As per Intent Market Research, the Location Intelligence Market was valued at USD 18.7 Billion in 2024-e and will surpass USD 42.7 Billion by 2030; growing at a CAGR of 14.8% during 2025-2030.

The location intelligence market has gained significant traction as businesses and governments increasingly recognize the value of spatial data to drive informed decision-making and improve operational efficiencies. Location intelligence leverages geospatial data, advanced analytics, and machine learning to provide actionable insights, enhancing processes such as market analysis, logistics optimization, and urban planning. With the growing importance of data-driven decision-making across various sectors, the adoption of location intelligence technologies continues to expand. The market is fueled by a surge in demand for more sophisticated data analytics, and it is becoming an essential tool for industries seeking to leverage geographic information for competitive advantage.

Among the technology segments, GIS (Geographic Information Systems) is the largest contributor to the location intelligence market. GIS technology enables organizations to capture, store, analyze, and visualize spatial data, providing a comprehensive view of geographic locations and patterns. This technology has wide applications across industries such as government, retail, and real estate, where precise mapping and analysis of geographic data are crucial. By integrating GIS with other data sources, businesses can derive insights that improve planning, forecasting, and customer targeting. The continued evolution of GIS technology, along with its integration with other cutting-edge technologies like AI and machine learning, is expected to drive further growth in this segment.

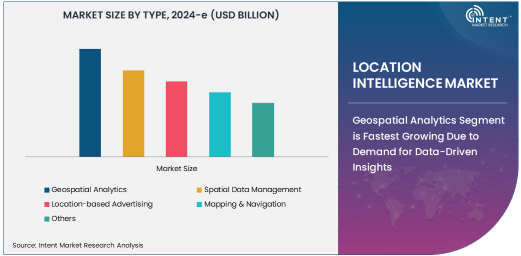

Geospatial Analytics Segment is Fastest Growing Due to Demand for Data-Driven Insights

In the type segment, geospatial analytics is the fastest-growing category, primarily driven by the increasing need for businesses and governments to extract meaningful insights from spatial data. Geospatial analytics involves the use of spatial data combined with statistical and analytical methods to uncover patterns and trends that are not immediately apparent. This technology is gaining momentum in sectors such as retail, transportation, and real estate, where location-based insights can guide critical business decisions, such as market expansion, site selection, and supply chain optimization. The ability to process and analyze large sets of spatial data in real-time is making geospatial analytics an indispensable tool in modern business strategy.

The rapid growth of geospatial analytics is further supported by the proliferation of data from IoT devices, smartphones, and satellites, which generates vast amounts of location-based data. By utilizing geospatial analytics, companies can identify emerging trends, optimize operational workflows, and improve customer targeting. In particular, the retail sector is leveraging geospatial analytics to better understand consumer behavior, predict foot traffic, and refine marketing strategies. As data volume and complexity continue to rise, the adoption of geospatial analytics will only accelerate, positioning it as the fastest-growing segment in the location intelligence market.

Retail End-User Segment is Largest Due to Personalization and Optimization

Among the end-user segments, retail stands out as the largest contributor to the location intelligence market, driven by the sector's increasing reliance on location-based insights for personalized customer engagement and operational efficiency. Retailers are leveraging location intelligence to gain a deeper understanding of customer behavior, optimize store locations, and enhance supply chain management. By analyzing spatial data, retailers can make data-driven decisions about product placement, inventory distribution, and marketing strategies. Additionally, location intelligence helps in creating personalized offers and recommendations based on customers' real-time location, leading to increased customer satisfaction and higher conversion rates.

The retail sector's focus on omnichannel strategies, where physical and online experiences are seamlessly integrated, has further fueled the demand for location intelligence. With the rise of e-commerce, retailers are turning to location-based analytics to enhance in-store experiences and refine their online marketing strategies. As competition intensifies in the retail space, the ability to leverage location data for targeted marketing and operational optimization is proving to be a key differentiator, solidifying retail as the largest end-user segment in the location intelligence market.

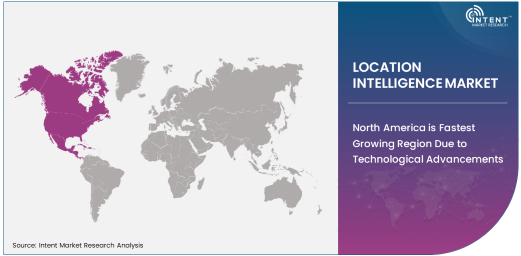

North America is Fastest Growing Region Due to Technological Advancements

Geographically, North America is the fastest-growing region in the location intelligence market, largely due to the rapid adoption of advanced technologies and strong infrastructure for data analytics. The region is home to some of the world's leading tech companies, which are driving innovations in GIS, big data analytics, and AI, enabling businesses to derive greater value from location-based data. North America's focus on digital transformation and smart city initiatives is further accelerating the demand for location intelligence solutions, particularly in sectors like retail, transportation, and government. The integration of location intelligence with emerging technologies such as machine learning and IoT is creating new opportunities for businesses to enhance operational efficiency and customer engagement.

The U.S. and Canada are leading the charge in the adoption of location intelligence technologies, with businesses in both private and public sectors investing heavily in data-driven solutions. In retail, for instance, companies are leveraging location intelligence to refine their marketing strategies and optimize store placements. The strong presence of tech giants and the rapid pace of digitalization in North America ensure that the region will continue to lead the growth of the location intelligence market in the coming years.

Leading Companies and Competitive Landscape

The location intelligence market is highly competitive, with several prominent players focusing on innovation and the development of integrated solutions to cater to the growing demand for spatial data analytics. Leading companies such as Esri, Microsoft, IBM, and Oracle are at the forefront, offering comprehensive GIS solutions, cloud-based platforms, and advanced analytics tools that enable businesses to harness the power of geospatial data. These companies are constantly evolving their offerings, incorporating AI, machine learning, and big data analytics to provide more sophisticated and actionable insights.

The competitive landscape is also characterized by strategic partnerships and acquisitions, as companies seek to expand their capabilities and reach new markets. In particular, collaborations between GIS providers and industries like transportation, retail, and government are becoming increasingly common, as organizations recognize the potential of location intelligence to drive efficiency and improve decision-making. The market is expected to see continued investment in R&D, with companies striving to develop more accurate, real-time geospatial analytics solutions. As the demand for location intelligence grows across various sectors, competition will intensify, with a focus on delivering increasingly powerful and user-friendly technologies.

Recent Developments:

- ESRI launched a new GIS platform designed to enhance location-based analytics and improve decision-making for businesses.

- Google Inc. introduced new AI-powered location intelligence features in its cloud platform to support better real-time decision-making.

- IBM Corporation expanded its location intelligence services by integrating advanced machine learning algorithms for geospatial analytics.

- HERE Technologies partnered with logistics companies to deploy location intelligence solutions for optimizing delivery routes and fleet management.

- Microsoft Corporation rolled out new cloud-based location intelligence solutions for government agencies to improve urban planning and management.

List of Leading Companies:

- ESRI (Environmental Systems Research Institute)

- IBM Corporation

- Google Inc.

- Microsoft Corporation

- HERE Technologies

- Oracle Corporation

- Trimble Inc.

- TomTom N.V.

- Pitney Bowes

- SAP SE

- Geotab Inc.

- Foursquare Labs, Inc.

- Telenav, Inc.

- Mapbox, Inc.

- Lightbox

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 18.7 Billion |

|

Forecasted Value (2030) |

USD 42.7 Billion |

|

CAGR (2025 – 2030) |

14.8% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Location Intelligence Market By Type (Geospatial Analytics, Spatial Data Management, Location-based Advertising, Mapping & Navigation), By Technology (GIS (Geographic Information Systems), Big Data & Analytics, Cloud Computing, AI & Machine Learning), and By End-User (Retail, Transportation & Logistics, Government, Real Estate, Healthcare); Global Insights & Forecast (2024 - 2030) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

ESRI (Environmental Systems Research Institute), IBM Corporation, Google Inc., Microsoft Corporation, HERE Technologies, Oracle Corporation, Trimble Inc., TomTom N.V., Pitney Bowes, SAP SE, Geotab Inc., Foursquare Labs, Inc., Telenav, Inc., Mapbox, Inc., Lightbox |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Location Intelligence Market, by Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Geospatial Analytics |

|

4.2. Spatial Data Management |

|

4.3. Location-based Advertising |

|

4.4. Mapping & Navigation |

|

4.5. Others |

|

5. Location Intelligence Market, by Technology (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. GIS (Geographic Information Systems) |

|

5.2. Big Data & Analytics |

|

5.3. Cloud Computing |

|

5.4. AI & Machine Learning |

|

5.5. Others |

|

6. Location Intelligence Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Retail |

|

6.2. Transportation & Logistics |

|

6.3. Government |

|

6.4. Real Estate |

|

6.5. Healthcare |

|

6.6. Others |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Location Intelligence Market, by Type |

|

7.2.7. North America Location Intelligence Market, by Technology |

|

7.2.8. North America Location Intelligence Market, by End-User |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Location Intelligence Market, by Type |

|

7.2.9.1.2. US Location Intelligence Market, by Technology |

|

7.2.9.1.3. US Location Intelligence Market, by End-User |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. ESRI (Environmental Systems Research Institute) |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. IBM Corporation |

|

9.3. Google Inc. |

|

9.4. Microsoft Corporation |

|

9.5. HERE Technologies |

|

9.6. Oracle Corporation |

|

9.7. Trimble Inc. |

|

9.8. TomTom N.V. |

|

9.9. Pitney Bowes |

|

9.10. SAP SE |

|

9.11. Geotab Inc. |

|

9.12. Foursquare Labs, Inc. |

|

9.13. Telenav, Inc. |

|

9.14. Mapbox, Inc. |

|

9.15. Lightbox |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Location Intelligence Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Location Intelligence Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Location Intelligence Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA