As per Intent Market Research, the Liquid Waste Management Market was valued at USD 97.1 Billion in 2024-e and will surpass USD 144.1 Billion by 2030; growing at a CAGR of 6.8% during 2025-2030.

The liquid waste management market plays a crucial role in addressing the environmental and health challenges posed by improper disposal of liquid waste. Rapid industrialization, urbanization, and stringent government regulations are driving the demand for effective solutions in this sector. Liquid waste management encompasses services such as collection, treatment, recycling, and disposal, tailored to different types of liquid waste, including industrial wastewater, hazardous liquids, and municipal wastewater. As sustainability becomes a priority, industries and municipalities are increasingly investing in advanced waste management technologies to minimize their environmental footprint and comply with regulatory standards.

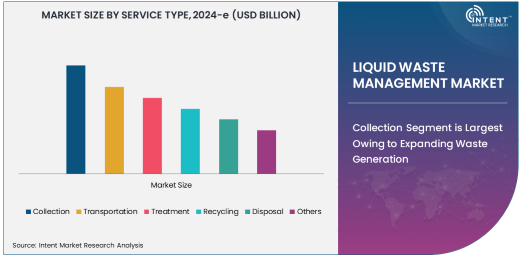

Collection Segment is Largest Owing to Expanding Waste Generation

The collection segment holds the largest share in the liquid waste management market due to the consistent increase in waste generation from industrial, municipal, and residential sources. Efficient collection systems form the backbone of liquid waste management by ensuring that waste is systematically gathered from various locations. Industries such as oil & gas, healthcare, and municipal sectors rely heavily on collection services to manage their liquid waste effectively.

Moreover, advancements in technology, including the integration of IoT-enabled sensors and smart systems, are optimizing the waste collection process. These technologies enable real-time monitoring, reducing inefficiencies and ensuring timely pick-ups. As urban populations grow and industrial activities intensify, the demand for scalable and reliable collection solutions is expected to drive further growth in this segment.

Industrial Wastewater is the Fastest Growing Waste Type Due to Rising Industrial Activities

Industrial wastewater is emerging as the fastest-growing waste type within the market, propelled by the surge in industrial activities across sectors such as manufacturing, chemicals, and oil & gas. The treatment and management of industrial wastewater are critical to ensuring environmental compliance and mitigating the release of harmful pollutants into ecosystems.

Governments worldwide are imposing stricter regulations on wastewater discharge, compelling industries to adopt advanced wastewater treatment and recycling technologies. Additionally, the adoption of zero-liquid discharge systems is gaining momentum, enabling industries to recycle and reuse water efficiently. The growing awareness of water conservation and the increasing emphasis on sustainable industrial practices are expected to drive the demand for industrial wastewater management solutions.

Oil & Gas Sector is the Largest End-Use Industry Due to High Wastewater Output

The oil & gas sector represents the largest end-use industry in the liquid waste management market. This is attributed to the significant volume of wastewater generated during exploration, production, and refining processes. Produced water, which contains hydrocarbons and other contaminants, requires advanced treatment before disposal or reuse.

With the global energy demand showing consistent growth, the oil & gas sector is under pressure to adopt sustainable waste management practices. Companies are investing in cutting-edge treatment technologies to manage hazardous waste efficiently and comply with environmental regulations. Furthermore, the industry's focus on resource recovery, such as extracting valuable by-products from wastewater, is creating opportunities for innovation and growth.

Asia-Pacific is the Fastest Growing Region Owing to Rapid Urbanization

The Asia-Pacific region is poised to register the fastest growth in the liquid waste management market, driven by rapid urbanization, industrial expansion, and population growth. Countries such as China, India, and Southeast Asian nations are witnessing increased waste generation from both industrial and municipal sources.

Government initiatives to improve wastewater infrastructure, coupled with rising investments in sustainable waste management technologies, are fueling market growth in this region. Additionally, the increasing awareness among industries and municipalities about the environmental and health impacts of liquid waste disposal is driving the adoption of advanced waste management solutions.

Competitive Landscape and Leading Companies

The liquid waste management market is characterized by the presence of numerous players offering a wide range of services. Key companies such as Veolia, SUEZ, Clean Harbors, and Waste Management Inc. lead the market with their extensive service portfolios and advanced treatment technologies. These companies are focused on innovation, strategic partnerships, and expanding their geographical footprint to cater to the growing demand.

The competitive landscape is marked by a shift toward digitalization and automation, with companies leveraging technologies like IoT, AI, and data analytics to optimize their operations. As regulatory frameworks become more stringent and industries prioritize sustainability, the liquid waste management market is expected to see continued growth and innovation in the coming years.

Recent Developments:

- Veolia Environnement expanded its wastewater treatment capabilities with the launch of a new sustainable solution for industrial liquid waste.

- SUEZ partnered with a leading municipal authority to modernize its wastewater treatment plants with advanced recycling systems.

- Waste Management, Inc. introduced a new technology to improve hazardous liquid waste handling efficiency.

- Clean Harbors acquired a regional waste management firm to enhance its liquid waste disposal services.

- Republic Services, Inc. announced investments in cutting-edge treatment technologies for municipal wastewater.

List of Leading Companies:

- Veolia Environnement

- SUEZ

- Waste Management, Inc.

- Clean Harbors

- Covanta Holding Corporation

- Republic Services, Inc.

- Stericycle, Inc.

- Remondis SE & Co. KG

- GFL Environmental Inc.

- US Ecology, Inc.

- FCC Environment

- Biffa

- Hulsey Environmental Services

- Heritage-Crystal Clean, Inc.

- Casella Waste Systems, Inc.

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 97.1 Billion |

|

Forecasted Value (2030) |

USD 144.1 Billion |

|

CAGR (2025 – 2030) |

6.8% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Liquid Waste Management Market By Service Type (Collection, Transportation, Treatment, Recycling, Disposal), By Waste Type (Industrial Wastewater, Municipal Wastewater, Hazardous Liquid Waste, Non-Hazardous Liquid Waste), and By End-Use Industry (Oil & Gas, Chemical Industry, Healthcare, Agriculture, Municipal Sector) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Veolia Environnement, SUEZ, Waste Management, Inc., Clean Harbors, Covanta Holding Corporation, Republic Services, Inc., Stericycle, Inc., Remondis SE & Co. KG, GFL Environmental Inc., US Ecology, Inc., FCC Environment, Biffa, Hulsey Environmental Services, Heritage-Crystal Clean, Inc., Casella Waste Systems, Inc. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Liquid Waste Management Market, by Service Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Collection |

|

4.2. Transportation |

|

4.3. Treatment |

|

4.4. Recycling |

|

4.5. Disposal |

|

4.6. Others |

|

5. Liquid Waste Management Market, by Waste Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Industrial Wastewater |

|

5.2. Municipal Wastewater |

|

5.3. Hazardous Liquid Waste |

|

5.4. Non-Hazardous Liquid Waste |

|

5.5. Others |

|

6. Liquid Waste Management Market, by End-Use Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Oil & Gas |

|

6.2. Chemical Industry |

|

6.3. Healthcare |

|

6.4. Agriculture |

|

6.5. Municipal Sector |

|

6.6. Others |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Liquid Waste Management Market, by Service Type |

|

7.2.7. North America Liquid Waste Management Market, by Waste Type |

|

7.2.8. North America Liquid Waste Management Market, by End-Use Industry |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Liquid Waste Management Market, by Service Type |

|

7.2.9.1.2. US Liquid Waste Management Market, by Waste Type |

|

7.2.9.1.3. US Liquid Waste Management Market, by End-Use Industry |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Veolia Environnement |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. SUEZ |

|

9.3. Waste Management, Inc. |

|

9.4. Clean Harbors |

|

9.5. Covanta Holding Corporation |

|

9.6. Republic Services, Inc. |

|

9.7. Stericycle, Inc. |

|

9.8. Remondis SE & Co. KG |

|

9.9. GFL Environmental Inc. |

|

9.10. US Ecology, Inc. |

|

9.11. FCC Environment |

|

9.12. Biffa |

|

9.13. Hulsey Environmental Services |

|

9.14. Heritage-Crystal Clean, Inc. |

|

9.15. Casella Waste Systems, Inc. |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Liquid Waste Management Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Liquid Waste Management Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Liquid Waste Management Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA