As per Intent Market Research, the Lung Cancer Diagnostic and Screening Market was valued at USD 1.8 Billion in 2024-e and will surpass USD 2.6 Billion by 2030; growing at a CAGR of 6.4% during 2025-2030.

The lung cancer diagnostic and screening market has gained significant momentum due to the increasing incidence of lung cancer globally and the growing demand for early detection. Lung cancer remains one of the leading causes of cancer-related deaths, making early diagnosis crucial for improving survival rates. As technologies in imaging, molecular diagnostics, and genetic testing continue to advance, the market is poised for substantial growth. The ongoing development of non-invasive diagnostic methods and the growing adoption of personalized medicine are driving the demand for more efficient and accurate screening solutions in both clinical and research settings.

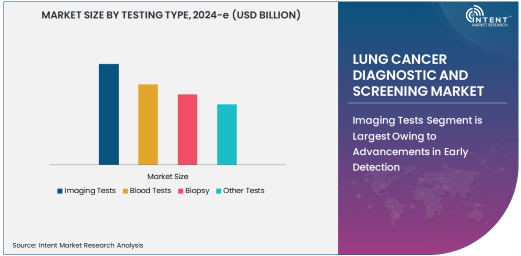

Imaging Tests Segment is Largest Owing to Advancements in Early Detection

Imaging tests are the largest subsegment in the lung cancer diagnostic market, primarily due to their ability to detect cancer in its early stages and provide detailed visualizations of the lung’s structure. Technologies such as computed tomography (CT) scans, X-rays, and magnetic resonance imaging (MRI) are widely used for screening and diagnosing lung cancer. The non-invasive nature of these tests, along with their established role in clinical practice, has made them the go-to diagnostic tool for lung cancer detection. Furthermore, advancements in imaging technologies, such as low-dose CT scans, have improved their accuracy and sensitivity, making them an essential part of lung cancer screening programs, especially for high-risk populations such as smokers or individuals with a family history of lung cancer.

The growing adoption of advanced imaging technologies, including AI-powered imaging systems, is expected to further enhance the precision of lung cancer detection. With the introduction of newer methods that combine imaging with genetic and molecular diagnostics, imaging tests are becoming even more effective in identifying tumors at earlier stages. These advancements make imaging tests indispensable in the fight against lung cancer, further solidifying their dominant position in the market.

Molecular Diagnostics Segment is Fastest Growing Due to Personalized Medicine

Molecular diagnostics is the fastest-growing subsegment within the lung cancer diagnostic market, driven by the increasing shift towards personalized medicine. Molecular diagnostics involves analyzing genetic mutations, biomarkers, and other molecular characteristics of cancer cells, providing insights that help tailor treatment plans to individual patients. This personalized approach is particularly important in lung cancer, where tumor genetics can vary widely between patients, influencing the efficacy of treatments. The ability to detect specific mutations such as EGFR, ALK, and ROS1 has revolutionized treatment options, allowing oncologists to offer targeted therapies that are more effective and cause fewer side effects compared to traditional chemotherapy.

The rapid growth of molecular diagnostics in lung cancer detection is also fueled by the increasing availability of advanced testing platforms that can perform next-generation sequencing (NGS) and liquid biopsy testing. These technologies not only allow for more comprehensive and accurate diagnostic information but also reduce the need for invasive procedures like biopsies, thus improving patient comfort and outcomes. As the demand for more precise, targeted treatments continues to rise, the molecular diagnostics segment is expected to grow rapidly in the coming years.

Hospitals Segment is Largest End-User Due to High Patient Volume

Hospitals remain the largest end-user in the lung cancer diagnostic market, driven by their central role in diagnosing and treating cancer. Hospitals are equipped with state-of-the-art diagnostic tools, including imaging systems, biopsy services, and molecular diagnostic tests, making them the primary location for lung cancer screening and diagnosis. The large patient population seeking diagnosis and treatment in hospitals contributes significantly to the market size, with hospitals offering a wide range of diagnostic services for early detection of lung cancer.

Moreover, hospitals are increasingly adopting advanced technologies like AI-assisted diagnostic systems and robotic surgery for lung cancer treatment, enhancing their diagnostic capabilities. This adoption, coupled with the rising burden of cancer globally, is expected to further drive the demand for lung cancer diagnostic services in hospitals. The comprehensive care provided by hospitals, from diagnostic testing to treatment and rehabilitation, solidifies their dominant position in the market.

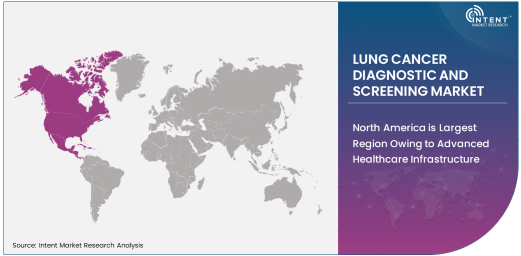

North America is Largest Region Owing to Advanced Healthcare Infrastructure

North America is the largest region in the lung cancer diagnostic and screening market, with the United States leading the way due to its advanced healthcare infrastructure and high adoption rate of cutting-edge diagnostic technologies. The growing incidence of lung cancer, coupled with increasing government initiatives for cancer screening, contributes to the region’s market leadership. Furthermore, North America benefits from a high level of healthcare expenditure, ensuring that healthcare facilities are well-equipped with the latest diagnostic tools and technologies.

The region also has a well-established network of hospitals, oncology centers, and diagnostic laboratories, driving the demand for lung cancer screening and diagnostic services. The widespread awareness about the importance of early detection and the availability of reimbursement for diagnostic tests further supports the growth of the market. With continuous advancements in diagnostic technologies, North America is expected to maintain its dominant position in the lung cancer diagnostic market for the foreseeable future.

Competitive Landscape and Leading Companies

The lung cancer diagnostic and screening market is highly competitive, with a mix of established players and emerging companies. Leading companies in the market include Roche Diagnostics, Illumina, GE Healthcare, Abbott Laboratories, and Siemens Healthineers, which offer a wide range of diagnostic solutions, from imaging tests to molecular diagnostics. These companies are continuously innovating to expand their product portfolios and enhance the accuracy and efficiency of their diagnostic technologies.

The competitive landscape is marked by strategic collaborations, mergers and acquisitions, and investments in research and development. Companies are focusing on expanding their presence in emerging markets, where the demand for advanced diagnostic solutions is increasing. Moreover, the integration of AI and machine learning into diagnostic platforms is a key area of focus, helping companies stay ahead of the curve in offering more precise and efficient diagnostic tools. As the demand for early lung cancer detection continues to grow, leading players are positioning themselves to capture significant market share through technological advancements, partnerships, and enhanced service offerings.

Recent Developments:

- Roche recently launched an advanced liquid biopsy test to detect early-stage lung cancer, enhancing precision diagnostics and improving patient outcomes.

- Illumina acquired Grail, a leader in multi-cancer early detection, to strengthen its presence in the lung cancer diagnostic space.

- GE Healthcare’s new imaging technology for lung cancer screening has been approved by the FDA, allowing for more accurate and faster diagnosis.

- Abbott Laboratories has partnered with a leading cancer research institute to enhance genomic testing capabilities for lung cancer diagnostics.

- Medtronic launched a new minimally invasive biopsy technology for lung cancer, aimed at improving diagnostic accuracy while reducing patient recovery times.

List of Leading Companies:

- Roche Diagnostics

- Abbott Laboratories

- Thermo Fisher Scientific Inc.

- Illumina, Inc.

- GE Healthcare

- Siemens Healthineers

- Philips Healthcare

- Medtronic

- Hologic

- Bio-Rad Laboratories

- Labcorp

- PerkinElmer

- F. Hoffmann-La Roche Ltd.

- AstraZeneca

- Mayo Clinic

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 1.8 Billion |

|

Forecasted Value (2030) |

USD 2.6 Billion |

|

CAGR (2025 – 2030) |

6.4% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Lung Cancer Diagnostic and Screening Market By Test Type (Imaging Tests, Blood Tests, Biopsy), By Method (Radiological Imaging, Molecular Diagnostics, Genetic Testing), By End-User (Hospitals, Diagnostic Laboratories, Cancer Research Institutes) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Roche Diagnostics, Abbott Laboratories, Thermo Fisher Scientific Inc., Illumina, Inc., GE Healthcare, Siemens Healthineers, Philips Healthcare, Medtronic, Hologic, Bio-Rad Laboratories, Labcorp, PerkinElmer, F. Hoffmann-La Roche Ltd., AstraZeneca, Mayo Clinic |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Lung Cancer Diagnostic and Screening Market, by Test Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Imaging Tests |

|

4.2. Blood Tests |

|

4.3. Biopsy |

|

4.4. Other Tests |

|

5. Lung Cancer Diagnostic and Screening Market, by Method (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Radiological Imaging |

|

5.2. Molecular Diagnostics |

|

5.3. Genetic Testing |

|

5.4. Others |

|

6. Lung Cancer Diagnostic and Screening Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Hospitals |

|

6.2. Diagnostic Laboratories |

|

6.3. Cancer Research Institutes |

|

6.4. Others |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Lung Cancer Diagnostic and Screening Market, by Test Type |

|

7.2.7. North America Lung Cancer Diagnostic and Screening Market, by Method |

|

7.2.8. North America Lung Cancer Diagnostic and Screening Market, by End-User |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Lung Cancer Diagnostic and Screening Market, by Test Type |

|

7.2.9.1.2. US Lung Cancer Diagnostic and Screening Market, by Method |

|

7.2.9.1.3. US Lung Cancer Diagnostic and Screening Market, by End-User |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Roche Diagnostics |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Abbott Laboratories |

|

9.3. Thermo Fisher Scientific Inc. |

|

9.4. Illumina, Inc. |

|

9.5. GE Healthcare |

|

9.6. Siemens Healthineers |

|

9.7. Philips Healthcare |

|

9.8. Medtronic |

|

9.9. Hologic |

|

9.10. Bio-Rad Laboratories |

|

9.11. Labcorp |

|

9.12. PerkinElmer |

|

9.13. F. Hoffmann-La Roche Ltd. |

|

9.14. AstraZeneca |

|

9.15. Mayo Clinic |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Lung Cancer Diagnostic and Screening Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Lung Cancer Diagnostic and Screening Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Lung Cancer Diagnostic and Screening Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA