As per Intent Market Research, the Motion Preservation Devices Market was valued at USD 1.4 Billion in 2024-e and will surpass USD 2.8 Billion by 2030; growing at a CAGR of 10.7% during 2025-2030.

The motion preservation devices market is experiencing significant growth due to the rising prevalence of spinal disorders and the increasing demand for non-fusion surgical procedures. These devices aim to preserve the natural movement of the spine while offering patients alternative treatments to traditional fusion-based techniques. As spinal diseases such as degenerative disc disease and scoliosis become more common, the need for motion-preserving surgical solutions continues to rise, making this market one of the most dynamic within the broader orthopedic devices sector. Factors such as aging populations, technological advancements, and rising awareness of minimally invasive surgery are driving this market forward.

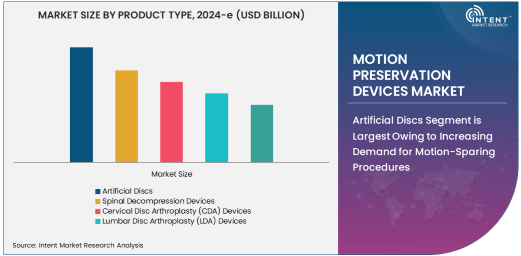

Artificial Discs Segment is Largest Owing to Increasing Demand for Motion-Sparing Procedures

The artificial discs segment dominates the motion preservation devices market due to their ability to provide a motion-sparing alternative to traditional spinal fusion surgeries. Artificial discs are designed to replace damaged spinal discs while maintaining the natural movement of the spine, making them highly sought after for treating conditions like degenerative disc disease. This segment benefits from advancements in material technology, improving the performance and longevity of artificial discs. Additionally, artificial disc replacements are less invasive than spinal fusion procedures, reducing recovery times and complications, which further boosts their popularity among patients and surgeons alike.

The growth in this segment is also supported by an expanding body of clinical evidence that demonstrates the benefits of artificial discs in terms of preserving mobility and reducing pain. With increasing approval and adoption in markets such as North America and Europe, artificial discs are set to continue their dominance in the market for motion preservation devices.

Minimally Invasive Motion Preservation Devices Segment is Fastest Growing Owing to Advancements in Surgical Techniques

The minimally invasive motion preservation devices segment is the fastest growing within the market, driven by continuous advancements in surgical techniques and an increasing preference for less invasive procedures. These devices typically allow surgeons to perform spinal surgeries with smaller incisions, reducing the risk of complications, minimizing blood loss, and accelerating patient recovery times. As the healthcare industry pushes for more cost-effective treatments and quicker recoveries, minimally invasive motion preservation devices are becoming the preferred option for both patients and healthcare providers.

Moreover, the development of robotic-assisted surgeries and other technologies that improve the precision of spinal surgeries has played a key role in this segment’s growth. Minimally invasive devices cater to a broad range of spinal disorders, including degenerative disc disease and spinal trauma, making them applicable to a large patient population. With growing awareness and a higher demand for minimally invasive surgical options, this segment is expected to expand rapidly in the coming years.

Degenerative Disc Disease Application is Largest Owing to High Prevalence and Impact

The degenerative disc disease application is the largest in the motion preservation devices market due to the high prevalence of this condition, particularly in aging populations. Degenerative disc disease is a leading cause of back pain and spine-related disability, with millions of people worldwide experiencing chronic pain and discomfort associated with the wear and tear of spinal discs. Motion preservation devices, such as artificial discs and spinal decompression devices, provide effective solutions for treating this condition, which drives significant demand.

Additionally, the ongoing research and development in degenerative disc disease treatments have led to improved outcomes for patients, further driving the adoption of motion preservation devices. As people continue to live longer and maintain active lifestyles, the prevalence of degenerative disc disease is expected to rise, ensuring that the market for motion preservation devices targeting this application remains robust.

Metal-based Materials Segment is Largest Owing to Durability and Performance

The metal-based materials segment is the largest within the material category, primarily due to the superior durability and strength of metals such as titanium and stainless steel, which are commonly used in motion preservation devices. These materials are widely preferred for artificial discs and other spinal implants because they offer long-term stability, resistance to wear, and the ability to withstand the mechanical stresses placed on the spine during normal activities. Metal-based materials have been proven to provide excellent mechanical performance and longevity, making them the material of choice for spinal devices in the market.

Furthermore, metal alloys allow for precise manufacturing and customizability, ensuring that the implants meet the unique needs of individual patients. The combination of durability and adaptability ensures that metal-based materials continue to dominate the motion preservation device market.

North America Region is Largest Market Owing to Advanced Healthcare Infrastructure

North America holds the largest share of the motion preservation devices market, owing to its advanced healthcare infrastructure, high adoption rates of cutting-edge medical technologies, and a large patient population suffering from spinal disorders. The region has long been at the forefront of adopting new spinal treatments, and the demand for motion preservation devices, particularly in the United States, continues to increase. A growing aging population, higher levels of healthcare spending, and a preference for non-invasive surgical options contribute to North America's market leadership.

In addition, North American regulatory bodies like the FDA have been at the forefront of approving new spinal technologies, fostering an environment conducive to innovation. The region's dominance is further supported by the presence of leading market players and an established network of skilled healthcare professionals specializing in spinal surgeries.

Competitive Landscape and Leading Companies

The motion preservation devices market is highly competitive, with several key players dominating the landscape. Companies like Medtronic, NuVasive, and Stryker lead the market with their advanced technologies and broad product portfolios. These companies have established a strong presence through strategic mergers, acquisitions, and partnerships aimed at expanding their product offerings and increasing their market reach.

Medtronic, for example, has invested heavily in developing new artificial disc technologies, while NuVasive focuses on minimally invasive solutions. As the market continues to evolve, companies are increasingly prioritizing research and development to bring innovative products to market and cater to the growing demand for non-fusion spine surgeries. Additionally, collaboration between industry players and healthcare providers, along with investments in clinical trials, is expected to foster continued growth and competition in the motion preservation devices market.

Recent Developments:

- Medtronic announced the launch of its new Artificial Cervical Disc technology, aiming to reduce complications in cervical spine surgeries.

- NuVasive recently received FDA approval for its Minimally Invasive Spine Surgery Device, allowing for quicker recovery and less invasive procedures.

- Stryker Corporation expanded its portfolio of spinal motion preservation devices by acquiring Spinal Elements, a leader in spine technologies.

- DePuy Synthes rolled out its next-generation Cervical Disc Prosthesis, designed to enhance post-operative mobility and patient recovery.

- Zimmer Biomet received regulatory clearance for its Motion Preservation Technology, which promises enhanced clinical outcomes in spinal surgeries.

List of Leading Companies:

- Medtronic

- NuVasive

- Stryker Corporation

- Zimmer Biomet

- DePuy Synthes

- Johnson & Johnson

- Orthofix

- Globus Medical

- Aesculap (B. Braun)

- Spinal Elements

- Alphatec Spine

- K2M

- RTI Surgical

- SeaSpine

- X-spine Systems

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 1.4 Billion |

|

Forecasted Value (2030) |

USD 2.8 Billion |

|

CAGR (2025 – 2030) |

10.7% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Motion Preservation Devices Market By Product Type (Artificial Discs, Spinal Decompression Devices, Cervical Disc Arthroplasty Devices, Lumbar Disc Arthroplasty Devices), By End-User Industry (Hospitals, Ambulatory Surgical Centers, Orthopedic Clinics, Rehabilitation Centers), By Application (Degenerative Disc Disease, Scoliosis, Spinal Trauma, Post-Operative Recovery), By Material (Metal-based Materials, Ceramic-based Materials, Polymeric Materials), By Technology (Non-invasive Motion Preservation Devices, Minimally Invasive Motion Preservation Devices) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Medtronic, NuVasive, Stryker Corporation, Zimmer Biomet, DePuy Synthes, Johnson & Johnson, Orthofix, Globus Medical, Aesculap (B. Braun), Spinal Elements, Alphatec Spine, K2M, RTI Surgical, SeaSpine, X-spine Systems |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Motion Preservation Devices Market, by Product Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Artificial Discs |

|

4.2. Spinal Decompression Devices |

|

4.3. Cervical Disc Arthroplasty (CDA) Devices |

|

4.4. Lumbar Disc Arthroplasty (LDA) Devices |

|

4.5. Other Motion Preservation Devices |

|

5. Motion Preservation Devices Market, by End-User Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Hospitals |

|

5.2. Ambulatory Surgical Centers |

|

5.3. Orthopedic Clinics |

|

5.4. Rehabilitation Centers |

|

6. Motion Preservation Devices Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Degenerative Disc Disease |

|

6.2. Scoliosis |

|

6.3. Spinal Trauma |

|

6.4. Post-Operative Recovery |

|

6.5. Other Spinal Disorders |

|

7. Motion Preservation Devices Market, by Material (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Metal-based Materials |

|

7.2. Ceramic-based Materials |

|

7.3. Polymeric Materials |

|

8. Motion Preservation Devices Market, by Technology (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Non-invasive Motion Preservation Devices |

|

8.2. Minimally Invasive Motion Preservation Devices |

|

9. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

9.1. Regional Overview |

|

9.2. North America |

|

9.2.1. Regional Trends & Growth Drivers |

|

9.2.2. Barriers & Challenges |

|

9.2.3. Opportunities |

|

9.2.4. Factor Impact Analysis |

|

9.2.5. Technology Trends |

|

9.2.6. North America Motion Preservation Devices Market, by Product Type |

|

9.2.7. North America Motion Preservation Devices Market, by End-User Industry |

|

9.2.8. North America Motion Preservation Devices Market, by Application |

|

9.2.9. North America Motion Preservation Devices Market, by Material |

|

9.2.10. North America Motion Preservation Devices Market, by Technology |

|

9.2.11. By Country |

|

9.2.11.1. US |

|

9.2.11.1.1. US Motion Preservation Devices Market, by Product Type |

|

9.2.11.1.2. US Motion Preservation Devices Market, by End-User Industry |

|

9.2.11.1.3. US Motion Preservation Devices Market, by Application |

|

9.2.11.1.4. US Motion Preservation Devices Market, by Material |

|

9.2.11.1.5. US Motion Preservation Devices Market, by Technology |

|

9.2.11.2. Canada |

|

9.2.11.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

9.3. Europe |

|

9.4. Asia-Pacific |

|

9.5. Latin America |

|

9.6. Middle East & Africa |

|

10. Competitive Landscape |

|

10.1. Overview of the Key Players |

|

10.2. Competitive Ecosystem |

|

10.2.1. Level of Fragmentation |

|

10.2.2. Market Consolidation |

|

10.2.3. Product Innovation |

|

10.3. Company Share Analysis |

|

10.4. Company Benchmarking Matrix |

|

10.4.1. Strategic Overview |

|

10.4.2. Product Innovations |

|

10.5. Start-up Ecosystem |

|

10.6. Strategic Competitive Insights/ Customer Imperatives |

|

10.7. ESG Matrix/ Sustainability Matrix |

|

10.8. Manufacturing Network |

|

10.8.1. Locations |

|

10.8.2. Supply Chain and Logistics |

|

10.8.3. Product Flexibility/Customization |

|

10.8.4. Digital Transformation and Connectivity |

|

10.8.5. Environmental and Regulatory Compliance |

|

10.9. Technology Readiness Level Matrix |

|

10.10. Technology Maturity Curve |

|

10.11. Buying Criteria |

|

11. Company Profiles |

|

11.1. Medtronic |

|

11.1.1. Company Overview |

|

11.1.2. Company Financials |

|

11.1.3. Product/Service Portfolio |

|

11.1.4. Recent Developments |

|

11.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

11.2. NuVasive |

|

11.3. Stryker Corporation |

|

11.4. Zimmer Biomet |

|

11.5. DePuy Synthes |

|

11.6. Johnson & Johnson |

|

11.7. Orthofix |

|

11.8. Globus Medical |

|

11.9. Aesculap (B. Braun) |

|

11.10. Spinal Elements |

|

11.11. Alphatec Spine |

|

11.12. K2M |

|

11.13. RTI Surgical |

|

11.14. SeaSpine |

|

11.15. X-spine Systems |

|

12. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Motion Preservation Devices Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Motion Preservation Devices Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Motion Preservation Devices Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA