As per Intent Market Research, the Microfinance Market was valued at USD 130.2 billion in 2024-e and will surpass USD 319.9 billion by 2030; growing at a CAGR of 16.2% during 2025 - 2030.

The microfinance market is witnessing significant growth as it continues to play a pivotal role in providing financial services to underserved populations and businesses, particularly in emerging economies. Microfinance services, including microloans, microsavings, and microinsurance, offer individuals and small businesses access to capital that would otherwise be unavailable through traditional financial institutions. These services are designed to improve financial inclusion, empower low-income individuals, and promote entrepreneurship. As financial inclusion initiatives gain momentum worldwide, the microfinance sector is expected to expand, offering diverse solutions to meet the financial needs of both individuals and small businesses.

The market is evolving with the increased adoption of digital platforms, enabling more efficient and accessible delivery of microfinance services. Technological advancements, along with the rise of mobile banking and fintech solutions, are reshaping how microfinance products are offered, making them more scalable and accessible. This shift is expected to fuel the continued growth of microfinance, particularly in developing regions where access to traditional banking services remains limited.

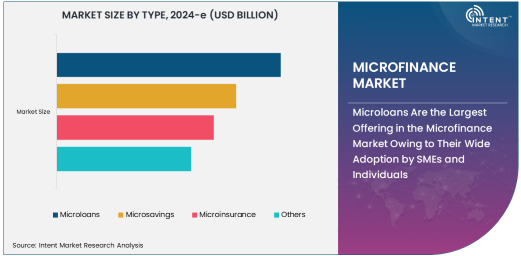

Microloans Are the Largest Offering in the Microfinance Market Owing to Their Wide Adoption by SMEs and Individuals

Microloans dominate the microfinance market, primarily due to their broad adoption by small and medium enterprises (SMEs) and individuals seeking capital to start or grow their businesses. These small loans, typically ranging from a few dollars to a few thousand, are designed to provide working capital to entrepreneurs in underserved regions, where access to traditional banking is limited. Microloans are particularly impactful in fostering economic growth in developing countries by enabling small-scale businesses to access necessary funding.

The success of microloans is driven by their ability to provide financial inclusion and support entrepreneurship in low-income communities. Organizations like Grameen Bank and various microfinance institutions have been instrumental in promoting microloans as an essential tool for alleviating poverty and boosting local economies. With the continued push for financial inclusion, the microloan segment is expected to remain the largest and most influential in the microfinance market.

Direct Lending Is the Fastest Growing Distribution Channel Owing to Increased Access Through Digital Platforms

Direct lending is the fastest-growing distribution channel in the microfinance market, primarily due to the increased access provided by digital platforms. Advances in mobile banking and online lending platforms have enabled direct lenders to reach a larger pool of borrowers, particularly in underserved regions where traditional banking infrastructure is lacking. Digital platforms facilitate the quick disbursement of microloans and other financial services, offering convenience and accessibility to borrowers who would otherwise struggle to access credit.

The rise of peer-to-peer lending and online platforms has further accelerated the growth of direct lending, making it a popular choice for both lenders and borrowers. The ability to process loans quickly and efficiently via digital means has transformed how microfinance services are delivered, expanding their reach and driving the rapid growth of this channel.

Small and Medium Enterprises (SMEs) Are the Largest End-Use Industry Owing to the Growing Need for Capital to Support Business Growth

Small and medium enterprises (SMEs) are the largest end-use industry in the microfinance market, as these businesses are often the primary recipients of microloans and other financial products. SMEs play a critical role in the economic development of many regions, providing jobs and contributing to local economies. However, SMEs frequently face challenges in accessing traditional forms of financing, which makes microfinance a crucial resource for their growth.

Microfinance services, particularly microloans, help SMEs bridge the financing gap by providing them with the capital needed to expand operations, purchase equipment, or cover operating expenses. As governments and institutions continue to emphasize the importance of supporting SMEs, the demand for microfinance products tailored to these businesses is expected to increase.

Asia-Pacific Leads the Market Owing to Expanding Financial Inclusion and Government Initiatives

Asia-Pacific holds the largest share in the microfinance market, driven by the region's significant efforts to enhance financial inclusion and support low-income populations. Countries such as India, Bangladesh, and Indonesia have robust microfinance ecosystems, fueled by strong governmental backing and the presence of well-established microfinance institutions. These nations have introduced various policies and programs to empower small businesses, women entrepreneurs, and rural communities.

The region's high population density and large unbanked segments create a substantial demand for microloans, microsavings, and microinsurance products. The rapid adoption of digital financial services, coupled with increasing investments in fintech solutions, further strengthens the market in Asia-Pacific. This dynamic environment positions the region as a global leader in microfinance.

Leading Companies and Competitive Landscape

The microfinance market is highly competitive, with several key players contributing to the sector’s growth and innovation. Leading companies and organizations in this space include microfinance institutions (MFIs) such as Grameen Bank, SKS Microfinance, and FINCA International, which have established themselves as pioneers in providing microloans and other financial services to underserved populations. Additionally, digital platforms like Kiva, LendingClub, and Branch are reshaping the microfinance landscape by offering innovative solutions that increase accessibility and efficiency in lending.

The competitive landscape is characterized by increasing collaboration between traditional microfinance institutions, fintech startups, and digital platforms. As the demand for financial inclusion grows, companies that can integrate digital technologies with traditional microfinance models will likely gain a competitive edge in the market. Innovation in product offerings, loan repayment mechanisms, and borrower outreach will be key to capturing market share in this rapidly expanding sector.

Recent Developments:

- In November 2024, Grameen Bank expanded its operations into East Africa, providing microloans to rural entrepreneurs. The expansion is expected to create thousands of new jobs in the region.

- In October 2024, Accion International partnered with a leading fintech company to launch a new digital lending platform. This platform aims to provide small loans to underserved communities across Latin America.

- In September 2024, ASA International raised $100 million to fund microfinance initiatives in South Asia. The funds will be used to provide low-interest loans to women entrepreneurs in rural areas.

- In August 2024, Kiva introduced a new feature on its platform allowing users to track the impact of their microloans. This feature aims to increase transparency and accountability in micro-lending.

- In July 2024, Bandhan Bank reached a milestone of 10 million customers in its microfinance division. This expansion highlights the growing demand for microfinance products in India.

List of Leading Companies:

- Grameen Bank

- SKS Microfinance

- Accion International

- FINCA International

- Kiva

- Compartamos Banco

- Advans Group

- ASA International

- MicroCred

- Oikocredit

- Ujjivan Financial Services

- Branch International

- Bandhan Bank

- Pro Mujer

- Aavishkaar Capital

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 130.2 billion |

|

Forecasted Value (2030) |

USD 319.9 billion |

|

CAGR (2025 – 2030) |

16.2% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Microfinance Market By Type (Microloans, Microsavings, Microinsurance), By Distribution Channel (Direct Lending, Microfinance Institutions, Online Platforms, Banks), By End-Use Industry (Small and Medium Enterprises (SMEs), Individuals, Agriculture, Retail) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Grameen Bank, SKS Microfinance, Accion International, FINCA International, Kiva, Compartamos Banco, Advans Group, ASA International, MicroCred, Oikocredit, Ujjivan Financial Services, Branch International, Bandhan Bank, Pro Mujer, Aavishkaar Capital |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Microfinance Market, by Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Microloans |

|

4.2. Microsavings |

|

4.3. Microinsurance |

|

4.4. Others |

|

5. Microfinance Market, by Distribution Channel (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Direct Lending |

|

5.2. Microfinance Institutions |

|

5.3. Online Platforms |

|

5.4. Banks |

|

6. Microfinance Market, by End-Use Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Small and Medium Enterprises (SMEs) |

|

6.2. Individuals |

|

6.3. Agriculture |

|

6.4. Retail |

|

6.5. Others |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Microfinance Market, by Type |

|

7.2.7. North America Microfinance Market, by Distribution Channel |

|

7.2.8. North America Microfinance Market, by End-Use Industry |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Microfinance Market, by Type |

|

7.2.9.1.2. US Microfinance Market, by Distribution Channel |

|

7.2.9.1.3. US Microfinance Market, by End-Use Industry |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Grameen Bank |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. SKS Microfinance |

|

9.3. Accion International |

|

9.4. FINCA International |

|

9.5. Kiva |

|

9.6. Compartamos Banco |

|

9.7. Advans Group |

|

9.8. ASA International |

|

9.9. MicroCred |

|

9.10. Oikocredit |

|

9.11. Ujjivan Financial Services |

|

9.12. Branch International |

|

9.13. Bandhan Bank |

|

9.14. Pro Mujer |

|

9.15. Aavishkaar Capital |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Microfinance Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Microfinance Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Microfinance Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA