As per Intent Market Research, the Microcontroller Market was valued at USD 21.9 billion in 2024-e and will surpass USD 49.9 billion by 2030; growing at a CAGR of 14.7% during 2025 - 2030.

The microcontroller market is witnessing substantial growth, driven by the increasing adoption of embedded systems across various industries. Microcontrollers serve as the central processing units for embedded devices, making them integral to applications in automotive, consumer electronics, industrial automation, medical devices, and telecommunications. With the rise of the Internet of Things (IoT) and advancements in smart technologies, the demand for microcontrollers is expected to continue its upward trajectory, powered by the need for more intelligent and efficient systems.

The market is segmented by type, architecture, and application, each offering different growth opportunities. The diversity in architecture and processing capabilities of microcontrollers ensures they can meet the unique needs of different industries, ranging from simple control functions to complex data processing. As new applications emerge, the microcontroller market is becoming increasingly specialized, fostering innovation and competition among key players.

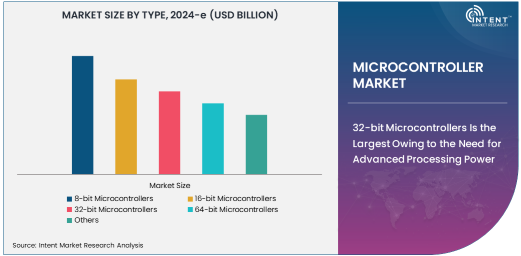

32-bit Microcontrollers Is the Largest Owing to the Need for Advanced Processing Power

In the type segment, 32-bit microcontrollers dominate the market due to their high processing power and versatility, which make them suitable for a wide range of applications. These microcontrollers are essential in industries requiring more complex computations and faster processing speeds, such as automotive, industrial automation, and consumer electronics. Their ability to handle larger data sets and perform complex control functions makes them the preferred choice for modern embedded systems.

As industries demand more sophisticated devices, particularly in IoT, AI, and automation, 32-bit microcontrollers are becoming increasingly integral to meeting these needs. Their adoption is expected to continue growing as more devices require greater performance, reliability, and power efficiency, solidifying their position as the largest subsegment in the market.

Harvard Architecture Is the Fastest Growing Owing to Its High Performance in Embedded Systems

Harvard architecture is the fastest growing in the architecture segment due to its ability to separate data and instruction memory, enabling more efficient data processing. This architecture is particularly advantageous in real-time systems and applications that require high-speed processing, such as automotive, telecommunications, and medical devices. The Harvard architecture offers faster execution and greater efficiency compared to other architectures, making it ideal for applications with strict performance requirements.

The rise of complex embedded systems, including those used in automotive control systems, robotics, and medical equipment, is driving the growth of Harvard architecture. As the demand for high-performance, real-time applications increases, Harvard architecture microcontrollers are expected to see rapid adoption, positioning them as the fastest-growing architecture in the microcontroller market.

Automotive Is the Largest Application Segment Owing to the Rise of Smart Vehicles

The automotive application segment is the largest in the microcontroller market, driven by the increasing integration of advanced driver-assistance systems (ADAS), infotainment systems, and electric vehicle (EV) technologies. Microcontrollers are at the heart of these innovations, enabling complex functionalities such as vehicle control, safety systems, and communication interfaces. As the automotive industry continues to evolve towards electric and autonomous vehicles, the demand for microcontrollers with enhanced processing power and reliability is growing.

Moreover, the need for energy-efficient and robust systems in the automotive sector is further driving the adoption of microcontrollers. With the ongoing development of self-driving cars and the rise in the number of electric vehicles on the road, automotive applications are expected to remain the largest driver of microcontroller demand.

Asia Pacific Leads the Microcontroller Market Owing to Manufacturing Hub and Growing Demand

Asia Pacific is the largest region in the microcontroller market, owing to its role as a major manufacturing hub for electronic components and the rapidly growing demand for microcontrollers in various applications. The region is home to key manufacturing countries such as China, Japan, South Korea, and Taiwan, which collectively dominate the global supply chain for microcontroller production. Additionally, the increasing adoption of consumer electronics, automotive innovations, and industrial automation in the region is fueling market growth.

The region’s cost-effective production capabilities and the increasing demand for high-performance microcontrollers in sectors like automotive and consumer electronics make Asia Pacific a key player in the global microcontroller market. As these industries continue to grow, Asia Pacific is expected to maintain its dominance and drive the market's expansion.

Leading Companies and Competitive Landscape

The microcontroller market is highly competitive, with several global players striving for leadership through technological innovation and strategic collaborations. Key players include NXP Semiconductors, Microchip Technology, STMicroelectronics, Texas Instruments, and Renesas Electronics, all of which offer a wide range of microcontrollers across different segments. These companies focus on advancing processing power, energy efficiency, and connectivity capabilities to meet the growing demand for smart, connected devices.

The competitive landscape is marked by continuous advancements in microcontroller performance, with companies investing heavily in research and development. Strategic partnerships with automotive, consumer electronics, and industrial automation companies are also common, as market leaders aim to position themselves as integral components of the evolving IoT and automation ecosystems. As the market continues to grow, companies are increasingly focused on delivering tailored solutions for specific industry needs, fostering both competition and collaboration in the space.

Recent Developments:

- In November 2024, Microchip Technology announced the launch of its new family of 32-bit microcontrollers. These microcontrollers are designed to meet the growing needs of automotive and industrial automation applications.

- In October 2024, NXP Semiconductors introduced a new series of microcontrollers aimed at enhancing security for IoT devices. This move underscores NXP's push to lead in the growing IoT market.

- In September 2024, STMicroelectronics expanded its microcontroller portfolio with a focus on energy-efficient solutions for industrial applications. This expansion is expected to cater to the increasing demand for automation and robotics.

- In August 2024, Renesas Electronics unveiled its new automotive-grade microcontroller. The microcontroller is designed to support advanced driver-assistance systems (ADAS) in the next generation of vehicles.

- In July 2024, Texas Instruments announced a new microcontroller that integrates both analog and digital capabilities. This product is aimed at simplifying designs in industrial automation systems.

List of Leading Companies:

- Intel Corporation

- NXP Semiconductors

- Microchip Technology Incorporated

- STMicroelectronics

- Texas Instruments

- Renesas Electronics Corporation

- Analog Devices, Inc.

- Infineon Technologies AG

- ON Semiconductor

- Cypress Semiconductor

- Toshiba Corporation

- Silicon Labs

- MediaTek Inc.

- Broadcom Inc.

- Maxim Integrated Products

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 21.9 billion |

|

Forecasted Value (2030) |

USD 49.9 billion |

|

CAGR (2025 – 2030) |

14.7% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Microcontroller Market By Type (8-bit Microcontrollers, 16-bit Microcontrollers, 32-bit Microcontrollers, 64-bit Microcontrollers), By Architecture (Harvard Architecture, Von Neumann Architecture, Modified Harvard Architecture), By Application (Automotive, Consumer Electronics, Industrial Automation, Medical Devices, Telecommunications) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Intel Corporation, NXP Semiconductors, Microchip Technology Incorporated, STMicroelectronics, Texas Instruments, Renesas Electronics Corporation, Analog Devices, Inc., Infineon Technologies AG, ON Semiconductor, Cypress Semiconductor, Toshiba Corporation, Silicon Labs, MediaTek Inc., Broadcom Inc., Maxim Integrated Products |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Microcontroller Market, by Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. 8-bit Microcontrollers |

|

4.2. 16-bit Microcontrollers |

|

4.3. 32-bit Microcontrollers |

|

4.4. 64-bit Microcontrollers |

|

4.5. Others |

|

5. Microcontroller Market, by Architecture (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Harvard Architecture |

|

5.2. Von Neumann Architecture |

|

5.3. Modified Harvard Architecture |

|

5.4. Others |

|

6. Microcontroller Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Automotive |

|

6.2. Consumer Electronics |

|

6.3. Industrial Automation |

|

6.4. Medical Devices |

|

6.5. Telecommunications |

|

6.6. Others |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Microcontroller Market, by Type |

|

7.2.7. North America Microcontroller Market, by Architecture |

|

7.2.8. North America Microcontroller Market, by Application |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Microcontroller Market, by Type |

|

7.2.9.1.2. US Microcontroller Market, by Architecture |

|

7.2.9.1.3. US Microcontroller Market, by Application |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Intel Corporation |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. NXP Semiconductors |

|

9.3. Microchip Technology Incorporated |

|

9.4. STMicroelectronics |

|

9.5. Texas Instruments |

|

9.6. Renesas Electronics Corporation |

|

9.7. Analog Devices, Inc. |

|

9.8. Infineon Technologies AG |

|

9.9. ON Semiconductor |

|

9.10. Cypress Semiconductor |

|

9.11. Toshiba Corporation |

|

9.12. Silicon Labs |

|

9.13. MediaTek Inc. |

|

9.14. Broadcom Inc. |

|

9.15. Maxim Integrated Products |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Microcontroller Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Microcontroller Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Microcontroller Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA