As per Intent Market Research, the Location Based Services Market was valued at USD 69.7 Billion in 2024-e and will surpass USD 166.2 Billion by 2030; growing at a CAGR of 15.6% during 2025-2030.

The location-based services (LBS) market has emerged as a vital component in numerous industries, leveraging geographic data to enhance consumer experiences, improve operational efficiencies, and enable precise service delivery. The market spans several types of services, including asset tracking, geofencing, and location-based advertising, driven by the increasing reliance on mobile devices and connected technology. The advent of GPS technology has greatly contributed to the expansion of this market, as it facilitates real-time tracking, navigation, and service personalization for users across various sectors, ranging from retail to healthcare. As consumers demand more tailored and immediate solutions, LBS technologies continue to evolve, pushing the boundaries of what location data can achieve.

Among the technology segments, GPS is the largest contributor to the growth of the location-based services market. GPS technology enables accurate location tracking, which is critical for services such as navigation, asset tracking, and geofencing. With the widespread adoption of smartphones and connected devices, GPS has become the cornerstone of modern location-based services, supporting industries like transportation, retail, and logistics in optimizing operations. From providing real-time navigation updates to tracking assets in transit, GPS plays a pivotal role in meeting the growing demand for personalized, location-driven services.

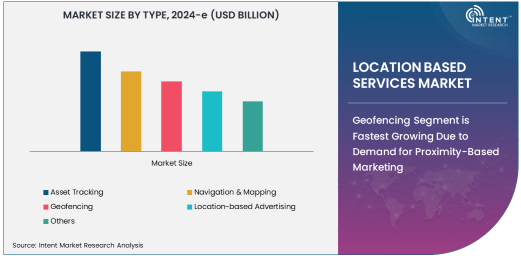

Geofencing Segment is Fastest Growing Due to Demand for Proximity-Based Marketing

In the type segment, geofencing is the fastest-growing subsegment, primarily driven by the increasing demand for proximity-based marketing and location-specific services. Geofencing technology enables businesses to set virtual boundaries around a specific location, triggering alerts or notifications when a customer enters or exits the designated area. This capability has found widespread application in retail, hospitality, and advertising, allowing companies to target customers with personalized promotions and offers based on their real-time location. As consumers increasingly expect tailored and timely interactions with brands, the geofencing segment is witnessing rapid growth, particularly in mobile marketing strategies.

Geofencing is also gaining traction in industries such as transportation and logistics, where it enables fleet management and delivery optimization by notifying operators when vehicles enter or leave predefined areas. The ability to automate processes and deliver context-aware services has positioned geofencing as a key enabler of efficiency and customer engagement. As technology advances and the integration of geofencing with other location-based tools improves, its adoption is expected to accelerate, solidifying its position as the fastest-growing segment in the LBS market.

Retail End-User Segment is Largest Due to Enhanced Customer Engagement

Among the end-user segments, retail is the largest contributor to the location-based services market, owing to its reliance on personalized customer engagement and operational efficiency. Retailers are increasingly adopting location-based technologies to enhance the shopping experience, improve in-store navigation, and provide personalized offers to customers based on their real-time location. Through LBS, retailers can send notifications, coupons, and recommendations directly to consumers' mobile devices, driving foot traffic and increasing conversion rates. Additionally, LBS helps retailers optimize store layouts and inventory management by tracking customer movement and preferences.

The retail sector’s adoption of location-based services has been further accelerated by the rise of omnichannel shopping, where customers expect seamless interactions both online and offline. As the retail industry continues to focus on improving customer engagement and creating smarter shopping experiences, location-based technologies such as geofencing and proximity-based marketing will continue to play a crucial role. The combination of personalized marketing and operational enhancements has cemented retail as the largest end-user segment in the LBS market.

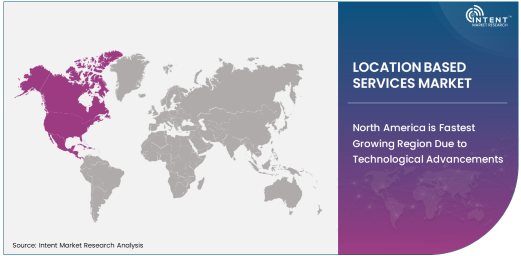

North America is Fastest Growing Region Due to Technological Advancements

Geographically, North America is the fastest-growing region in the location-based services market. The region's rapid adoption of advanced technologies, coupled with a strong infrastructure for mobile and internet connectivity, positions it at the forefront of LBS innovations. North America is home to major technology companies that are driving the development of GPS, Bluetooth, and NFC solutions, making it a hub for LBS applications across various industries. The region's focus on smart cities, e-commerce, and digital transformation in sectors like retail and healthcare has further propelled the demand for location-based services.

The growing trend of personalization and data-driven marketing in North America, combined with the region's robust mobile penetration, ensures a high uptake of LBS solutions. In particular, the retail and transportation sectors are major drivers of market growth, as businesses strive to deliver more tailored services and streamline operations. As companies in North America continue to innovate with location-aware technologies, the region is set to maintain its position as the fastest-growing market for LBS globally.

Leading Companies and Competitive Landscape

The location-based services market is highly competitive, with several leading players focused on providing cutting-edge solutions to cater to the diverse needs of industries. Companies like Google, Apple, and Microsoft are key players, offering LBS technologies such as GPS navigation, mapping, and geofencing capabilities through their platforms and services. Additionally, specialized firms like Zebra Technologies and Qualcomm are leading innovation in asset tracking and Bluetooth-based location solutions.

The competitive landscape is characterized by constant technological advancements and partnerships aimed at expanding market reach. Companies are increasingly integrating artificial intelligence, machine learning, and data analytics into LBS platforms to provide more sophisticated and personalized services. The growing demand for smart cities, autonomous vehicles, and smart retail experiences is fueling investment in R&D, ensuring that the market remains dynamic. As new entrants and established firms continue to evolve their offerings, competition in the LBS market is expected to intensify, with an emphasis on enhancing user experiences and delivering precise, actionable insights.

Recent Developments:

- Google Inc. launched a new suite of location-based services for businesses, integrating advanced AI and GPS tracking capabilities.

- Apple Inc. expanded its location-based advertising tools for retailers, offering more precise targeting and customer insights.

- Microsoft Corporation introduced a new geofencing feature in its cloud platform, enabling businesses to trigger automated actions based on user location.

- IBM Corporation partnered with transportation companies to provide real-time location tracking for fleet management and logistics operations.

- Qualcomm Technologies, Inc. unveiled a new Bluetooth-based location tracking solution designed for indoor positioning systems.

List of Leading Companies:

- Google Inc.

- Apple Inc.

- Microsoft Corporation

- IBM Corporation

- Qualcomm Technologies, Inc.

- HERE Technologies

- Ericsson AB

- TomTom N.V.

- SAP SE

- Geoforce, Inc.

- Cisco Systems, Inc.

- Inrix, Inc.

- Telenav, Inc.

- Uber Technologies, Inc.

- Accenture Plc

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 69.7 Billion |

|

Forecasted Value (2030) |

USD 166.2 Billion |

|

CAGR (2025 – 2030) |

15.6% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Location Based Services Market By Type (Asset Tracking, Navigation & Mapping, Geofencing, Location-based Advertising), By Technology (GPS, Wi-Fi, Bluetooth, NFC (Near Field Communication)), and By End-User (Retail, Transportation & Logistics, Healthcare, BFSI (Banking, Financial Services, and Insurance), Government) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Google Inc., Apple Inc., Microsoft Corporation, IBM Corporation, Qualcomm Technologies, Inc., HERE Technologies, Ericsson AB, TomTom N.V., SAP SE, Geoforce, Inc., Cisco Systems, Inc., Inrix, Inc., Telenav, Inc., Uber Technologies, Inc., Accenture Plc |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Location Based Services Market, by Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Asset Tracking |

|

4.2. Navigation & Mapping |

|

4.3. Geofencing |

|

4.4. Location-based Advertising |

|

4.5. Others |

|

5. Location Based Services Market, by Technology (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. GPS |

|

5.2. Wi-Fi |

|

5.3. Bluetooth |

|

5.4. NFC (Near Field Communication) |

|

5.5. Others |

|

6. Location Based Services Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Retail |

|

6.2. Transportation & Logistics |

|

6.3. Healthcare |

|

6.4. BFSI (Banking, Financial Services, and Insurance) |

|

6.5. Government |

|

6.6. Others |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Location Based Services Market, by Type |

|

7.2.7. North America Location Based Services Market, by Technology |

|

7.2.8. North America Location Based Services Market, by End-User |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Location Based Services Market, by Type |

|

7.2.9.1.2. US Location Based Services Market, by Technology |

|

7.2.9.1.3. US Location Based Services Market, by End-User |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Google Inc. |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Apple Inc. |

|

9.3. Microsoft Corporation |

|

9.4. IBM Corporation |

|

9.5. Qualcomm Technologies, Inc. |

|

9.6. HERE Technologies |

|

9.7. Ericsson AB |

|

9.8. TomTom N.V. |

|

9.9. SAP SE |

|

9.10. Geoforce, Inc. |

|

9.11. Cisco Systems, Inc. |

|

9.12. Inrix, Inc. |

|

9.13. Telenav, Inc. |

|

9.14. Uber Technologies, Inc. |

|

9.15. Accenture Plc |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Location Based Services Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Location Based Services Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Location Based Services Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA