As per Intent Market Research, the Muscular Dystrophy Treatment Market was valued at USD 3.6 billion in 2024-e and will surpass USD 6.0 billion by 2030; growing at a CAGR of 8.9% during 2025 - 2030.

The muscular dystrophy treatment market is gaining traction due to the increasing prevalence of various forms of muscular dystrophy and advancements in therapeutic approaches. Muscular dystrophy encompasses a group of genetic disorders characterized by progressive muscle weakness and degeneration, with Duchenne Muscular Dystrophy (DMD) being the most common and severe type. The development of innovative treatments, such as gene therapies and antisense oligonucleotides (AON), is driving significant growth in this market. These therapies aim to address the underlying genetic causes of muscular dystrophy, providing hope for improved patient outcomes. Additionally, the rising investments in research and development and supportive government initiatives further fuel market growth.

With the advent of muscle regeneration therapies and advanced steroid medications, there has been an increase in treatment options tailored to different disease types. Hospitals and clinics are the primary end-users, providing specialized care and access to cutting-edge therapies. However, the demand for home-based care is also on the rise, driven by patient preferences for convenient treatment options and the availability of portable medical equipment. The muscular dystrophy treatment market is poised for growth as novel therapies receive regulatory approvals and enter the commercial landscape.

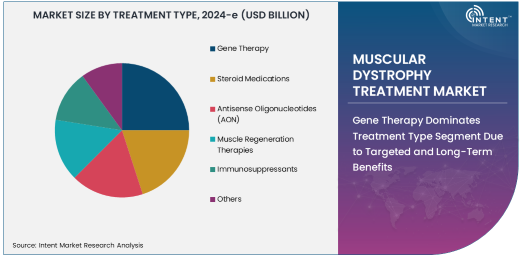

Gene Therapy Dominates Treatment Type Segment Due to Targeted and Long-Term Benefits

Gene therapy is the dominant segment in the muscular dystrophy treatment market, offering targeted and potentially long-term solutions for managing the disease. Unlike traditional therapies that address symptoms, gene therapy targets the genetic root cause of muscular dystrophy by introducing functional genes or modifying defective ones. Recent advancements in gene-editing technologies, such as CRISPR-Cas9, have opened new avenues for developing effective gene therapies tailored to specific types of muscular dystrophy, particularly DMD and BMD.

The success of clinical trials and increasing regulatory approvals for gene therapy products have solidified their position as a leading treatment option. These therapies have demonstrated significant improvements in muscle function and quality of life for patients, making them a preferred choice among healthcare providers. The growing number of partnerships between biotechnology companies and research institutions further accelerates the development and accessibility of gene therapies, ensuring their continued dominance in the treatment type segment.

Duchenne Muscular Dystrophy (DMD) Is Largest Disease Type Segment Due to High Prevalence and Severity

Duchenne Muscular Dystrophy (DMD) is the largest disease type segment in the muscular dystrophy treatment market, primarily due to its high prevalence and severe clinical manifestations. DMD is an X-linked genetic disorder that predominantly affects males, leading to progressive muscle degeneration and loss of mobility. The significant unmet medical need associated with DMD has spurred extensive research efforts and investments in developing innovative therapies, including gene therapy, antisense oligonucleotides, and muscle regeneration approaches.

The rising awareness of DMD and the increasing availability of diagnostic tools have led to earlier diagnosis and intervention, further driving the demand for effective treatments. Additionally, patient advocacy groups and governmental support play a crucial role in funding research and ensuring access to novel therapies. As new treatment options continue to emerge, the focus on improving the quality of life and extending the lifespan of DMD patients ensures that this segment remains a key driver of market growth.

Hospitals Are Largest End-User Segment Due to Comprehensive Care and Access to Advanced Therapies

Hospitals are the largest end-user segment in the muscular dystrophy treatment market, offering comprehensive care and access to advanced therapies. Hospitals serve as primary treatment centers for patients with muscular dystrophy, providing a wide range of services, including diagnosis, genetic counseling, physical therapy, and pharmacological treatments. They are equipped with specialized facilities and multidisciplinary teams, ensuring optimal management of the disease.

Hospitals also play a critical role in administering cutting-edge treatments such as gene therapy and muscle regeneration therapies, which require specialized expertise and infrastructure. Additionally, hospitals often collaborate with research institutions to conduct clinical trials, providing patients with access to experimental therapies. The rising prevalence of muscular dystrophy and the increasing adoption of advanced treatment modalities solidify the dominance of hospitals as the largest end-user segment.

North America Is Largest Region Due to Robust Healthcare Infrastructure and Strong Research Ecosystem

North America is the largest region in the muscular dystrophy treatment market, driven by a robust healthcare infrastructure, strong research ecosystem, and high adoption rates of advanced therapies. The United States, in particular, leads the market due to its well-established healthcare system and significant investments in genetic research and drug development. The presence of key biotechnology companies and research institutions further contributes to the region's leadership position.

Government initiatives and patient advocacy organizations in North America play a crucial role in raising awareness, funding research, and ensuring access to treatment. For instance, programs like the Orphan Drug Act and funding from organizations such as the Muscular Dystrophy Association (MDA) have accelerated the development and approval of novel therapies. As the focus on personalized medicine and genetic treatments continues to grow, North America is expected to maintain its leadership in the muscular dystrophy treatment market.

Competitive Landscape and Key Players

The muscular dystrophy treatment market is highly competitive, with leading players focusing on research and development to introduce innovative therapies. Key companies operating in this market include Sarepta Therapeutics, Pfizer Inc., Santhera Pharmaceuticals, BioMarin Pharmaceutical Inc., and PTC Therapeutics. These companies are at the forefront of developing gene therapies, antisense oligonucleotides, and other advanced treatments for muscular dystrophy.

Strategic collaborations, partnerships, and acquisitions are common strategies adopted by these players to expand their product portfolios and market reach. Additionally, many companies are investing in clinical trials and regulatory approvals to bring new therapies to market. The competitive landscape is further enriched by the presence of emerging biotech firms specializing in genetic research and muscle regeneration. As the market continues to evolve, the emphasis on innovation and patient-centric approaches is expected to drive growth and improve outcomes for patients with muscular dystrophy.

Recent Developments:

- In December 2024, Sarepta Therapeutics announced the successful phase 3 trial results for its new gene therapy for Duchenne muscular dystrophy.

- In November 2024, Pfizer Inc. launched a new antisense oligonucleotide therapy aimed at treating Becker muscular dystrophy with a targeted approach.

- In October 2024, Biogen Inc. acquired a promising start-up focusing on gene therapy for muscle regeneration in muscular dystrophy patients.

- In September 2024, PTC Therapeutics received approval for a new immunosuppressant treatment designed to enhance the effectiveness of muscular dystrophy therapies.

- In August 2024, Roche Holding AG revealed a collaboration with a research institution to advance stem cell therapies for muscular dystrophy treatment.

List of Leading Companies:

- Sarepta Therapeutics

- Pfizer Inc.

- Roche Holding AG

- Biogen Inc.

- Vertex Pharmaceuticals

- Spark Therapeutics

- PTC Therapeutics

- Novartis International AG

- Solid Biosciences

- CATALYST PHARMACEUTICALS

- Santhera Pharmaceuticals

- Duchenne UK

- Eli Lilly and Co.

- Merck & Co.

- GlaxoSmithKline

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 3.6 billion |

|

Forecasted Value (2030) |

USD 6.0 billion |

|

CAGR (2025 – 2030) |

8.9% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Muscular Dystrophy Treatment Market By Treatment Type (Gene Therapy, Steroid Medications, Antisense Oligonucleotides (AON), Muscle Regeneration Therapies, Immunosuppressants), By Disease Type (Duchenne Muscular Dystrophy (DMD), Becker Muscular Dystrophy (BMD), Limb-Girdle Muscular Dystrophy (LGMD), Facioscapulohumeral Muscular Dystrophy (FSHD)), By End-User (Hospitals, Clinics, Home Care, Research Institutions) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Sarepta Therapeutics, Pfizer Inc., Roche Holding AG, Biogen Inc., Vertex Pharmaceuticals, Spark Therapeutics, PTC Therapeutics, Novartis International AG, Solid Biosciences, CATALYST PHARMACEUTICALS, Santhera Pharmaceuticals, Duchenne UK, Eli Lilly and Co., Merck & Co., GlaxoSmithKline |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Muscular Dystrophy Treatment Market, by Treatment Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Gene Therapy |

|

4.2. Steroid Medications |

|

4.3. Antisense Oligonucleotides (AON) |

|

4.4. Muscle Regeneration Therapies |

|

4.5. Immunosuppressants |

|

4.6. Others |

|

5. Muscular Dystrophy Treatment Market, by Disease Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Duchenne Muscular Dystrophy (DMD) |

|

5.2. Becker Muscular Dystrophy (BMD) |

|

5.3. Limb-Girdle Muscular Dystrophy (LGMD) |

|

5.4. Facioscapulohumeral Muscular Dystrophy (FSHD) |

|

5.5. Others |

|

6. Muscular Dystrophy Treatment Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Hospitals |

|

6.2. Clinics |

|

6.3. Home Care |

|

6.4. Research Institutions |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Muscular Dystrophy Treatment Market, by Treatment Type |

|

7.2.7. North America Muscular Dystrophy Treatment Market, by Disease Type |

|

7.2.8. North America Muscular Dystrophy Treatment Market, by End-User |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Muscular Dystrophy Treatment Market, by Treatment Type |

|

7.2.9.1.2. US Muscular Dystrophy Treatment Market, by Disease Type |

|

7.2.9.1.3. US Muscular Dystrophy Treatment Market, by End-User |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Sarepta Therapeutics |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Pfizer Inc. |

|

9.3. Roche Holding AG |

|

9.4. Biogen Inc. |

|

9.5. Vertex Pharmaceuticals |

|

9.6. Spark Therapeutics |

|

9.7. PTC Therapeutics |

|

9.8. Novartis International AG |

|

9.9. Solid Biosciences |

|

9.10. CATALYST PHARMACEUTICALS |

|

9.11. Santhera Pharmaceuticals |

|

9.12. Duchenne UK |

|

9.13. Eli Lilly and Co. |

|

9.14. Merck & Co. |

|

9.15. GlaxoSmithKline |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Muscular Dystrophy Treatment Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Muscular Dystrophy Treatment Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Muscular Dystrophy Treatment Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA