is not only improving treatment outcomes but also reducing healthcare costs by minimizing trial-and-error approaches in cancer treatment.

Hospitals End-User Segment is Largest Due to High Volume of Cancer Diagnoses

The hospitals segment is the largest end-user in the oncology molecular diagnostics market, primarily driven by the high volume of cancer diagnoses and treatments conducted in hospital settings. Hospitals are the primary healthcare institutions where most cancer patients are diagnosed, staged, and treated. With the increasing number of cancer cases globally and the shift towards personalized medicine, hospitals are investing significantly in advanced diagnostic technologies to provide accurate and timely cancer diagnoses.

Hospitals also offer specialized treatment and monitoring services, which require advanced molecular diagnostics for identifying genetic mutations and determining appropriate therapies. Furthermore, the integration of molecular diagnostics into clinical pathways has enabled hospitals to offer better outcomes for cancer patients, positioning hospitals as the largest end-user segment in the oncology molecular diagnostics market.

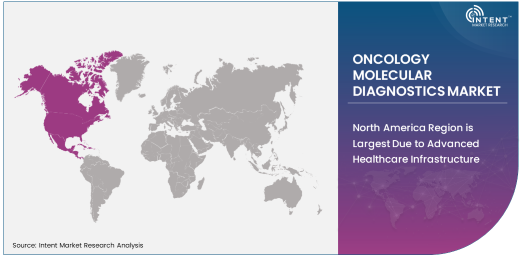

North America Region is Largest Due to Advanced Healthcare Infrastructure

North America dominates the oncology molecular diagnostics market, primarily due to its advanced healthcare infrastructure, high adoption of cutting-edge diagnostic technologies, and substantial healthcare investments. The United States, in particular, is a global leader in the adoption of molecular diagnostics, driven by the availability of advanced technologies, well-established healthcare providers, and a large patient pool. Additionally, the high prevalence of cancer in the region and the emphasis on early diagnosis and personalized treatment further contribute to North America’s market leadership.

The region also benefits from robust regulatory support for oncology diagnostics, with the FDA providing fast-track approval processes for innovative diagnostic technologies. The increasing demand for next-generation sequencing and companion diagnostics in clinical settings, particularly for personalized medicine, has further fueled the growth of the oncology molecular diagnostics market in North America. Moreover, the presence of leading molecular diagnostic companies and a well-established reimbursement system has bolstered the region's dominance.

Competitive Landscape and Leading Companies

The oncology molecular diagnostics market is highly competitive, with several prominent players leading the market through continuous innovation and strategic partnerships. Key companies like Roche Diagnostics, Thermo Fisher Scientific, and Abbott Laboratories are at the forefront, offering a wide range of products and services for molecular cancer diagnosis and treatment monitoring. These companies invest heavily in research and development to introduce advanced diagnostic technologies like NGS, PCR, and liquid biopsy solutions.

In addition to established leaders, several emerging players are focusing on niche applications of molecular diagnostics, such as genetic profiling and personalized cancer care, creating a dynamic and competitive market environment. Strategic acquisitions, collaborations, and partnerships are common as companies aim to expand their portfolios and enhance their competitive positions. The ongoing innovation in molecular diagnostic platforms, combined with the increasing focus on precision medicine, is expected to drive further growth and competition in the oncology molecular diagnostics market.

Recent Developments:

- Roche Diagnostics launched its Cobas EGFR Mutation Test v2 in 2024 to detect mutations associated with non-small cell lung cancer (NSCLC) for better-targeted therapy.

- Thermo Fisher Scientific announced its acquisition of The Binding Site Group in 2024, expanding its molecular diagnostics portfolio, especially for oncology and immunology.

- Illumina, Inc. received FDA approval in 2023 for its TruSight Oncology 500 test, a comprehensive next-generation sequencing panel for detecting key cancer mutations.

- Abbott Laboratories launched the Alinity m Molecular Diagnostics System in 2023, a new platform for oncology diagnostics that provides faster results with higher precision.

- Qiagen N.V. acquired NeuMoDx Molecular, Inc. in 2023, strengthening its position in oncology molecular diagnostics with innovative PCR-based solutions.

List of Leading Companies:

- Roche Diagnostics

- Thermo Fisher Scientific

- Abbott Laboratories

- Qiagen N.V.

- Agilent Technologies

- Illumina, Inc.

- Bio-Rad Laboratories, Inc.

- Siemens Healthineers

- GE Healthcare

- Cepheid, Inc.

- Hologic, Inc.

- Foundation Medicine, Inc.

- Sysmex Corporation

- Becton, Dickinson and Company (BD)

- PerkinElmer, Inc.

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 5.2 Billion |

|

Forecasted Value (2030) |

USD 11.2 Billion |

|

CAGR (2025 – 2030) |

13.8% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Oncology Molecular Diagnostics Market By Product Type (Consumables, Instruments, Software & Services), By Technology (PCR, Next-Generation Sequencing, In Situ Hybridization, Fluorescence In Situ Hybridization, Microarrays), By Application (Cancer Screening, Companion Diagnostics, Genetic Profiling, Prognostics, Monitoring & Treatment), By End-User Industry (Hospitals, Diagnostic Laboratories, Academic and Research Institutes, Cancer Research Centers) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Roche Diagnostics, Thermo Fisher Scientific, Abbott Laboratories, Qiagen N.V., Agilent Technologies, Illumina, Inc., Bio-Rad Laboratories, Inc., Siemens Healthineers, GE Healthcare, Cepheid, Inc., Hologic, Inc., Foundation Medicine, Inc., Sysmex Corporation, Becton, Dickinson and Company (BD), PerkinElmer, Inc. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Oncology Molecular Diagnostics Market, by Product Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Consumables |

|

4.2. Instruments |

|

4.3. Software & Services |

|

5. Oncology Molecular Diagnostics Market, by Technology (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. PCR (Polymerase Chain Reaction) |

|

5.2. Next-Generation Sequencing (NGS) |

|

5.3. In Situ Hybridization (ISH) |

|

5.4. Fluorescence In Situ Hybridization (FISH) |

|

5.5. Microarrays |

|

6. Oncology Molecular Diagnostics Market, by Application (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Cancer Screening |

|

6.2. Companion Diagnostics |

|

6.3. Genetic Profiling |

|

6.4. Prognostics |

|

6.5. Monitoring & Treatment |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Oncology Molecular Diagnostics Market, by Product Type |

|

7.2.7. North America Oncology Molecular Diagnostics Market, by Technology |

|

7.2.8. North America Oncology Molecular Diagnostics Market, by Application |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Oncology Molecular Diagnostics Market, by Product Type |

|

7.2.9.1.2. US Oncology Molecular Diagnostics Market, by Technology |

|

7.2.9.1.3. US Oncology Molecular Diagnostics Market, by Application |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Roche Diagnostics |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Thermo Fisher Scientific |

|

9.3. Abbott Laboratories |

|

9.4. Qiagen N.V. |

|

9.5. Agilent Technologies |

|

9.6. Illumina, Inc. |

|

9.7. Bio-Rad Laboratories, Inc. |

|

9.8. Siemens Healthineers |

|

9.9. GE Healthcare |

|

9.10. Cepheid, Inc. |

|

9.11. Hologic, Inc. |

|

9.12. Foundation Medicine, Inc. |

|

9.13. Sysmex Corporation |

|

9.14. Becton, Dickinson and Company (BD) |

|

9.15. PerkinElmer, Inc. |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Oncology Molecular Diagnostics Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Oncology Molecular Diagnostics Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Oncology Molecular Diagnostics Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA