As per Intent Market Research, the Microsurgery Market was valued at USD 2.7 billion in 2024-e and will surpass USD 3.9 billion by 2030; growing at a CAGR of 6.4% during 2025 - 2030.

The microsurgery market is witnessing steady growth, fueled by the advancements in precision surgical technology and the increasing demand for minimally invasive procedures. Microsurgery, which involves the use of specialized equipment and techniques to perform complex surgeries requiring high precision, is prevalent in a wide range of applications such as neurosurgery, ophthalmic surgery, and orthopedic procedures. The market benefits from the rising prevalence of chronic diseases, an aging population, and the increasing adoption of robotic-assisted surgery across various medical fields. As healthcare systems increasingly prioritize patient outcomes, the demand for microsurgery procedures is expected to grow, further supported by innovations in surgical robots and minimally invasive technologies.

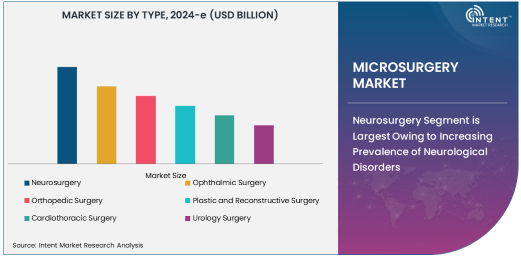

Neurosurgery Segment is Largest Owing to Increasing Prevalence of Neurological Disorders

Neurosurgery is the largest segment within the microsurgery market, driven by the growing incidence of neurological disorders such as brain tumors, spinal cord injuries, and degenerative diseases. With advancements in microsurgical techniques and robotic-assisted surgery, neurosurgery has become more efficient and precise, resulting in improved patient outcomes. The demand for high-precision instruments and minimally invasive procedures in the treatment of neurological conditions is propelling the growth of this segment. Neurosurgery procedures, such as brain tumor resection and spinal surgeries, rely heavily on the capabilities of microsurgical techniques to minimize damage to surrounding tissues and ensure faster recovery times.

The growing incidence of conditions like Alzheimer's disease, Parkinson's disease, and brain injuries is expected to continue driving the neurosurgery segment. Additionally, the increasing adoption of robotic systems for performing minimally invasive brain and spinal surgeries is enhancing the precision and efficiency of these procedures. This will likely lead to further growth in the microsurgery market, particularly in neurosurgery.

Robotic-Assisted Microsurgery is Fastest Growing Owing to Advancements in Surgical Robotics

Robotic-assisted microsurgery is the fastest-growing application segment within the microsurgery market. Robotic systems, such as the da Vinci Surgical System and other advanced surgical robots, provide surgeons with enhanced precision, flexibility, and control during complex microsurgical procedures. The integration of robotics in microsurgery has revolutionized the field by offering minimally invasive options that reduce recovery time, minimize surgical trauma, and improve overall surgical outcomes. With innovations in robotic systems that allow for greater dexterity and more precise movements, the demand for robotic-assisted microsurgeries is rapidly increasing.

This surge in demand for robotic-assisted microsurgery is also attributed to the growing preference for minimally invasive techniques, which are less painful and offer faster recovery compared to traditional open surgeries. The ability to perform intricate procedures with high precision and minimal disruption to healthy tissues is one of the key advantages driving the rapid adoption of robotic systems in microsurgery.

Hospitals Segment is Largest End-User Due to High Volume of Surgical Procedures

Hospitals continue to be the largest end-user of microsurgery services, primarily due to the high volume of surgeries performed in these settings. Hospitals are equipped with advanced surgical tools, including robotic surgical systems, and have the infrastructure to handle complex surgeries, including neurosurgery, ophthalmic surgery, and orthopedic procedures. The demand for microsurgery services in hospitals is also driven by the need for specialized care in critical surgeries, where precision is paramount for positive patient outcomes.

Hospitals are increasingly adopting robotic-assisted microsurgery for its ability to perform delicate procedures with enhanced precision and reduced human error. The increasing investment in healthcare technologies and the growing focus on providing high-quality, patient-centered care are further fueling the expansion of the microsurgery segment in hospitals. Additionally, hospitals are seeing improved patient satisfaction rates due to shorter recovery times and fewer complications, reinforcing the demand for microsurgical procedures.

North America Region is Largest Market Owing to Technological Advancements and Healthcare Infrastructure

North America is the largest market for microsurgery, driven by the region's advanced healthcare infrastructure, high adoption of robotic surgery, and significant investments in medical technology. The United States, in particular, accounts for a substantial share of the market, thanks to its robust healthcare system, well-established hospitals, and the early adoption of cutting-edge surgical technologies. In addition, North America is home to several key players in the medical device and robotics sectors, contributing to the continued growth of the microsurgery market.

The high demand for precision surgeries, particularly in fields such as neurosurgery and ophthalmic surgery, has fueled the growth of microsurgery in North America. Furthermore, the region benefits from favorable reimbursement policies for robotic-assisted surgeries, making advanced microsurgical procedures more accessible. The presence of leading companies and research institutes in North America also plays a significant role in driving innovation and market expansion.

Competitive Landscape and Leading Companies

The competitive landscape of the microsurgery market is characterized by the presence of several global players who are driving innovation in surgical robotics and microsurgical instruments. Leading companies in the market include Intuitive Surgical, Stryker Corporation, Medtronic, Zimmer Biomet, and Johnson & Johnson, among others. These companies are focusing on technological advancements, product launches, and strategic partnerships to strengthen their market position.

Intuitive Surgical is a market leader in robotic-assisted surgery, with its da Vinci Surgical System being one of the most widely used platforms in microsurgery. Medtronic and Stryker are also prominent players, offering robotic-assisted systems and high-precision instruments for various microsurgical applications. Moreover, companies like Zimmer Biomet and Johnson & Johnson are investing in the development of next-generation robotic systems, further enhancing their competitive edge in the market. The increasing focus on minimally invasive techniques, automation, and precision surgery is expected to intensify competition, prompting companies to continually innovate and expand their product offerings to meet the growing demand for microsurgical procedures globally.

Recent Developments:

- Intuitive Surgical launched the da Vinci SP Surgical System, a next-generation robotic platform designed to increase the precision and scope of microsurgical procedures in various fields such as urology and cardiothoracic surgery.

- Medtronic announced the acquisition of Mazor Robotics, a leader in robotic spinal surgery, expanding its portfolio of robotic-assisted microsurgery systems for orthopedic and neurosurgery applications.

- Zimmer Biomet received regulatory approval from the FDA for its ROSA Spine System, a robotic-assisted technology designed for minimally invasive spinal procedures, enhancing the precision of spinal microsurgery.

- Johnson & Johnson unveiled its Verb Surgical Platform, a fully integrated robotic surgery system that combines robotics, visualization, and data analytics, advancing the capabilities of microsurgeons in critical surgeries.

- Stryker Corporation acquired Mobius Imaging to expand its microsurgery offerings in the field of orthopedics, particularly for minimally invasive spinal and trauma surgeries, enhancing the integration of robotics in surgical procedures.

List of Leading Companies:

- Intuitive Surgical

- Stryker Corporation

- Medtronic

- Zimmer Biomet

- Johnson & Johnson

- Smith & Nephew

- RoboMedica

- TransEnterix

- Mazor Robotics

- Corindus Vascular Robotics

- Brainlab

- Microline Surgical

- KUKA Robotics

- Aurora Surgical

- Accuray Incorporated

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 2.7 Billion |

|

Forecasted Value (2030) |

USD 3.9 Billion |

|

CAGR (2025 – 2030) |

6.4% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Microsurgery Market By Type (Neurosurgery, Ophthalmic Surgery, Orthopedic Surgery, Plastic and Reconstructive Surgery, Cardiothoracic Surgery, Urology Surgery), By Application (Robotic-Assisted Microsurgery, Minimally Invasive Surgery, Traditional Microsurgery, Laser Microsurgery), By End-User (Hospitals, Ambulatory Surgical Centers, Clinics, Research Institutes) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Intuitive Surgical, Stryker Corporation, Medtronic, Zimmer Biomet, Johnson & Johnson, Smith & Nephew, RoboMedica, TransEnterix, Mazor Robotics, Corindus Vascular Robotics, Brainlab, Microline Surgical, KUKA Robotics, Aurora Surgical, Accuray Incorporated |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Microsurgery Market, by Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Neurosurgery |

|

4.2. Ophthalmic Surgery |

|

4.3. Orthopedic Surgery |

|

4.4. Plastic and Reconstructive Surgery |

|

4.5. Cardiothoracic Surgery |

|

4.6. Urology Surgery |

|

5. Microsurgery Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Robotic-Assisted Microsurgery |

|

5.2. Minimally Invasive Surgery |

|

5.3. Traditional Microsurgery |

|

5.4. Laser Microsurgery |

|

6. Microsurgery Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Hospitals |

|

6.2. Ambulatory Surgical Centers (ASCs) |

|

6.3. Clinics |

|

6.4. Research Institutes |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Microsurgery Market, by Type |

|

7.2.7. North America Microsurgery Market, by Application |

|

7.2.8. North America Microsurgery Market, by End-User |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Microsurgery Market, by Type |

|

7.2.9.1.2. US Microsurgery Market, by Application |

|

7.2.9.1.3. US Microsurgery Market, by End-User |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Intuitive Surgical |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Stryker Corporation |

|

9.3. Medtronic |

|

9.4. Zimmer Biomet |

|

9.5. Johnson & Johnson |

|

9.6. Smith & Nephew |

|

9.7. RoboMedica |

|

9.8. TransEnterix |

|

9.9. Mazor Robotics |

|

9.10. Corindus Vascular Robotics |

|

9.11. Brainlab |

|

9.12. Microline Surgical |

|

9.13. KUKA Robotics |

|

9.14. Aurora Surgical |

|

9.15. Accuray Incorporated |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Microsurgery Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Microsurgery Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Microsurgery Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA