As per Intent Market Research, the Micro Motor Market was valued at USD 3.4 billion in 2024-e and will surpass USD 7.8 billion by 2030; growing at a CAGR of 14.7% during 2025 - 2030.

The micro motor market is expanding rapidly, driven by the increasing demand for small, efficient, and versatile motors across various industries. Micro motors, due to their compact size and high performance, are critical components in a wide range of applications, including consumer electronics, automotive, industrial automation, medical devices, and robotics. The need for miniaturization, energy efficiency, and improved performance in electronic devices, machinery, and robotics is fueling the growth of the micro motor market. As industries continue to evolve, the demand for motors that can operate in small, confined spaces while delivering high torque and speed is pushing technological advancements in micro motor designs.

Moreover, the growth of electric vehicles, advancements in robotics, and the increasing adoption of automation in manufacturing processes are further boosting the demand for micro motors. With the rise of IoT-enabled devices and the expansion of the medical device industry, the market for micro motors is expected to continue its upward trajectory, driven by the need for precision, reliability, and energy-efficient solutions across various applications.

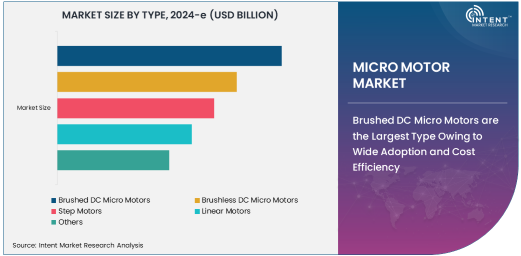

Brushed DC Micro Motors are the Largest Type Owing to Wide Adoption and Cost Efficiency

Brushed DC micro motors dominate the micro motor market due to their wide adoption, cost efficiency, and simple design. These motors are commonly used in consumer electronics, automotive applications, and other devices that require reliable and efficient performance at a relatively low cost. The brushed DC micro motors offer a straightforward mechanism with a commutator and brushes to provide a rotating motion, making them easy to design and integrate into a variety of products. Their low manufacturing cost and ease of control make them the preferred choice for mass-produced devices and applications where space and cost constraints are critical.

Brushed DC motors are typically used in applications like electric fans, vacuum cleaners, toys, and small home appliances, where high reliability and durability are required. Their widespread use across various sectors, including automotive for window lifts and small pumps, makes brushed DC micro motors the largest type within the market. With advances in materials and production techniques, the performance and lifespan of these motors have also been enhanced, ensuring their continued dominance in the micro motor space.

Battery-Powered Micro Motors Are the Fastest Growing Power Source Due to Increased Portability Needs

Battery-powered micro motors are the fastest growing power source segment in the market, primarily due to the rising demand for portable and energy-efficient devices. With the growing use of mobile electronics, wearables, and robotics, battery-powered motors offer the advantage of portability, making them ideal for applications where access to external power sources is limited or not feasible. These motors are widely used in handheld devices such as electric toothbrushes, portable fans, and mobile robotics, as well as in medical devices such as hearing aids and infusion pumps. Battery-powered motors are especially popular in consumer electronics, where devices are expected to be lightweight and efficient.

The growth of the battery-powered segment is further supported by advancements in battery technology, which are extending the operational life and performance of battery-operated devices. As manufacturers continue to innovate and produce smaller, more efficient batteries, the demand for battery-powered micro motors is expected to increase, particularly in emerging applications such as wearables and autonomous robots. With the rise of the Internet of Things (IoT) and the proliferation of smart devices, battery-powered micro motors will continue to see strong growth in the coming years.

Medical Devices Drive Application Growth Owing to Precision and Reliability Requirements

The medical devices application segment is one of the fastest growing in the micro motor market, driven by the need for high precision, reliability, and miniaturization in medical equipment. Micro motors are integral to medical devices such as surgical tools, dental equipment, infusion pumps, and diagnostic instruments, where compact size and precise control are essential. In applications like dental drills and robotic-assisted surgery, the performance of micro motors directly impacts the accuracy and effectiveness of the procedures. As the medical device industry focuses on enhancing patient care through innovative technologies, the demand for micro motors that can operate efficiently in small, intricate devices continues to rise.

The trend towards wearable medical devices, such as insulin pumps and hearing aids, further fuels the demand for small, reliable micro motors. These devices require motors that are not only energy-efficient but also capable of operating under stringent medical standards. As the global healthcare market continues to grow and evolve, micro motors will play an increasingly vital role in advancing medical technology, ensuring the continued expansion of this application segment.

Asia Pacific Leads the Market Owing to Manufacturing Excellence and Demand for Consumer Electronics

Asia Pacific is the leading region in the micro motor market, driven by the region's strong manufacturing base, technological advancements, and high demand for consumer electronics. Countries like China, Japan, and South Korea are key players in the production of micro motors, with a significant number of companies engaged in the development of efficient and cost-effective solutions for a wide range of applications. The region’s robust automotive and industrial automation sectors also contribute to the strong demand for micro motors.

The growth of the Asia Pacific micro motor market is further supported by the increasing consumption of consumer electronics, such as smartphones, wearables, and home appliances, where micro motors are crucial components. As the adoption of robotics, electric vehicles, and IoT-based devices expands, the demand for micro motors continues to grow in the region. Additionally, the increasing focus on advanced manufacturing techniques and the push towards energy-efficient solutions are expected to sustain Asia Pacific’s leadership position in the global micro motor market.

Leading Companies and Competitive Landscape

The micro motor market is highly competitive, with several key players leading the charge in innovation and market penetration. Prominent companies such as Nidec Corporation, Maxon Motor AG, and Mabuchi Motor Co., Ltd. are major players in the market, providing a wide range of micro motors for applications across consumer electronics, automotive, industrial automation, and medical devices. These companies are focused on advancing motor efficiency, miniaturization, and integration with emerging technologies like robotics and IoT.

In addition to traditional motor manufacturers, companies like Johnson Electric and Precision Microdrives are making significant strides in providing specialized micro motors for niche applications, including medical and robotic technologies. The market is also seeing increased collaborations and partnerships between micro motor manufacturers and technology providers to enhance motor capabilities and develop solutions for next-generation applications. As the demand for small, energy-efficient, and high-performance motors continues to rise, competition will intensify, driving further innovation and technological advancements in the micro motor market.

Recent Developments:

- In November 2024, Nidec Corporation launched a new brushless DC micro motor for industrial automation applications.

- In October 2024, Maxon Motor expanded its production facility to meet rising demand for precision micro motors in robotics.

- In September 2024, Siemens AG introduced a new line of stepper motors aimed at medical device applications.

- In August 2024, Johnson Electric developed a new energy-efficient micro motor for automotive systems.

- In July 2024, MinebeaMitsumi announced the release of a compact linear motor for consumer electronics.

List of Leading Companies:

- Nidec Corporation

- Maxon Motor

- Faulhaber Group

- Allied Motion Technologies Inc.

- Johnson Electric

- Mabuchi Motor Co., Ltd.

- MinebeaMitsumi Inc.

- Buehler Motor GmbH

- Portescap

- Mclennan

- Siemens AG

- Harmonic Drive Systems

- Kontron

- Ametek Inc.

- Linix Motor Co., Ltd.

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 3.4 billion |

|

Forecasted Value (2030) |

USD 7.8 billion |

|

CAGR (2025 – 2030) |

14.7% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Micro Motor Market By Type (Brushed DC Micro Motors, Brushless DC Micro Motors, Step Motors, Linear Motors), By Power Source (Battery-Powered, AC Powered, DC Powered), By Application (Consumer Electronics, Automotive, Industrial Automation, Medical Devices, Robotics) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Nidec Corporation, Maxon Motor, Faulhaber Group, Allied Motion Technologies Inc., Johnson Electric, Mabuchi Motor Co., Ltd., MinebeaMitsumi Inc., Buehler Motor GmbH, Portescap, Mclennan, Siemens AG, Harmonic Drive Systems, Kontron, Ametek Inc., Linix Motor Co., Ltd. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Micro Motor Market, by Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Brushed DC Micro Motors |

|

4.2. Brushless DC Micro Motors |

|

4.3. Step Motors |

|

4.4. Linear Motors |

|

4.5. Others |

|

5. Micro Motor Market, by Power Source (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Battery-Powered |

|

5.2. AC Powered |

|

5.3. DC Powered |

|

5.4. Others |

|

6. Micro Motor Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Consumer Electronics |

|

6.2. Automotive |

|

6.3. Industrial Automation |

|

6.4. Medical Devices |

|

6.5. Robotics |

|

6.6. Others |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Micro Motor Market, by Type |

|

7.2.7. North America Micro Motor Market, by Power Source |

|

7.2.8. North America Micro Motor Market, by Application |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Micro Motor Market, by Type |

|

7.2.9.1.2. US Micro Motor Market, by Power Source |

|

7.2.9.1.3. US Micro Motor Market, by Application |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Nidec Corporation |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Maxon Motor |

|

9.3. Faulhaber Group |

|

9.4. Allied Motion Technologies Inc. |

|

9.5. Johnson Electric |

|

9.6. Mabuchi Motor Co., Ltd. |

|

9.7. MinebeaMitsumi Inc. |

|

9.8. Buehler Motor GmbH |

|

9.9. Portescap |

|

9.10. Mclennan |

|

9.11. Siemens AG |

|

9.12. Harmonic Drive Systems |

|

9.13. Kontron |

|

9.14. Ametek Inc. |

|

9.15. Linix Motor Co., Ltd. |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Micro Motor Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Micro Motor Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Micro Motor Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA