As per Intent Market Research, the Lumbar Disc Replacement Device Market was valued at USD 1.3 Billion in 2024-e and will surpass USD 2.8 Billion by 2030; growing at a CAGR of 13.9% during 2025-2030.

The lumbar disc replacement device market is experiencing substantial growth, driven by the rising prevalence of lumbar spine degenerative diseases, advancements in surgical technologies, and increasing patient demand for less invasive procedures. The market is primarily segmented by product type, material, end-user, procedure type, and application. Among these, artificial lumbar discs are the largest product segment, while metal-on-polymer materials are the fastest growing due to their cost-effectiveness and durability. Minimally invasive surgery (MIS) is the leading procedure type, offering faster recovery times and fewer complications than traditional open surgery.

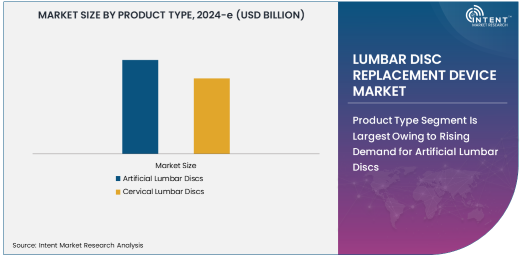

Product Type Segment Is Largest Owing to Rising Demand for Artificial Lumbar Discs

The lumbar disc replacement device market is experiencing significant growth, driven by the increasing prevalence of lumbar spine degenerative diseases and advancements in surgical techniques. Among the various product types available, artificial lumbar discs are the largest segment due to their widespread adoption in spinal surgery. These discs serve as a viable alternative to traditional spinal fusion surgeries, offering improved mobility and quality of life for patients, which has contributed to their growing popularity. The integration of innovative materials and designs in artificial lumbar discs has further fueled their demand, making them the preferred choice for many patients and healthcare providers.

The global preference for artificial lumbar discs is particularly strong in regions with advanced healthcare infrastructure, such as North America and Europe. These regions are witnessing a rise in the number of procedures performed using artificial discs, driven by a higher rate of spine-related disorders, including degenerative disc disease. The efficiency of artificial lumbar discs in restoring natural spine function, combined with the growing trend for less invasive procedures, positions them as the dominant product type within the market.

Metal-on-Polymer Material Segment Is Fastest Growing Owing to Cost-Effective and Durable Solutions

Material innovation is a key factor driving the evolution of the lumbar disc replacement device market. Among the various materials used in lumbar disc replacements, the metal-on-polymer segment is the fastest growing. This material combination is gaining popularity due to its cost-effectiveness and durability, making it an attractive option for both patients and healthcare providers. The metal-on-polymer structure offers enhanced wear resistance, reducing the risk of long-term complications, which is essential for patients requiring long-term relief from spinal issues.

As the demand for affordable and reliable treatments increases, especially in emerging markets with cost-sensitive healthcare systems, metal-on-polymer materials are increasingly being favored. The advantages of this material type, including strength, flexibility, and lower manufacturing costs, are contributing to its rapid adoption across the globe, particularly in regions like Asia-Pacific and Latin America, where healthcare accessibility and budget constraints influence treatment choices.

Ambulatory Surgical Centers (ASCs) Segment Is Fastest Growing Due to Rising Preference for Outpatient Procedures

End-users of lumbar disc replacement devices include hospitals, ambulatory surgical centers (ASCs), and orthopedic clinics. Among these, ASCs are the fastest-growing subsegment, primarily driven by the increasing preference for outpatient procedures. ASCs offer a more cost-effective alternative to hospital-based surgeries, with shorter recovery times and reduced risks of hospital-acquired infections. The shift towards minimally invasive spine surgeries in outpatient settings is also boosting the demand for lumbar disc replacements, particularly for patients seeking faster recovery and lower costs.

The rise in ASC adoption is also supported by advancements in surgical technologies, including robotic-assisted procedures and improved imaging systems, that enable more precise and efficient surgeries outside of traditional hospital settings. With the growing trend of healthcare decentralization and the focus on reducing the burden on hospitals, ASCs are increasingly becoming the go-to option for lumbar disc replacement surgeries, particularly in developed regions like North America and Europe, where healthcare systems are optimizing their operations for efficiency.

Minimally Invasive Surgery (MIS) Segment Is Largest Owing to Technological Advancements and Patient Demand

The procedure type segment in the lumbar disc replacement device market is dominated by minimally invasive surgery (MIS), which is rapidly gaining traction over traditional open surgery. MIS offers several advantages, including smaller incisions, reduced blood loss, less postoperative pain, and faster recovery times, making it the preferred choice for both patients and surgeons. The continued advancements in surgical technologies, such as robotic assistance and improved imaging systems, have further facilitated the growth of MIS, providing a less traumatic alternative to conventional open surgery.

The rising demand for MIS is being driven by patients’ desire for quicker recovery and reduced hospital stays, which is particularly important for those seeking to return to daily activities as soon as possible. As a result, healthcare providers are increasingly adopting MIS for lumbar disc replacement procedures, and this trend is expected to continue as the technology evolves. The largest share of the market for MIS is in developed regions such as North America and Europe, where healthcare systems are better equipped to support these advanced surgical techniques.

Spinal Degeneration Application Segment Is Largest Owing to High Incidence of Lumbar Degenerative Diseases

The application segment of the lumbar disc replacement device market is primarily driven by spinal degeneration, which is the largest subsegment. Spinal degeneration, particularly lumbar degenerative disc disease, is a common cause of severe back pain, especially among the aging population. As the global population ages, the incidence of spinal degeneration is increasing, leading to higher demand for lumbar disc replacement surgeries. This application is typically the first choice for patients experiencing chronic back pain due to degenerative disc conditions that do not respond to conservative treatments.

The growing prevalence of lumbar degenerative diseases and the effectiveness of lumbar disc replacement in restoring mobility and reducing pain are key factors driving the dominance of this application segment. In addition, lumbar disc replacement devices offer long-term solutions by preventing the need for spinal fusion, which can result in loss of motion. As a result, spinal degeneration continues to be the largest application for lumbar disc replacement devices, particularly in North America and Europe, where the aging population is contributing to a surge in demand.

North America Region Is Largest Owing to Advanced Healthcare Systems and High Adoption Rates

North America is the largest region in the lumbar disc replacement device market, driven by its advanced healthcare infrastructure, high disposable income, and increasing prevalence of spinal disorders. The region is home to some of the world’s leading medical device manufacturers and healthcare providers, which facilitates the rapid adoption of cutting-edge technologies, including lumbar disc replacement devices. The growing aging population in the U.S. and Canada is also contributing to the rising demand for these devices, as older individuals are more susceptible to lumbar degenerative diseases.

Moreover, the presence of well-established reimbursement policies for spinal surgeries, coupled with high healthcare expenditure, makes North America an attractive market for lumbar disc replacement devices. The U.S. remains the largest market within North America, with a significant number of procedures being performed each year. This dominance is expected to continue, with further expansion expected through the development of new and improved devices, alongside innovations in minimally invasive surgery techniques.

Competitive Landscape: Leading Companies and Market Dynamics

The competitive landscape of the lumbar disc replacement device market is characterized by the presence of several key players who are innovating in product development, expanding their geographical footprints, and forming strategic partnerships. Leading companies such as Zimmer Biomet, Medtronic, Stryker, and NuVasive are at the forefront of market advancements, with a strong focus on the development of artificial lumbar discs and minimally invasive surgical solutions. These companies are leveraging their technological expertise and extensive distribution networks to gain a competitive edge.

The market is also witnessing an increase in mergers and acquisitions, as companies look to expand their product portfolios and tap into emerging markets with growing healthcare needs. Additionally, strategic collaborations and partnerships with hospitals and ambulatory surgical centers are helping companies to strengthen their market presence. As the demand for lumbar disc replacement devices continues to grow, competition will intensify, especially with the entry of new players offering innovative solutions aimed at improving patient outcomes and reducing overall surgical costs.

Recent Developments:

- Medtronic announced the launch of the Mazor X Stealth Edition for spinal surgeries, including lumbar disc replacement, integrating robotic guidance with advanced imaging technology.

- Stryker acquired K2M to expand its spine portfolio, including lumbar disc replacement devices, and enhance its minimally invasive surgery capabilities.

- Zimmer Biomet received FDA approval for its Mobi-C Cervical Disc, paving the way for broader adoption of cervical and lumbar disc replacement devices in the U.S.

- Globus Medical launched its Matador Artificial Disc to offer a more durable and effective lumbar disc replacement solution for patients suffering from degenerative disc disease.

- NuVasive entered a partnership with Aesculap for expanding its product reach in Europe, focusing on artificial lumbar disc technologies and minimally invasive spinal surgery solutions.

List of Leading Companies:

- Zimmer Biomet

- Medtronic

- Stryker Corporation

- Johnson & Johnson

- NuVasive

- Globus Medical

- Spinal Elements

- Orthofix International

- K2M (A subsidiary of Stryker)

- Aesculap Implant Systems (B. Braun)

- LDR Holding Corporation

- RTI Surgical

- Flexion Therapeutics

- Bone Biologics

- Cerapedics

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 1.3 Billion |

|

Forecasted Value (2030) |

USD 2.8 Billion |

|

CAGR (2025 – 2030) |

13.9% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Lumbar Disc Replacement Device Market By Product Type (Artificial Lumbar Discs, Cervical Lumbar Discs), By Material (Metal-on-Metal, Metal-on-Polymer, Ceramic-on-Metal), By End-User (Hospitals, Ambulatory Surgical Centers, Orthopedic Clinics), By Procedure Type (Minimally Invasive Surgery, Open Surgery), By Application (Spinal Degeneration, Spinal Disc Herniation, Spinal Injuries) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Zimmer Biomet, Medtronic, Stryker Corporation, Johnson & Johnson, NuVasive, Globus Medical, Spinal Elements, Orthofix International, K2M (A subsidiary of Stryker), Aesculap Implant Systems (B. Braun), LDR Holding Corporation, RTI Surgical, Flexion Therapeutics, Bone Biologics, Cerapedics |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Lumbar Disc Replacement Device Market, by Product Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Artificial Lumbar Discs |

|

4.2. Cervical Lumbar Discs |

|

5. Lumbar Disc Replacement Device Market, by Material (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Metal-on-Metal |

|

5.2. Metal-on-Polymer |

|

5.3. Ceramic-on-Metal |

|

6. Lumbar Disc Replacement Device Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Hospitals |

|

6.2. Ambulatory Surgical Centers (ASCs) |

|

6.3. Orthopedic Clinics |

|

7. Lumbar Disc Replacement Device Market, by Procedure Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Minimally Invasive Surgery (MIS) |

|

7.2. Open Surgery |

|

8. Lumbar Disc Replacement Device Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Spinal Degeneration |

|

8.2. Spinal Disc Herniation |

|

8.3. Spinal Injuries |

|

9. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

9.1. Regional Overview |

|

9.2. North America |

|

9.2.1. Regional Trends & Growth Drivers |

|

9.2.2. Barriers & Challenges |

|

9.2.3. Opportunities |

|

9.2.4. Factor Impact Analysis |

|

9.2.5. Technology Trends |

|

9.2.6. North America Lumbar Disc Replacement Device Market, by Product Type |

|

9.2.7. North America Lumbar Disc Replacement Device Market, by Material |

|

9.2.8. North America Lumbar Disc Replacement Device Market, by End-User |

|

9.2.9. North America Lumbar Disc Replacement Device Market, by Procedure Type |

|

9.2.10. North America Lumbar Disc Replacement Device Market, by Application |

|

9.2.11. By Country |

|

9.2.11.1. US |

|

9.2.11.1.1. US Lumbar Disc Replacement Device Market, by Product Type |

|

9.2.11.1.2. US Lumbar Disc Replacement Device Market, by Material |

|

9.2.11.1.3. US Lumbar Disc Replacement Device Market, by End-User |

|

9.2.11.1.4. US Lumbar Disc Replacement Device Market, by Procedure Type |

|

9.2.11.1.5. US Lumbar Disc Replacement Device Market, by Application |

|

9.2.11.2. Canada |

|

9.2.11.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

9.3. Europe |

|

9.4. Asia-Pacific |

|

9.5. Latin America |

|

9.6. Middle East & Africa |

|

10. Competitive Landscape |

|

10.1. Overview of the Key Players |

|

10.2. Competitive Ecosystem |

|

10.2.1. Level of Fragmentation |

|

10.2.2. Market Consolidation |

|

10.2.3. Product Innovation |

|

10.3. Company Share Analysis |

|

10.4. Company Benchmarking Matrix |

|

10.4.1. Strategic Overview |

|

10.4.2. Product Innovations |

|

10.5. Start-up Ecosystem |

|

10.6. Strategic Competitive Insights/ Customer Imperatives |

|

10.7. ESG Matrix/ Sustainability Matrix |

|

10.8. Manufacturing Network |

|

10.8.1. Locations |

|

10.8.2. Supply Chain and Logistics |

|

10.8.3. Product Flexibility/Customization |

|

10.8.4. Digital Transformation and Connectivity |

|

10.8.5. Environmental and Regulatory Compliance |

|

10.9. Technology Readiness Level Matrix |

|

10.10. Technology Maturity Curve |

|

10.11. Buying Criteria |

|

11. Company Profiles |

|

11.1. Zimmer Biomet |

|

11.1.1. Company Overview |

|

11.1.2. Company Financials |

|

11.1.3. Product/Service Portfolio |

|

11.1.4. Recent Developments |

|

11.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

11.2. Medtronic |

|

11.3. Stryker Corporation |

|

11.4. Johnson & Johnson |

|

11.5. NuVasive |

|

11.6. Globus Medical |

|

11.7. Spinal Elements |

|

11.8. Orthofix International |

|

11.9. K2M (A subsidiary of Stryker) |

|

11.10. Aesculap Implant Systems (B. Braun) |

|

11.11. LDR Holding Corporation |

|

11.12. RTI Surgical |

|

11.13. Flexion Therapeutics |

|

11.14. Bone Biologics |

|

11.15. Cerapedics |

|

12. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Lumbar Disc Replacement Device Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Lumbar Disc Replacement Device Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Lumbar Disc Replacement Device Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA