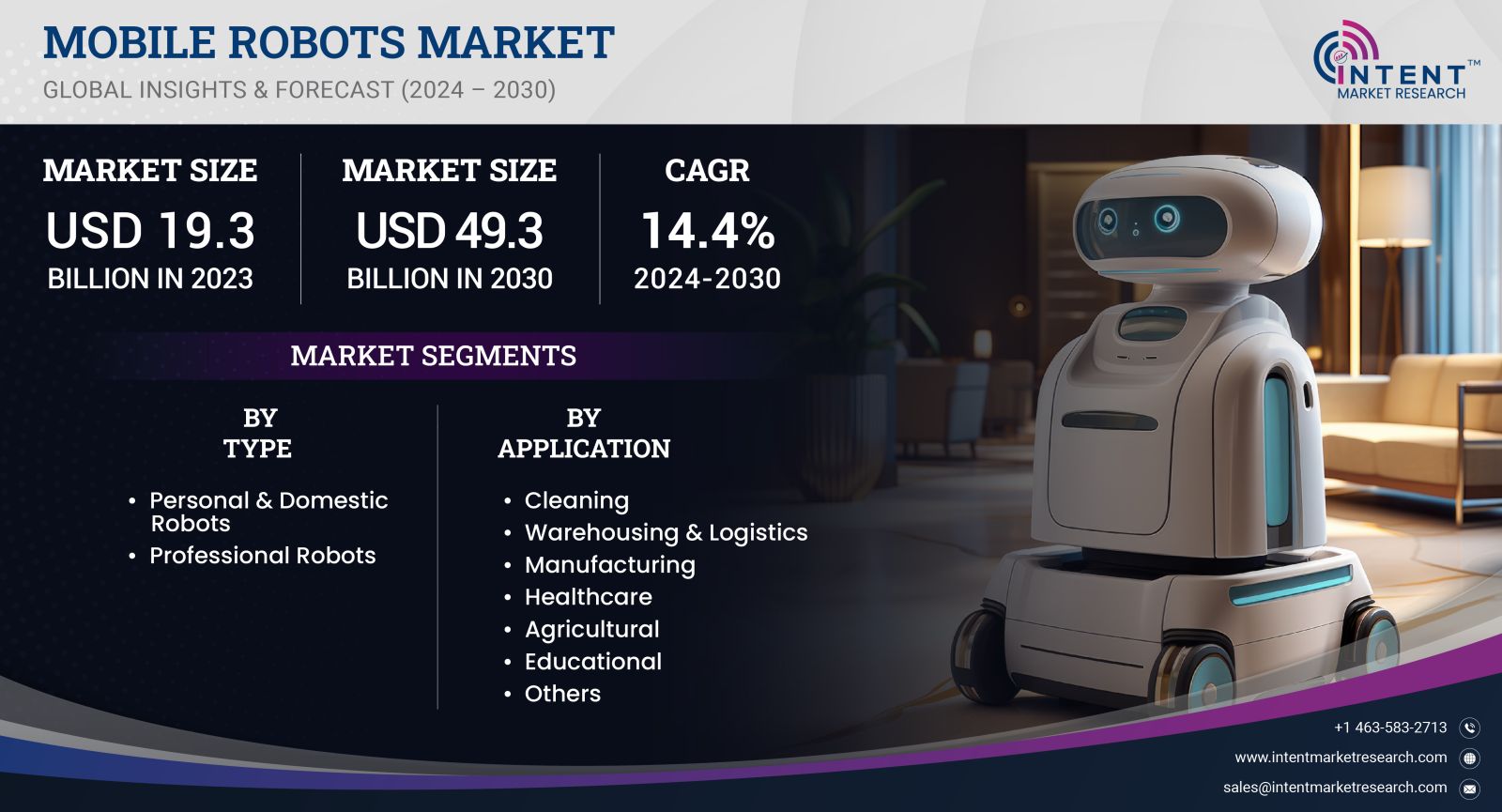

As per Intent Market Research, the Mobile Robots Market was valued at USD 19.3 billion in 2023-e and will surpass USD 49.3 billion by 2030; growing at a CAGR of 14.4% during 2024 - 2030.

The mobile robots market is rapidly evolving, fueled by advancements in automation technologies and the increasing demand for efficient, flexible solutions across various industries. Mobile robots, capable of navigating autonomously in dynamic environments, are being deployed in sectors such as manufacturing, logistics, healthcare, and retail. As organizations seek to enhance operational efficiency, reduce labor costs, and improve safety, the adoption of mobile robots has surged.

The growth of the mobile robots market is driven by several factors, including the rising trend of Industry 4.0, advancements in artificial intelligence (AI) and machine learning, and the increasing need for contactless solutions in the post-pandemic world. As businesses continue to invest in automation and robotics to streamline their operations, mobile robots are becoming integral to enhancing productivity and achieving strategic goals. This overview will explore key subsegments of the mobile robots market, highlighting areas of significant growth and innovation.

Logistics and Warehousing Segment is Largest Owing to E-Commerce Boom

The logistics and warehousing segment is the largest within the mobile robots market, primarily driven by the explosive growth of e-commerce and the increasing demand for efficient supply chain solutions. Mobile robots, such as Automated Guided Vehicles (AGVs) and Autonomous Mobile Robots (AMRs), are widely used in warehouses for tasks such as inventory management, picking, and transporting goods. The ability of these robots to operate continuously without fatigue enables businesses to enhance productivity and reduce operational costs significantly.

This segment is expected to maintain its dominance, with an anticipated CAGR of approximately 22% through 2030. The ongoing digital transformation in supply chains, coupled with the rising need for faster and more efficient order fulfillment, will further drive the adoption of mobile robots in logistics and warehousing. As companies look to optimize their operations and respond to changing consumer demands, the logistics sector will continue to be a primary driver of mobile robot technology.

Healthcare Segment is Fastest Growing Owing to Demand for Automation

The healthcare segment is witnessing the fastest growth within the mobile robots market, driven by the increasing demand for automation and efficient patient care solutions. Mobile robots in healthcare are deployed for various applications, including disinfecting hospital environments, transporting medications and supplies, and assisting with patient mobility. The COVID-19 pandemic has accelerated the adoption of robotics in healthcare settings as hospitals seek to minimize human contact and enhance safety protocols.

This segment is projected to grow at an impressive CAGR of approximately 25% during the forecast period, reflecting the urgent need for innovative solutions that improve operational efficiency and patient outcomes. The integration of mobile robots in healthcare not only streamlines processes but also allows medical staff to focus on critical tasks, ultimately improving the overall quality of care. As healthcare facilities continue to embrace technological advancements, the role of mobile robots in enhancing patient care will be paramount.

Manufacturing Segment is Largest Owing to Increased Automation Needs

The manufacturing segment is recognized as one of the largest within the mobile robots market, primarily due to the increasing need for automation and efficiency in production processes. Mobile robots are extensively used in manufacturing environments for tasks such as assembly, material handling, and quality control. Their ability to operate alongside human workers without the need for physical barriers enhances flexibility and productivity on the production floor.

As manufacturers continue to adopt smart manufacturing practices and Industry 4.0 technologies, the mobile robots segment is expected to grow steadily, with a projected CAGR of around 18% from 2024 to 2030. The push for enhanced operational efficiency, reduced lead times, and improved safety standards will drive the demand for mobile robots in manufacturing settings. The continuous development of advanced robotics technologies will further solidify the manufacturing sector's reliance on mobile automation solutions.

Retail Segment is Fastest Growing Owing to Enhanced Customer Experience

The retail segment is emerging as the fastest-growing area within the mobile robots market, driven by the increasing emphasis on enhancing customer experience and operational efficiency. Mobile robots in retail are used for various applications, including inventory management, shelf scanning, and customer assistance. By automating routine tasks, retailers can improve inventory accuracy, reduce labor costs, and offer a more personalized shopping experience.

This segment is projected to grow at an astonishing CAGR of approximately 27% during the forecast period, reflecting the industry's shift towards adopting advanced technologies to meet changing consumer preferences. The integration of mobile robots in retail environments not only streamlines operations but also provides valuable insights into customer behavior and preferences. As retailers increasingly leverage automation to improve operational efficiency and customer satisfaction, the retail segment will play a crucial role in the growth of the mobile robots market.

Asia-Pacific Region is Fastest Growing Owing to Rapid Industrialization

The Asia-Pacific region is the fastest-growing market for mobile robots, driven by rapid industrialization, technological advancements, and a burgeoning e-commerce sector. Countries such as China, Japan, and South Korea are at the forefront of adopting automation and robotics technologies across various industries, including logistics, manufacturing, and healthcare. The increasing focus on enhancing operational efficiency and productivity in the region's manufacturing and logistics sectors is significantly propelling the demand for mobile robots.

The Asia-Pacific region is projected to experience a CAGR of approximately 23% from 2024 to 2030, reflecting the ongoing digital transformation and investment in smart technologies. As organizations in the region prioritize automation to streamline operations and respond to competitive pressures, the mobile robots market will witness substantial growth. The region's commitment to innovation and technological development will position it as a key player in shaping the future of mobile robotics.

Competitive Landscape and Leading Companies

The mobile robots market is characterized by intense competition, with numerous players striving for market share through innovation, strategic partnerships, and technological advancements. The leading companies in this sector include:

- ABB Ltd. - A global leader in automation and robotics, ABB offers a range of mobile robotic solutions for manufacturing, logistics, and warehousing applications.

- KUKA AG - Known for its industrial robots, KUKA also develops mobile robots for logistics and material handling, focusing on enhancing operational efficiency.

- Amazon Robotics - A subsidiary of Amazon, this company specializes in mobile robotics solutions for warehouses, revolutionizing order fulfillment and inventory management.

- Boston Dynamics, Inc. - Renowned for its advanced robotic technologies, Boston Dynamics offers mobile robots capable of performing complex tasks in various environments.

- Fanuc Corporation - A leading manufacturer of industrial robots, Fanuc develops mobile robotic solutions for manufacturing and logistics applications.

- Yaskawa Electric Corporation - Yaskawa provides a variety of robotic solutions, including mobile robots for manufacturing and warehousing, with a focus on automation.

- Locus Robotics - Specializing in warehouse automation, Locus Robotics offers autonomous mobile robots designed to optimize order fulfillment processes.

- GrayOrange - This company develops AI-powered mobile robots for warehouse automation, focusing on improving efficiency and reducing operational costs.

- Clearpath Robotics - Clearpath provides autonomous mobile robots for research and industrial applications, emphasizing safety and reliability in various environments.

- Omron Corporation - A global leader in automation technology, Omron offers mobile robotics solutions for logistics, manufacturing, and healthcare applications.

The competitive landscape is marked by continuous innovation and collaboration, as companies strive to develop cutting-edge mobile robotic solutions that address the evolving needs of various industries. As the mobile robots market continues to grow, organizations will increasingly prioritize investments in advanced technologies to enhance their operational capabilities and maintain a competitive edge.

Report Objectives:

The report will help you answer some of the most critical questions in the Mobile Robots Market. A few of them are as follows:

- What are the key drivers, restraints, opportunities, and challenges influencing the market growth?

- What are the prevailing technology trends in the mobile robots market?

- What is the size of the mobile robots market based on segments, sub-segments, and regions?

- What is the size of different market segments across key regions: North America, Europe, Asia Pacific, Latin America, Middle East & Africa?

- What are the market opportunities for stakeholders after analyzing key market trends?

- Who are the leading market players and what are their market share and core competencies?

- What is the degree of competition in the market and what are the key growth strategies adopted by leading players?

- What is the competitive landscape of the market, including market share analysis, revenue analysis, and a ranking of key players?

Report Scope:

|

Report Features |

Description |

|

Market Size (2023-e) |

USD 19.3 billion |

|

Forecasted Value (2030) |

USD 49.3 billion |

|

CAGR (2024-2030) |

14.4% |

|

Base Year for Estimation |

2023-e |

|

Historic Year |

2022 |

|

Forecast Period |

2024-2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Mobile Robots Market By Type (Personal & Domestic Robots, Professional), By Application (Manufacturing, Cleaning, Educational, Agricultural, LifeSciences and Healthcare, Warehousing & Logistics) |

|

Regional Analysis |

North America (US, Canada), Europe (Germany, France, UK, Spain, Italy & Rest of Europe), Asia Pacific (China, Japan, South Korea, India, and rest of Asia Pacific), Latin America (Brazil, Mexico, Argentina, & Rest of Latin America), Middle East & Africa (Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA) |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1.Introduction |

|

1.1.Market Definition |

|

1.2.Scope of the Study |

|

1.3.Research Assumptions |

|

1.4.Study Limitations |

|

2.Research Methodology |

|

2.1.Research Approach |

|

2.1.1.Top-Down Method |

|

2.1.2.Bottom-Up Method |

|

2.1.3.Factor Impact Analysis |

|

2.2.Insights & Data Collection Process |

|

2.2.1.Secondary Research |

|

2.2.2.Primary Research |

|

2.3.Data Mining Process |

|

2.3.1.Data Analysis |

|

2.3.2.Data Validation and Revalidation |

|

2.3.3.Data Triangulation |

|

3.Executive Summary |

|

3.1.Major Markets & Segments |

|

3.2.Highest Growing Regions and Respective Countries |

|

3.3.Impact of Growth Drivers & Inhibitors |

|

3.4.Regulatory Overview by Country |

|

4.Mobile Robots Market, by Type (Market Size & Forecast: USD Billion, 2024 – 2030) |

|

4.1.Personal & Domestic Robots |

|

4.2.Professional Robots |

|

5.Mobile Robots Market, by Application (Market Size & Forecast: USD Billion, 2024 – 2030) |

|

5.1.Cleaning |

|

5.2.Warehousing & Logistics |

|

5.3.Manufacturing |

|

5.4.Healthcare |

|

5.5.Agricultural |

|

5.6.Educational |

|

5.7.Others |

|

6.Regional Analysis (Market Size & Forecast: USD Billion, 2024 – 2030) |

|

6.1.Regional Overview |

|

6.2.North America |

|

6.2.1.Regional Trends & Growth Drivers |

|

6.2.2.Barriers & Challenges |

|

6.2.3.Opportunities |

|

6.2.4.Factor Impact Analysis |

|

6.2.5.Technology Trends |

|

6.2.6.North America Mobile Robots Market, by Type |

|

6.2.7.North America Mobile Robots Market, by Application |

|

*Similar segmentation will be provided at each regional level |

|

6.3.By Country |

|

6.3.1.US |

|

6.3.1.1.US Mobile Robots Market, by Type |

|

6.3.1.2.US Mobile Robots Market, by Application |

|

6.3.2.Canada |

|

*Similar segmentation will be provided at each country level |

|

6.4.Europe |

|

6.5.APAC |

|

6.6.Latin America |

|

6.7.Middle East & Africa |

|

7.Competitive Landscape |

|

7.1.Overview of the Key Players |

|

7.2.Competitive Ecosystem |

|

7.2.1.Platform Manufacturers |

|

7.2.2.Subsystem Manufacturers |

|

7.2.3.Service Providers |

|

7.2.4.Software Providers |

|

7.3.Company Share Analysis |

|

7.4.Company Benchmarking Matrix |

|

7.4.1.Strategic Overview |

|

7.4.2.Product Innovations |

|

7.5.Start-up Ecosystem |

|

7.6.Strategic Competitive Insights/ Customer Imperatives |

|

7.7.ESG Matrix/ Sustainability Matrix |

|

7.8.Manufacturing Network |

|

7.8.1.Locations |

|

7.8.2.Supply Chain and Logistics |

|

7.8.3.Product Flexibility/Customization |

|

7.8.4.Digital Transformation and Connectivity |

|

7.8.5.Environmental and Regulatory Compliance |

|

7.9.Technology Readiness Level Matrix |

|

7.10.Technology Maturity Curve |

|

7.11.Buying Criteria |

|

8.Company Profiles |

|

8.1.ABB |

|

8.1.1.Company Overview |

|

8.1.2.Company Financials |

|

8.1.3.Product/Service Portfolio |

|

8.1.4.Recent Developments |

|

8.1.5.IMR Analysis |

|

*Similar information will be provided for other companies |

|

8.2.iRobot Corporation |

|

8.3.Honda Motor |

|

8.4.Mobile Industrial Robots |

|

8.5.Omron Automation |

|

8.6.KUKA AG |

|

8.7.Samsung |

|

8.8.Boston Dynamics |

|

8.9.Softbank Robotics |

|

8.10.Denso |

|

9.Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Mobile Robots Market. In the process, the analysis was also done to estimate the parent market and relevant adjacencies to major the impact of them on the mobile robots Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the mobile robots ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Estimation

A combination of top-down and bottom-up approaches was utilized to estimate the overall size of the mobile robots market. These methods were also employed to estimate the size of various subsegments within the market. The market size estimation methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size estimates, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size estimates.

NA