As per Intent Market Research, the Lysosomal Alpha Glucosidase Market was valued at USD 2.3 Billion in 2024-e and will surpass USD 5.0 Billion by 2030; growing at a CAGR of 13.7% during 2025-2030.

The Lysosomal Alpha Glucosidase market is a growing sector within the rare disease treatment landscape, driven by advancements in therapeutic approaches and increased awareness of lysosomal storage disorders. The market addresses conditions like Pompe disease, characterized by alpha-glucosidase enzyme deficiency, which leads to the accumulation of glycogen in cells, affecting muscular and systemic functions. With innovations in enzyme replacement and gene therapy, coupled with expanded diagnosis rates, the market is poised for significant growth in the coming years.

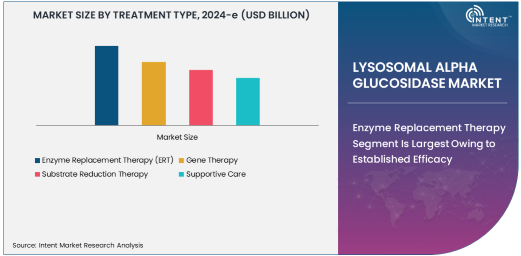

Enzyme Replacement Therapy Segment Is Largest Owing to Established Efficacy

Enzyme Replacement Therapy (ERT) remains the largest treatment type segment due to its proven efficacy and widespread adoption for managing Pompe disease. ERT involves supplementing the deficient enzyme, which effectively reduces glycogen accumulation in affected patients. Established products like alglucosidase alfa have demonstrated a significant improvement in patient outcomes, particularly for early-diagnosed individuals.

The dominance of ERT is further reinforced by consistent regulatory approvals and ongoing research to enhance treatment efficiency. With an increasing number of patients receiving early diagnoses, the adoption of ERT is expected to sustain its market leadership, especially in developed regions with advanced healthcare infrastructure.

Late-Onset Pompe Disease Segment Is Fastest Growing Due to Rising Diagnosis Rates

Late-Onset Pompe Disease (LOPD) is emerging as the fastest-growing segment in the indication category. LOPD manifests later in life and is often misdiagnosed as other neuromuscular disorders. However, advancements in diagnostic technologies and awareness campaigns have significantly improved identification rates.

The growing availability of targeted therapies for LOPD is driving this segment’s rapid expansion. Pharmaceutical companies are increasingly investing in clinical trials for therapies specific to LOPD, highlighting the growing recognition of this condition's unique needs within the broader Pompe disease spectrum.

Oral Route of Administration Segment Is Fastest Growing Due to Patient Preference

The oral route of administration is witnessing the fastest growth due to the convenience it offers compared to intravenous methods. Oral therapies, while still in early development stages, are gaining traction for their potential to improve patient compliance and quality of life.

This growth is supported by innovations in substrate reduction therapies delivered orally. Companies are actively exploring oral formulations to cater to patients who may not have access to intravenous administration facilities or prefer less invasive options.

Hospitals Segment Is Largest Owing to Centralized Care Delivery

Hospitals represent the largest segment in the end-user category, driven by their role as primary care centers for administering therapies like ERT and managing Pompe disease patients. Hospitals often house multidisciplinary teams equipped to handle the complex needs of lysosomal storage disorder patients, making them a preferred choice for treatment.

Moreover, hospitals are typically the first point of contact for patients seeking diagnosis and treatment, reinforcing their dominance in the market. Expanding hospital infrastructure and the availability of specialized care in developed regions further contribute to this segment’s leadership.

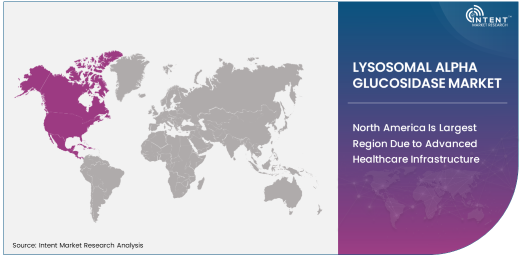

North America Is Largest Region Due to Advanced Healthcare Infrastructure

North America dominates the lysosomal alpha glucosidase market, supported by robust healthcare infrastructure, high diagnosis rates, and significant R&D investments. The presence of leading pharmaceutical companies and widespread access to advanced therapies further bolster the region's leadership.

The United States, in particular, drives this growth with substantial government and private sector funding for rare disease research. Efforts to increase awareness and improve accessibility to treatments ensure North America remains a pivotal market for lysosomal alpha glucosidase therapies.

Leading Companies and Competitive Landscape

The competitive landscape of the lysosomal alpha glucosidase market is characterized by a strong focus on innovation and strategic collaborations. Key players like Sanofi, Amicus Therapeutics, and Genzyme Corporation are leading the way with established products and a robust pipeline of advanced therapies. Emerging companies like Spark Therapeutics and Ultragenyx Pharmaceutical are further intensifying competition by introducing novel approaches such as gene therapy.

Collaborations between biopharmaceutical companies and research institutes, along with M&A activities, are shaping the market dynamics. With a growing emphasis on personalized medicine and targeted treatments, the competitive landscape is expected to remain dynamic in the coming years.

Recent Developments:

- Sanofi launched Nexviazyme, an advanced enzyme replacement therapy for Pompe disease, enhancing its therapeutic portfolio

- Amicus Therapeutics announced FDA approval for AT-GAA, a next-generation therapy for LOPD

- Spark Therapeutics initiated clinical trials for a gene therapy targeting infantile-onset Pompe disease

- Ultragenyx Pharmaceutical acquired rights for a novel substrate reduction therapy for lysosomal storage disorders

- Pfizer expanded its rare disease research unit with investments in lysosomal storage disease therapies

List of Leading Companies:

- Pfizer Inc.

- Merck & Co., Inc.

- GlaxoSmithKline plc (GSK)

- Sanofi

- AstraZeneca

- Johnson & Johnson

- Novartis AG

- F. Hoffmann-La Roche Ltd

- Eli Lilly and Company

- Bayer AG

- Amgen Inc.

- Bristol Myers Squibb

- Takeda Pharmaceutical Company

- AbbVie Inc.

- CSL Behring

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 2.3 Billion |

|

Forecasted Value (2030) |

USD 5.0 Billion |

|

CAGR (2025 – 2030) |

13.7% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Lysosomal Alpha Glucosidase Market By Treatment Type (Enzyme Replacement Therapy, Gene Therapy, Substrate Reduction Therapy, Supportive Care), By Indication (Infantile-Onset Pompe Disease, Late-Onset Pompe Disease), By Route of Administration (Intravenous, Oral), By End-User (Hospitals, Specialty Clinics, Research Institutes, Homecare Settings) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Pfizer Inc., Merck & Co., Inc., GlaxoSmithKline plc (GSK), Sanofi, AstraZeneca, Johnson & Johnson, Novartis AG, F. Hoffmann-La Roche Ltd, Eli Lilly and Company, Bayer AG, Amgen Inc., Bristol Myers Squibb, Takeda Pharmaceutical Company, AbbVie Inc., CSL Behring |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Lysosomal Alpha Glucosidase Market, by Treatment Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Enzyme Replacement Therapy (ERT) |

|

4.2. Gene Therapy |

|

4.3. Substrate Reduction Therapy |

|

4.4. Supportive Care |

|

5. Lysosomal Alpha Glucosidase Market, by Indication (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Infantile-Onset Pompe Disease (IOPD) |

|

5.2. Late-Onset Pompe Disease (LOPD) |

|

6. Lysosomal Alpha Glucosidase Market, by Route of Administration (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Intravenous |

|

6.2. Oral |

|

7. Lysosomal Alpha Glucosidase Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Hospitals |

|

7.2. Specialty Clinics |

|

7.3. Research Institutes |

|

7.4. Homecare Settings |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Lysosomal Alpha Glucosidase Market, by Treatment Type |

|

8.2.7. North America Lysosomal Alpha Glucosidase Market, by Indication |

|

8.2.8. North America Lysosomal Alpha Glucosidase Market, by Route of Administration |

|

8.2.9. North America Lysosomal Alpha Glucosidase Market, by End-User |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Lysosomal Alpha Glucosidase Market, by Treatment Type |

|

8.2.10.1.2. US Lysosomal Alpha Glucosidase Market, by Indication |

|

8.2.10.1.3. US Lysosomal Alpha Glucosidase Market, by Route of Administration |

|

8.2.10.1.4. US Lysosomal Alpha Glucosidase Market, by End-User |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Pfizer Inc. |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Merck & Co., Inc. |

|

10.3. GlaxoSmithKline plc (GSK) |

|

10.4. Sanofi |

|

10.5. AstraZeneca |

|

10.6. Johnson & Johnson |

|

10.7. Novartis AG |

|

10.8. F. Hoffmann-La Roche Ltd |

|

10.9. Eli Lilly and Company |

|

10.10. Bayer AG |

|

10.11. Amgen Inc. |

|

10.12. Bristol Myers Squibb |

|

10.13. Takeda Pharmaceutical Company |

|

10.14. AbbVie Inc. |

|

10.15. CSL Behring |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Lysosomal Alpha Glucosidase Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Lysosomal Alpha Glucosidase Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Lysosomal Alpha Glucosidase Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA