As per Intent Market Research, the Lithium Titanate Batteries Market was valued at USD 2.6 Billion in 2024-e and will surpass USD 6.2 Billion by 2030; growing at a CAGR of 15.2% during 2025-2030.

The lithium titanate batteries market is emerging as a key player in energy storage and power solutions, offering distinct advantages in terms of safety, lifespan, and charge/discharge performance. Known for their exceptional thermal stability and fast charging capabilities, lithium titanate batteries (LTO) are gaining traction in industries that demand high power density, longevity, and reliability. Unlike conventional lithium-ion batteries, LTO batteries utilize lithium titanate as the anode material, which enhances their overall performance by offering faster charging times and a longer cycle life.

This unique combination of characteristics positions lithium titanate batteries as an ideal solution for electric vehicles (EVs), energy storage systems (ESS), and critical applications in aerospace and medical devices. The market's growth is closely tied to the global shift towards clean energy solutions and the rising demand for electric mobility and energy storage technologies. As industries seek longer-lasting, more efficient batteries, LTO batteries present a compelling alternative to traditional lithium-ion technologies.

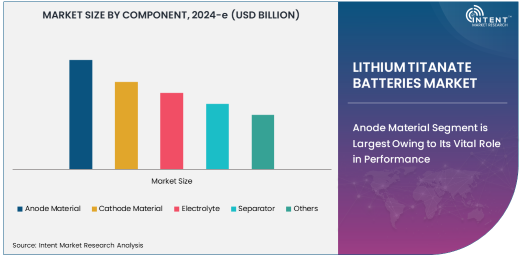

Anode Material Segment is Largest Owing to Its Vital Role in Performance

The anode material segment holds the largest share in the lithium titanate batteries market, primarily due to the unique properties of lithium titanate (Li4Ti5O12), which serves as the anode in these batteries. Lithium titanate offers superior charge and discharge rates, making it an essential component for applications requiring quick power delivery and long life cycles. This anode material is known for its high safety profile and resistance to thermal runaway, which makes lithium titanate batteries particularly suitable for high-stakes environments like electric vehicles and aerospace.

Compared to traditional graphite-based anodes, lithium titanate provides a higher voltage window and a significantly longer cycle life. These advantages are crucial in applications that require frequent charging and discharging, such as energy storage systems (ESS) and consumer electronics. The longevity of LTO batteries, with more than 10,000 charge cycles, makes it a preferred choice for industries seeking sustainable and cost-effective energy storage solutions.

Electric Vehicles (EVs) Segment is Fastest Growing Due to Growing EV Demand

The electric vehicle (EV) application segment is the fastest growing in the lithium titanate batteries market, driven by the increasing adoption of EVs as a part of the global push for clean energy and reduced carbon emissions. Lithium titanate batteries, with their fast charging times, enhanced cycle life, and safety features, are particularly well-suited to the EV market. These batteries enable electric vehicles to charge more quickly compared to traditional lithium-ion batteries, which is a key selling point for consumers looking for convenient and efficient EV solutions.

As governments around the world implement stricter environmental regulations and provide incentives for electric vehicle adoption, the demand for LTO batteries in the EV sector is expected to rise exponentially. Additionally, LTO batteries' ability to handle extreme temperatures and maintain performance over longer periods makes them an attractive choice for electric vehicles operating in diverse climates and conditions.

Energy Storage Systems Segment is Gaining Momentum

The energy storage systems (ESS) segment is seeing significant growth, with lithium titanate batteries being increasingly integrated into renewable energy solutions. ESS plays a critical role in stabilizing energy grids, especially in regions that rely on intermittent renewable energy sources like solar and wind. Lithium titanate's long cycle life and rapid charging capabilities make it ideal for ESS applications, ensuring that energy can be stored efficiently and released quickly when needed.

The shift toward renewable energy is driving the need for robust and durable energy storage technologies, and lithium titanate batteries provide a high-performance solution. They offer significant advantages over conventional lead-acid and even some lithium-ion batteries, particularly in terms of longevity, thermal stability, and safety. As more countries invest in renewable energy infrastructure, the demand for efficient and reliable energy storage systems, powered by lithium titanate batteries, is set to rise.

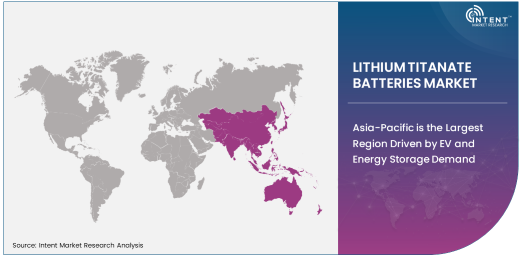

Asia-Pacific is the Largest Region Driven by EV and Energy Storage Demand

Asia-Pacific dominates the lithium titanate batteries market, driven by the booming electric vehicle (EV) market and the growing demand for energy storage systems in the region. Countries such as China, Japan, and South Korea are at the forefront of electric vehicle adoption and battery manufacturing. The region is home to some of the world's largest EV manufacturers, and lithium titanate batteries are increasingly being used in electric vehicles for their fast-charging and long-life benefits.

In addition to the automotive sector, Asia-Pacific is a major player in the renewable energy space, with substantial investments in solar and wind energy projects. This is further propelling the demand for energy storage solutions, where lithium titanate batteries offer long-term, efficient energy storage capabilities. The region's robust manufacturing infrastructure, along with favorable government policies supporting clean energy initiatives, positions Asia-Pacific as the largest and most lucrative market for lithium titanate batteries.

Competitive Landscape and Leading Companies

The lithium titanate batteries market is highly competitive, with key players including Toshiba Corporation, A123 Systems, and Leclanché SA. These companies are focused on advancing battery technology to meet the growing demand for EVs, energy storage systems, and other high-performance applications.

Toshiba, a leader in the market, has been at the forefront of lithium titanate battery development, offering their SCiB (Super Charge ion Battery) technology, which is widely used in both automotive and industrial applications. A123 Systems and Leclanché have also made significant strides in developing high-quality LTO batteries, with a particular emphasis on large-scale energy storage systems. As the market for lithium titanate batteries continues to expand, companies are investing in research and development to enhance battery performance, reduce costs, and improve manufacturing processes.

Strategic partnerships, mergers, and acquisitions are also shaping the competitive landscape, as companies seek to strengthen their positions in the growing energy storage and electric vehicle sectors. Additionally, the push for sustainable battery solutions and advancements in recycling technologies are expected to drive further innovation and competition in the market.

Recent Developments:

- Toshiba Corporation launched an upgraded lithium titanate battery with enhanced charging speed and durability for EV applications.

- Altairnano partnered with a renewable energy company to supply lithium titanate batteries for grid energy storage.

- Yinlong Energy Co., Ltd. expanded its production facility to meet the rising demand for lithium titanate batteries in the automotive sector.

- Microvast Inc. introduced a high-capacity lithium titanate battery for commercial electric vehicles.

- Leclanché SA announced a new collaboration to integrate lithium titanate batteries into smart grid energy systems.

List of Leading Companies:

- Toshiba Corporation

- Altairnano (Altair Nanotechnologies Inc.)

- Microvast Inc.

- Yinlong Energy Co., Ltd.

- Leclanché SA

- GS Yuasa Corporation

- CATL (Contemporary Amperex Technology Co., Ltd.)

- Panasonic Corporation

- BYD Company Limited

- LG Energy Solution

- Samsung SDI Co., Ltd.

- EnerDel, Inc.

- Hitachi Chemical Co., Ltd.

- Saft Groupe S.A. (TotalEnergies Company)

- Johnson Matthey

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 2.6 Billion |

|

Forecasted Value (2030) |

USD 6.2 Billion |

|

CAGR (2025 – 2030) |

15.2% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Lithium Titanate Batteries Market By Component (Anode Material, Cathode Material, Electrolyte, Separator), By Application (Electric Vehicles (EVs), Energy Storage Systems, Consumer Electronics, Aerospace & Defense, Medical Devices), and By End-User (Automotive Industry, Renewable Energy Sector, Electronics Manufacturers, Healthcare Industry, Aerospace Sector) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Toshiba Corporation, Altairnano (Altair Nanotechnologies Inc.), Microvast Inc., Yinlong Energy Co., Ltd., Leclanché SA, GS Yuasa Corporation, CATL (Contemporary Amperex Technology Co., Ltd.), Panasonic Corporation, BYD Company Limited, LG Energy Solution, Samsung SDI Co., Ltd., EnerDel, Inc., Hitachi Chemical Co., Ltd., Saft Groupe S.A. (TotalEnergies Company), Johnson Matthey |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Lithium Titanate Batteries Market, by Component (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Anode Material |

|

4.2. Cathode Material |

|

4.3. Electrolyte |

|

4.4. Separator |

|

4.5. Others |

|

5. Lithium Titanate Batteries Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Electric Vehicles (EVs) |

|

5.2. Energy Storage Systems |

|

5.3. Consumer Electronics |

|

5.4. Aerospace & Defense |

|

5.5. Medical Devices |

|

5.6. Others |

|

6. Lithium Titanate Batteries Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Automotive Industry |

|

6.2. Renewable Energy Sector |

|

6.3. Electronics Manufacturers |

|

6.4. Healthcare Industry |

|

6.5. Aerospace Sector |

|

6.6. Others |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Lithium Titanate Batteries Market, by Component |

|

7.2.7. North America Lithium Titanate Batteries Market, by Application |

|

7.2.8. North America Lithium Titanate Batteries Market, by End-User |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Lithium Titanate Batteries Market, by Component |

|

7.2.9.1.2. US Lithium Titanate Batteries Market, by Application |

|

7.2.9.1.3. US Lithium Titanate Batteries Market, by End-User |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Toshiba Corporation |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Altairnano (Altair Nanotechnologies Inc.) |

|

9.3. Microvast Inc. |

|

9.4. Yinlong Energy Co., Ltd. |

|

9.5. Leclanché SA |

|

9.6. GS Yuasa Corporation |

|

9.7. CATL (Contemporary Amperex Technology Co., Ltd.) |

|

9.8. Panasonic Corporation |

|

9.9. BYD Company Limited |

|

9.10. LG Energy Solution |

|

9.11. Samsung SDI Co., Ltd. |

|

9.12. EnerDel, Inc. |

|

9.13. Hitachi Chemical Co., Ltd. |

|

9.14. Saft Groupe S.A. (TotalEnergies Company) |

|

9.15. Johnson Matthey |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Lithium Titanate Batteries Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Lithium Titanate Batteries Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Lithium Titanate Batteries Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA