As per Intent Market Research, the Monosodium Glutamate (MSG) Market was valued at USD 4.2 Billion in 2024-e and will surpass USD 6.1 Billion by 2030; growing at a CAGR of 5.7% during 2025-2030.

Monosodium Glutamate (MSG) is a widely used flavor enhancer that has found applications across various industries, particularly in food and beverage products. With its ability to enhance umami, the savory taste in food, MSG is a key ingredient in processed foods, restaurant dishes, and snack products. The global MSG market is experiencing growth due to the increasing demand for processed foods and the expanding foodservice sector. Alongside this, MSG is also being utilized in animal feed, pharmaceuticals, and health supplements, which broadens its scope across industries. The market continues to evolve with new product types, more sustainable production methods, and a growing preference for plant-based sources of MSG. This article examines key segments of the MSG market and highlights the largest or fastest-growing subsegments in each category.

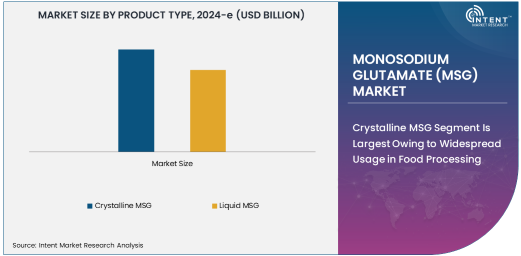

Crystalline MSG Segment Is Largest Owing to Widespread Usage in Food Processing

The crystalline MSG segment is the largest in the global MSG market due to its long-standing presence in the food industry and widespread usage in processed foods. Crystalline MSG is highly favored for its purity and ease of use in various food applications, particularly in soups, sauces, snacks, and seasonings. It is valued for providing the most potent umami flavor with minimal impact on the overall composition of the food. As food manufacturers continue to prioritize flavor enhancement, crystalline MSG remains a go-to ingredient in their formulations, contributing to its dominance in the market.

In the food processing industry, crystalline MSG is preferred due to its consistent quality, longer shelf life, and versatility in a range of applications. Additionally, advancements in production techniques have made crystalline MSG more affordable, thus promoting its use in both high-end culinary environments and mass-produced food products. As demand for processed and convenience foods increases, the crystalline MSG segment is expected to continue its strong growth trajectory.

Plant-Based MSG Segment Is Fastest Growing Due to Rising Consumer Preference for Natural Products

The plant-based MSG segment is the fastest growing owing to the rising consumer demand for natural and plant-derived ingredients in food products. As more consumers become conscious of health and environmental issues, there is a noticeable shift towards plant-based MSG as a more sustainable and perceived healthier alternative to animal-based MSG. This shift aligns with broader food industry trends towards clean-label products and plant-based diets. Companies are responding by developing and marketing plant-based MSG products, which appeal to health-conscious consumers and those with dietary restrictions.

Plant-based MSG, typically derived from hydrolyzed vegetable proteins or other natural sources, is gaining traction not only in food products but also in applications like animal feed and pharmaceuticals. This rapid growth in the plant-based MSG market segment is expected to continue, fueled by increasing consumer awareness of the environmental and health benefits of plant-derived products. As more brands and manufacturers incorporate plant-based MSG into their products, the segment's share of the market will likely expand further.

Food & Beverages Application Is Largest Due to High Demand for Flavor Enhancement

The food and beverages segment is the largest application area for MSG, driven by the constant demand for flavor enhancers in processed food products. As the global population grows and urbanization increases, consumers are opting for convenience foods that are easy to prepare yet still satisfy their taste preferences. MSG serves as a key ingredient in many packaged foods, including savory snacks, instant noodles, soups, and sauces. It enhances the overall taste profile of food, providing a savory umami flavor that is appealing to a wide variety of consumers.

Moreover, with the increasing popularity of ethnic and fast food, which heavily rely on MSG to achieve desired flavors, the demand for MSG in the food and beverages sector is projected to continue growing. As the sector evolves with changing consumer preferences, there is also a notable shift towards MSG formulations that are natural, clean-label, and non-GMO, further expanding its market presence.

Food Processing Industry Is Largest End-Use Industry Due to Uninterrupted Demand for MSG

The food processing industry is the largest end-use industry for MSG, primarily due to its extensive application in enhancing flavors in processed and packaged foods. Food processing plants and manufacturers use MSG to improve the taste of their products, making them more attractive to consumers. MSG is particularly important in the production of soups, sauces, seasonings, processed meats, and convenience foods. The growth of the food processing sector is expected to continue, especially in emerging markets, as the demand for packaged and ready-to-eat foods rises.

Additionally, food processors are increasingly adopting MSG to meet consumer demands for flavorful and easy-to-prepare food options. Innovations in MSG production, such as the development of high-quality, low-sodium alternatives, are also contributing to the growth of MSG usage in food processing, making it more attractive to health-conscious consumers. As a result, the food processing industry will remain a key driver of MSG market expansion.

Online Retail Distribution Channel Is Fastest Growing Due to E-commerce Expansion

The online retail distribution channel is the fastest growing in the MSG market, driven by the global expansion of e-commerce. As consumers increasingly turn to online platforms for food purchases and ingredients, e-commerce channels are becoming essential for MSG manufacturers and suppliers. This growth is fueled by the increasing reliance on online shopping for convenience products, which includes flavor enhancers and seasonings. Moreover, online retailers offer a wide variety of MSG products, including specialized and natural MSG options, catering to diverse consumer preferences.

With the convenience of home delivery and the ability to access global brands, online retail platforms are rapidly becoming the preferred shopping method for consumers looking to purchase MSG in smaller quantities or niche product types, including plant-based and organic variants. As internet penetration rises globally, especially in developing regions, the online retail segment is expected to continue its strong growth.

Asia-Pacific Region Is Largest Due to High Consumption and Production

The Asia-Pacific (APAC) region is the largest market for MSG, accounting for a significant portion of both global consumption and production. This region has a long history of using MSG in various cuisines, particularly in countries like China, Japan, and South Korea. The high demand for MSG in the APAC region is driven by the popularity of umami-rich foods and the region's extensive food processing industry. Furthermore, as urbanization increases in countries like India and Indonesia, there is a growing demand for packaged foods, which is further boosting MSG consumption.

Additionally, APAC hosts several leading MSG manufacturers, including Ajinomoto and Meihua Holdings, further reinforcing the region's dominant position in the global market. The region's continued economic development, rising disposable incomes, and expanding foodservice sector are expected to sustain strong demand for MSG, ensuring the APAC region remains the largest market for MSG in the coming years.

Leading Companies and Competitive Landscape

The global MSG market is highly competitive, with several leading companies dominating the industry. Companies like Ajinomoto, Fufeng Group, and Meihua Holdings hold significant market shares due to their large-scale production capabilities and extensive product offerings. These companies are focused on product innovation, including the development of plant-based and low-sodium MSG alternatives, to meet changing consumer preferences. Additionally, strategic partnerships, mergers, and acquisitions are common among top players looking to expand their global footprint and enhance their product portfolios.

The competitive landscape is also characterized by the presence of regional players that cater to local demands, while multinational companies continue to dominate in terms of production volume and brand recognition. As sustainability and clean-label trends gain importance, companies are investing in more environmentally friendly production methods and exploring new product formats to maintain their competitive edge in the MSG market

Recent Developments:

- Ajinomoto Expands in Southeast Asia: Ajinomoto Co., Inc. announced a new production facility in Thailand to meet the rising demand for MSG and seasonings in the region.

- Fufeng Group’s Strategic Partnership: Fufeng Group has entered into a strategic partnership with a global food company to strengthen its presence in the global MSG market and enhance its product offerings.

- FDA Approval for New MSG Formulation: In 2024, the U.S. FDA approved a new formulation of MSG by a leading food company, making it suitable for use in new health food product lines.

- Meihua Holdings Market Expansion: Meihua Holdings has expanded its market footprint with a significant investment in a new MSG production plant in North America.

- Sustainability Initiative by Tonghua Dongbao: Tonghua Dongbao Pharmaceutical Co. launched a new initiative to reduce the environmental impact of MSG production, focusing on water usage and waste management.

List of Leading Companies:

- Ajinomoto Co., Inc.

- Wuhan Sanzheng Group

- Fuji Oil Company

- Guangdong Wing Wing Food Technology Co., Ltd.

- Shanghai Bright Dairy & Food Co., Ltd.

- Meihua Holdings Group Co., Ltd.

- Fufeng Group Limited

- Jinjiang Fufeng Biotech Co., Ltd.

- CJ CheilJedang Corporation

- The Kewpie Corporation

- Sunkeen Group Co., Ltd.

- Nissin Foods Holdings Co., Ltd.

- Kerry Group Plc

- Tate & Lyle PLC

- Tonghua Dongbao Pharmaceutical Co.

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 4.2 Billion |

|

Forecasted Value (2030) |

USD 6.1 Billion |

|

CAGR (2025 – 2030) |

5.7% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Monosodium Glutamate (MSG) Market by Product Type (Crystalline MSG, Liquid MSG), by Source (Plant-Based MSG, Animal-Based MSG), by Application (Food & Beverages, Animal Feed, Pharmaceuticals & Health Supplements), by End-Use Industry (Food Processing, Restaurants & Foodservice, Household, Industrial Applications), and by Distribution Channel (Direct Sales, Retail Sales, Online Retail); Global Insights & Forecast (2023 – 2030) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Ajinomoto Co., Inc., Wuhan Sanzheng Group, Fuji Oil Company, Guangdong Wing Wing Food Technology Co., Ltd., Shanghai Bright Dairy & Food Co., Ltd., Meihua Holdings Group Co., Ltd., Fufeng Group Limited, Jinjiang Fufeng Biotech Co., Ltd., CJ CheilJedang Corporation, The Kewpie Corporation, Sunkeen Group Co., Ltd., Nissin Foods Holdings Co., Ltd., Kerry Group Plc, Tate & Lyle PLC, Tonghua Dongbao Pharmaceutical Co. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Monosodium Glutamate (MSG) Market, by Product Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Crystalline MSG |

|

4.2. Liquid MSG |

|

5. Monosodium Glutamate (MSG) Market, by Source (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Plant-based MSG |

|

5.2. Animal-based MSG |

|

6. Monosodium Glutamate (MSG) Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Food & Beverages |

|

6.2. Animal Feed |

|

6.3. Pharmaceuticals & Health Supplements |

|

6.4. Others |

|

7. Monosodium Glutamate (MSG) Market, by End-Use Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Food Processing |

|

7.2. Restaurants & Foodservice |

|

7.3. Household |

|

7.4. Industrial Applications |

|

8. Monosodium Glutamate (MSG) Market, by Distribution Channel (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Direct Sales |

|

8.2. Retail Sales |

|

8.3. Online Retail |

|

9. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

9.1. Regional Overview |

|

9.2. North America |

|

9.2.1. Regional Trends & Growth Drivers |

|

9.2.2. Barriers & Challenges |

|

9.2.3. Opportunities |

|

9.2.4. Factor Impact Analysis |

|

9.2.5. Technology Trends |

|

9.2.6. North America Monosodium Glutamate (MSG) Market, by Product Type |

|

9.2.7. North America Monosodium Glutamate (MSG) Market, by Source |

|

9.2.8. North America Monosodium Glutamate (MSG) Market, by Application |

|

9.2.9. North America Monosodium Glutamate (MSG) Market, by End-Use Industry |

|

9.2.10. North America Monosodium Glutamate (MSG) Market, by Distribution Channel |

|

9.2.11. By Country |

|

9.2.11.1. US |

|

9.2.11.1.1. US Monosodium Glutamate (MSG) Market, by Product Type |

|

9.2.11.1.2. US Monosodium Glutamate (MSG) Market, by Source |

|

9.2.11.1.3. US Monosodium Glutamate (MSG) Market, by Application |

|

9.2.11.1.4. US Monosodium Glutamate (MSG) Market, by End-Use Industry |

|

9.2.11.1.5. US Monosodium Glutamate (MSG) Market, by Distribution Channel |

|

9.2.11.2. Canada |

|

9.2.11.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

9.3. Europe |

|

9.4. Asia-Pacific |

|

9.5. Latin America |

|

9.6. Middle East & Africa |

|

10. Competitive Landscape |

|

10.1. Overview of the Key Players |

|

10.2. Competitive Ecosystem |

|

10.2.1. Level of Fragmentation |

|

10.2.2. Market Consolidation |

|

10.2.3. Product Innovation |

|

10.3. Company Share Analysis |

|

10.4. Company Benchmarking Matrix |

|

10.4.1. Strategic Overview |

|

10.4.2. Product Innovations |

|

10.5. Start-up Ecosystem |

|

10.6. Strategic Competitive Insights/ Customer Imperatives |

|

10.7. ESG Matrix/ Sustainability Matrix |

|

10.8. Manufacturing Network |

|

10.8.1. Locations |

|

10.8.2. Supply Chain and Logistics |

|

10.8.3. Product Flexibility/Customization |

|

10.8.4. Digital Transformation and Connectivity |

|

10.8.5. Environmental and Regulatory Compliance |

|

10.9. Technology Readiness Level Matrix |

|

10.10. Technology Maturity Curve |

|

10.11. Buying Criteria |

|

11. Company Profiles |

|

11.1. Ajinomoto Co., Inc. |

|

11.1.1. Company Overview |

|

11.1.2. Company Financials |

|

11.1.3. Product/Service Portfolio |

|

11.1.4. Recent Developments |

|

11.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

11.2. Wuhan Sanzheng Group |

|

11.3. Fuji Oil Company |

|

11.4. Guangdong Wing Wing Food Technology Co., Ltd. |

|

11.5. Shanghai Bright Dairy & Food Co., Ltd. |

|

11.6. Meihua Holdings Group Co., Ltd. |

|

11.7. Fufeng Group Limited |

|

11.8. Jinjiang Fufeng Biotech Co., Ltd. |

|

11.9. CJ CheilJedang Corporation |

|

11.10. The Kewpie Corporation |

|

11.11. Sunkeen Group Co., Ltd. |

|

11.12. Nissin Foods Holdings Co., Ltd. |

|

11.13. Kerry Group Plc |

|

11.14. Tate & Lyle PLC |

|

11.15. Tonghua Dongbao Pharmaceutical Co. |

|

12. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Monosodium Glutamate Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Monosodium Glutamate Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Monosodium Glutamate Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA