As per Intent Market Research, the Nasal Lacrimal Stent Market was valued at USD 1.1 Billion in 2024-e and will surpass USD 1.9 Billion by 2030; growing at a CAGR of 9.8% during 2025 - 2030.

The nasal lacrimal stent market is gaining traction due to the increasing prevalence of nasolacrimal duct obstructions and the rising awareness about minimally invasive treatment options for such conditions. Nasal lacrimal stents are used in ophthalmic and otolaryngologic procedures to treat blocked tear ducts, allowing for proper drainage of tears. These devices are designed to maintain the patency of the nasolacrimal duct following surgery or in patients with chronic duct obstruction, improving patient outcomes and minimizing the risk of infection or complications. The growing aging population and a higher incidence of lacrimal duct-related disorders are contributing to the market's expansion.

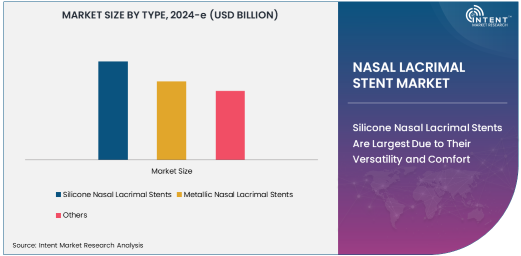

Silicone Nasal Lacrimal Stents Are Largest Due to Their Versatility and Comfort

Silicone nasal lacrimal stents are the largest segment in the nasal lacrimal stent market, owing to their flexibility, biocompatibility, and ease of use. Silicone stents are commonly chosen for the treatment of nasolacrimal duct obstructions and for post-surgical care because they are soft and conform easily to the anatomical shape of the nasal passage. Additionally, silicone stents are less likely to cause irritation, making them more comfortable for long-term use compared to other materials.

The versatility of silicone nasal lacrimal stents is another factor contributing to their dominance in the market. They can be customized in terms of size and shape to suit individual patient needs, further increasing their preference among ophthalmologists and otolaryngologists. As the demand for minimally invasive and effective solutions for tear duct obstructions continues to grow, silicone nasal lacrimal stents are expected to remain the dominant choice in the market.

Treatment of Nasolacrimal Duct Obstruction Is Largest Application Due to High Incidence of Blockages

The treatment of nasolacrimal duct obstruction is the largest application segment in the nasal lacrimal stent market. Nasolacrimal duct obstruction is a common condition that can lead to excessive tearing, pain, and recurrent infections if left untreated. The increasing prevalence of this condition, especially among the elderly population, drives the demand for nasal lacrimal stents used in surgical procedures to unblock or bypass the tear duct.

Patients who suffer from nasolacrimal duct obstruction often require stents as part of the post-operative care to ensure proper drainage and prevent recurrence. The use of nasal lacrimal stents in treating this condition is effective in maintaining the duct's patency and reducing complications such as tear accumulation and chronic infections. As the awareness and diagnosis of this condition increase, the treatment of nasolacrimal duct obstruction is expected to continue being the largest application segment in the market.

Hospitals and Clinics End-Use Industry Is Largest Due to High Patient Volume and Specialized Care

The hospitals and clinics segment is the largest end-use industry for nasal lacrimal stents, driven by the high volume of patients requiring surgical treatment for nasolacrimal duct obstructions. Hospitals and clinics have the necessary infrastructure and specialized healthcare professionals, such as ophthalmologists and otolaryngologists, to perform the procedures that require the insertion of nasal lacrimal stents. These institutions also play a significant role in post-operative care, where stents are frequently used to ensure the successful outcome of tear duct surgeries.

Hospitals and clinics are the primary settings where patients with nasolacrimal duct obstructions are diagnosed and treated. Given the high number of procedures conducted in these settings, hospitals and clinics continue to represent the largest share of the market for nasal lacrimal stents. Furthermore, with the increasing number of specialized eye and ENT surgeries performed annually, this end-use industry is expected to maintain its dominant role in the market.

North America Leads the Market Owing to Advanced Healthcare Infrastructure

North America holds the largest market share in the nasal lacrimal stent market, primarily due to the region’s advanced healthcare infrastructure, high adoption of advanced medical technologies, and the presence of leading medical device manufacturers. The United States, in particular, is at the forefront of market growth, with numerous hospitals and clinics offering state-of-the-art ophthalmic and otolaryngologic treatments, including the use of nasal lacrimal stents.

The growing aging population and increased incidence of lacrimal duct disorders in North America further contribute to the demand for nasal lacrimal stents. Additionally, the region’s well-established healthcare system, along with continuous innovation in medical devices, positions North America as a leader in the nasal lacrimal stent market. The availability of specialized medical professionals and treatment options also adds to the region's dominance in the market.

Leading Companies and Competitive Landscape

The nasal lacrimal stent market is characterized by the presence of a few key players who focus on innovation, product development, and maintaining high standards of patient care. Notable companies operating in this market include Medtronic, Cook Medical, Stryker, and Teleflex, among others. These companies are engaged in the development and distribution of a wide range of nasal lacrimal stents made from different materials such as silicone, metal, and others.

The competitive landscape of the nasal lacrimal stent market is dynamic, with companies focusing on advancing product offerings by improving biocompatibility, durability, and ease of use. Strategic collaborations and acquisitions are common as companies seek to expand their product portfolios and gain market share. With the increasing demand for minimally invasive surgical solutions and advancements in stent materials, the market is expected to witness further growth and innovation in the coming years.

Recent Developments:

- Kaneka Corporation launched a next-generation bicanalicular stent with enhanced flexibility and durability.

- FCI Ophthalmics introduced a monocanalicular stent optimized for pediatric patients with nasolacrimal duct obstruction.

- Cook Medical expanded its product portfolio by acquiring a patented lacrimal stent design technology.

- Medtronic announced the development of biodegradable stents for short-term tear duct obstruction treatments.

- Boston Scientific Corporation revealed plans for a joint venture to produce advanced lacrimal and ENT stents.

List of Leading Companies:

- Stryker Corporation

- CooperVision, Inc.

- Smith & Nephew plc

- Medtronic PLC

- Bausch Health Companies Inc.

- Abbott Laboratories

- Thermo Fisher Scientific Inc.

- Johnson & Johnson Vision Care, Inc.

- Integra LifeSciences Holdings Corporation

- Hoya Corporation

- KARL STORZ SE & Co. KG

- Richard Wolf GmbH

- KLS Martin Group

- Surgiwear

- Beaver-Visitec International, Inc.

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 1.1 Billion |

|

Forecasted Value (2030) |

USD 1.9 Billion |

|

CAGR (2025 – 2030) |

9.8% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Nasal Lacrimal Stent Market by Type (Silicone Nasal Lacrimal Stents, Metallic Nasal Lacrimal Stents), Application (Treatment of Nasolacrimal Duct Obstruction, Post-Surgical Care for Lacrimal Duct Procedure), End-Use Industry (Hospitals and Clinics, Ambulatory Surgical Centers, Research and Academic Institutions) and Regions |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Stryker Corporation, CooperVision, Inc., Smith & Nephew plc, Medtronic PLC, Bausch Health Companies Inc., Abbott Laboratories, Johnson & Johnson Vision Care, Inc., Integra LifeSciences Holdings Corporation, Hoya Corporation, KARL STORZ SE & Co. KG, Richard Wolf GmbH, KLS Martin Group, Beaver-Visitec International, Inc. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Nasal Lacrimal Stent Market, by Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Silicone Nasal Lacrimal Stents |

|

4.2. Metallic Nasal Lacrimal Stents |

|

4.3. Others |

|

5. Nasal Lacrimal Stent Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Treatment of Nasolacrimal Duct Obstruction |

|

5.2. Post-Surgical Care for Lacrimal Duct Procedure |

|

6. Nasal Lacrimal Stent Market, by End-Use (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Hospitals and Clinics |

|

6.2. Ambulatory Surgical Centers |

|

6.3. Research and Academic Institutions |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Nasal Lacrimal Stent Market, by Type |

|

7.2.7. North America Nasal Lacrimal Stent Market, by Application |

|

7.2.8. North America Nasal Lacrimal Stent Market, by End-Use |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Nasal Lacrimal Stent Market, by Type |

|

7.2.9.1.2. US Nasal Lacrimal Stent Market, by Application |

|

7.2.9.1.3. US Nasal Lacrimal Stent Market, by End-Use |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Stryker Corporation |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. CooperVision, Inc. |

|

9.3. Smith & Nephew plc |

|

9.4. Medtronic PLC |

|

9.5. Bausch Health Companies Inc. |

|

9.6. Abbott Laboratories |

|

9.7. Thermo Fisher Scientific Inc. |

|

9.8. Johnson & Johnson Vision Care, Inc. |

|

9.9. Integra LifeSciences Holdings Corporation |

|

9.10. Hoya Corporation |

|

9.11. KARL STORZ SE & Co. KG |

|

9.12. Richard Wolf GmbH |

|

9.13. KLS Martin Group |

|

9.14. Surgiwear |

|

9.15. Beaver-Visitec International, Inc. |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Nasal Lacrimal Stent Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Nasal Lacrimal Stent Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Nasal Lacrimal Stent Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA