As per Intent Market Research, the Microelectronics Market was valued at USD 119.9 billion in 2024-e and will surpass USD 279.6 billion by 2030; growing at a CAGR of 15.2% during 2025 - 2030.

The microelectronics market is a cornerstone of modern technology, driving innovations across a variety of industries, including consumer electronics, automotive, healthcare, and telecommunications. This sector encompasses a wide range of components such as semiconductors, microchips, MEMS (Micro-Electro-Mechanical Systems), and optoelectronics, all of which are integral to the functioning of advanced systems. The ongoing miniaturization of electronic components, coupled with the increasing demand for smarter and more efficient devices, is propelling the growth of the microelectronics market.

Advancements in technologies like artificial intelligence (AI), 5G, and quantum computing are accelerating the demand for high-performance microelectronics. As industries seek to improve efficiency, reduce costs, and enhance user experiences, the microelectronics market will continue to evolve, driving innovation in both consumer products and industrial systems. The expansion of IoT, the growth of connected devices, and the rise of automation are key factors contributing to the growing significance of microelectronics in the global economy.

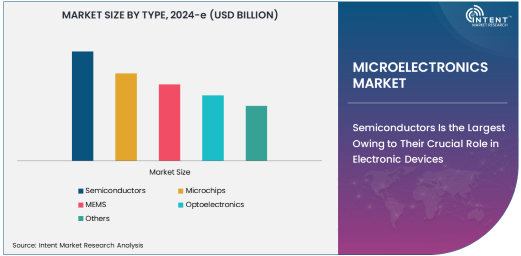

Semiconductors Is the Largest Owing to Their Crucial Role in Electronic Devices

Semiconductors are the largest segment in the microelectronics market, owing to their essential role in the functioning of virtually all modern electronic devices. These materials, which include silicon, gallium arsenide, and other compounds, serve as the backbone of electronic circuits, allowing for signal processing, power management, and data transmission. From smartphones and laptops to automotive systems and industrial machines, semiconductors are crucial for enabling device functionality and performance.

As the demand for more powerful, energy-efficient, and compact devices continues to rise, the semiconductor segment remains the largest in the microelectronics market. With the growth of emerging technologies such as AI, 5G, and IoT, the need for advanced semiconductors is set to increase, further solidifying their position as the dominant segment in the market.

5G Technology Is the Fastest Growing Technology Owing to Global Connectivity Expansion

5G technology is the fastest growing in the technology segment, driven by the ongoing global rollout of 5G networks and the increasing need for high-speed, low-latency communication. 5G technology is revolutionizing various industries by enabling faster data transmission, more reliable connectivity, and the ability to support a larger number of devices simultaneously. This is particularly important in sectors such as telecommunications, healthcare, and industrial automation, where real-time data and seamless communication are crucial.

The expansion of 5G infrastructure is facilitating the development of new applications, such as smart cities, autonomous vehicles, and advanced healthcare solutions, further driving the demand for 5G-enabled microelectronics. As 5G networks continue to expand worldwide, this technology is expected to experience rapid growth, making it the fastest-growing segment in the microelectronics market.

Automotive Is the Largest Application Segment Owing to the Rise of Electric and Autonomous Vehicles

The automotive application segment is the largest in the microelectronics market, driven by the increasing integration of advanced electronics in vehicles. From electric vehicles (EVs) to autonomous driving systems, microelectronics are essential for ensuring the performance, safety, and efficiency of modern vehicles. Semiconductors, sensors, and microchips are used in various automotive systems, including powertrains, infotainment, navigation, and safety features like adaptive cruise control and collision avoidance.

As the automotive industry continues to innovate with electric and autonomous vehicles, the demand for microelectronics will continue to grow. These advancements are leading to the development of more sophisticated vehicle systems that rely heavily on microelectronics, further establishing the automotive sector as the largest application for microelectronics.

Asia Pacific Leads the Microelectronics Market Owing to Robust Manufacturing and Growing Demand

Asia Pacific is the largest region in the microelectronics market, primarily due to its strong manufacturing base and the rapidly increasing demand for electronic devices across various industries. Countries like China, Japan, South Korea, and Taiwan are leaders in semiconductor production, with a well-established infrastructure for the design, fabrication, and testing of microelectronics. The region also benefits from a burgeoning consumer electronics market, which further fuels demand for microelectronic components.

Asia Pacific's dominance in the microelectronics market is supported by its capacity to meet both local and global demand, particularly in consumer electronics, automotive, and telecommunications. As technological advancements continue and industries such as electric vehicles and AI-driven solutions gain momentum, Asia Pacific will maintain its leading role in the global microelectronics market.

Leading Companies and Competitive Landscape

The microelectronics market is highly competitive, with several global players driving innovation and shaping the future of the industry. Leading companies include Intel, Samsung Electronics, TSMC (Taiwan Semiconductor Manufacturing Company), Qualcomm, and Broadcom, which are at the forefront of developing cutting-edge semiconductor technologies and microelectronic components. These companies focus on continuous innovation to address the growing demand for more powerful, efficient, and compact devices.

The competitive landscape is characterized by rapid technological advancements, strategic partnerships, and investments in research and development. As the market continues to evolve, companies are also focusing on expanding their portfolios to include emerging technologies such as AI, quantum computing, and 5G, which are expected to drive the next wave of growth in the microelectronics sector. Competition is intense, and the ability to stay ahead in terms of technological capabilities and manufacturing efficiency will be key to maintaining market leadership.

Recent Developments:

- In December 2024, Intel Corporation announced the launch of its new 7nm chip technology. The company aims to improve computing speeds and efficiency for data centers and cloud applications.

- In November 2024, Qualcomm Inc. unveiled a next-generation microprocessor for 5G-enabled devices. This chip is expected to enhance mobile device performance and power efficiency.

- In October 2024, TSMC (Taiwan Semiconductor Manufacturing Company) started production of its 3nm semiconductor chips. This move is set to lead to better energy efficiency and higher performance in smartphones and laptops.

- In September 2024, Micron Technology, Inc. introduced high-performance DRAM memory for AI applications. This new product will cater to the growing demand for faster and more reliable memory solutions in artificial intelligence.

- In August 2024, NXP Semiconductors announced a collaboration with a leading automotive company to develop microelectronic solutions for self-driving cars. This collaboration aims to enhance vehicle safety and performance through advanced electronics.

List of Leading Companies:

- Intel Corporation

- Samsung Electronics

- TSMC (Taiwan Semiconductor Manufacturing Company)

- Qualcomm Inc.

- Texas Instruments

- Broadcom Inc.

- NXP Semiconductors

- Analog Devices, Inc.

- STMicroelectronics

- Micron Technology, Inc.

- Infineon Technologies AG

- Advanced Micro Devices, Inc. (AMD)

- MediaTek Inc.

- ON Semiconductor Corporation

- Renesas Electronics Corporation

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 119.9 billion |

|

Forecasted Value (2030) |

USD 279.6 billion |

|

CAGR (2025 – 2030) |

15.2% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Microelectronics Market By Type (Semiconductors, Microchips, MEMS (Micro-Electro-Mechanical Systems), Optoelectronics), By Technology (Quantum Computing, AI Integration, 5G Technology, Nanoelectronics), By Application (Consumer Electronics, Automotive, Industrial Automation, Telecommunications, Healthcare, Aerospace & Defense) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Intel Corporation, Samsung Electronics, TSMC (Taiwan Semiconductor Manufacturing Company), Qualcomm Inc., Texas Instruments, Broadcom Inc., NXP Semiconductors, Analog Devices, Inc., STMicroelectronics, Micron Technology, Inc., Infineon Technologies AG, Advanced Micro Devices, Inc. (AMD), MediaTek Inc., ON Semiconductor Corporation, Renesas Electronics Corporation |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Microelectronics Market, by Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Semiconductors |

|

4.2. Microchips |

|

4.3. MEMS (Micro-Electro-Mechanical Systems) |

|

4.4. Optoelectronics |

|

4.5. Others |

|

5. Microelectronics Market, by Technology (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Quantum Computing |

|

5.2. AI Integration |

|

5.3. 5G Technology |

|

5.4. Nanoelectronics |

|

5.5. Others |

|

6. Microelectronics Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Consumer Electronics |

|

6.2. Automotive |

|

6.3. Industrial Automation |

|

6.4. Telecommunications |

|

6.5. Healthcare |

|

6.6. Aerospace & Defense |

|

6.7. Others |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Microelectronics Market, by Type |

|

7.2.7. North America Microelectronics Market, by Technology |

|

7.2.8. North America Microelectronics Market, by Application |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Microelectronics Market, by Type |

|

7.2.9.1.2. US Microelectronics Market, by Technology |

|

7.2.9.1.3. US Microelectronics Market, by Application |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Intel Corporation |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Samsung Electronics |

|

9.3. TSMC (Taiwan Semiconductor Manufacturing Company) |

|

9.4. Qualcomm Inc. |

|

9.5. Texas Instruments |

|

9.6. Broadcom Inc. |

|

9.7. NXP Semiconductors |

|

9.8. Analog Devices, Inc. |

|

9.9. STMicroelectronics |

|

9.10. Micron Technology, Inc. |

|

9.11. Infineon Technologies AG |

|

9.12. Advanced Micro Devices, Inc. (AMD) |

|

9.13. MediaTek Inc. |

|

9.14. ON Semiconductor Corporation |

|

9.15. Renesas Electronics Corporation |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Microelectronics Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Microelectronics Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Microelectronics Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA