As per Intent Market Research, the Joint Reconstruction Market was valued at USD 15.4 billion in 2024-e and will surpass USD 25.6 billion by 2030; growing at a CAGR of 7.6% during 2025 - 2030.

The joint reconstruction market is a critical segment within the broader orthopedic industry, driven by the increasing incidence of musculoskeletal disorders, aging populations, and the growing demand for advanced surgical solutions to treat joint degeneration. Joint reconstruction procedures, particularly total joint replacements, have gained widespread adoption due to their ability to significantly improve quality of life for patients suffering from conditions like osteoarthritis, rheumatoid arthritis, and traumatic joint injuries. Advances in surgical techniques, prosthetic materials, and minimally invasive procedures are further enhancing the effectiveness and appeal of joint reconstruction surgeries.

The market is segmented by product type, material, procedure type, and end-user, with key areas of focus including knee, hip, and shoulder reconstruction devices, as well as innovations in materials like metal, polyethylene, ceramic, and composite for prosthetic components. The rising prevalence of joint-related diseases, particularly among the aging population, has created a substantial demand for joint reconstruction procedures. Furthermore, technological advancements in implant design and surgical techniques are improving patient outcomes, contributing to the growth of the joint reconstruction market.

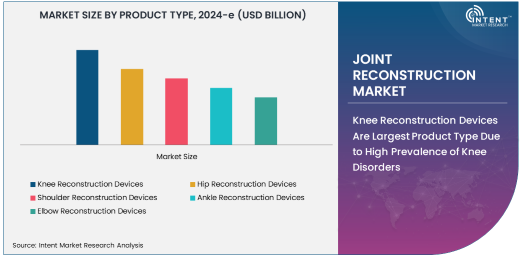

Knee Reconstruction Devices Are Largest Product Type Due to High Prevalence of Knee Disorders

Knee reconstruction devices represent the largest product type in the joint reconstruction market, driven by the high prevalence of knee-related disorders such as osteoarthritis, which significantly impacts mobility and quality of life. Knee osteoarthritis, often exacerbated by aging and lifestyle factors, is one of the most common causes of joint pain and dysfunction, leading to a high demand for knee reconstruction procedures like total knee replacements (TKR). The success of knee reconstruction surgeries, combined with advancements in prosthetic designs and materials, has made knee joint replacement a widely preferred treatment option for patients with severe knee degeneration.

Knee reconstruction procedures have also benefited from innovations in implant materials, which offer enhanced durability, reduced wear, and improved overall function. The demand for knee replacement surgeries is expected to continue growing, driven by factors such as the aging population, increasing obesity rates, and the rising incidence of knee injuries, particularly among athletes. As a result, knee reconstruction devices are poised to maintain their dominant position in the market, with ongoing improvements in surgical techniques and implant designs further supporting their widespread use.

Total Joint Replacement Is Largest Procedure Type Due to Proven Effectiveness and Widespread Adoption

Total joint replacement (TJR) is the largest procedure type in the joint reconstruction market, owing to its proven effectiveness in relieving pain, restoring mobility, and improving quality of life for patients suffering from severe joint degeneration. Total joint replacement involves the surgical removal of a damaged joint and the implantation of a prosthetic device, and is commonly performed for the knee, hip, and shoulder joints. The procedure has become the standard treatment for advanced osteoarthritis and other degenerative joint conditions, especially in elderly patients who experience significant impairment in their daily activities.

The popularity of total joint replacement is also driven by the long-term benefits it provides, including improved joint function, reduced pain, and enhanced mobility, leading to better patient outcomes and a higher quality of life. Technological advancements in surgical techniques, such as minimally invasive procedures, along with the development of more durable and biocompatible implant materials, have made total joint replacement surgeries safer and more effective, further driving their adoption. As the global population continues to age, the demand for total joint replacement procedures is expected to remain strong, fueling the growth of the joint reconstruction market.

Hospitals Are Largest End-User Segment Due to High Volume of Joint Reconstruction Surgeries

Hospitals are the largest end-user segment in the joint reconstruction market, primarily due to the high volume of joint reconstruction surgeries performed in these settings. Hospitals are equipped with the necessary surgical infrastructure, specialized medical teams, and post-operative care facilities to handle complex procedures like total and partial joint replacements. The prevalence of joint disorders, coupled with the increasing adoption of joint reconstruction surgeries, has made hospitals the primary providers of these services.

In addition to their capacity for handling a large number of surgeries, hospitals also play a key role in implementing cutting-edge surgical technologies, such as robotic-assisted surgeries and advanced imaging systems, which enhance the precision and safety of joint reconstruction procedures. As the demand for joint reconstruction surgeries continues to grow, hospitals will remain the dominant end-users of joint reconstruction devices, with a focus on improving surgical outcomes, reducing recovery times, and offering comprehensive patient care before, during, and after the procedure.

Metal Is Largest Material Type Due to Strength, Durability, and Biocompatibility

Metal is the largest material type in the joint reconstruction market, largely due to its strength, durability, and biocompatibility, making it an ideal choice for prosthetic components. Materials such as titanium and cobalt-chromium alloys are commonly used in joint reconstruction devices, particularly for knee and hip implants, due to their ability to withstand the mechanical stresses placed on joints during movement. Metals are known for their longevity and resistance to wear, which is crucial for ensuring the long-term success of joint replacement surgeries.

The popularity of metal materials is also driven by their ability to integrate well with bone tissue, reducing the risk of implant failure and promoting better outcomes. In addition to their strength and durability, metal implants can be designed to closely mimic the natural movement of joints, further improving patient satisfaction and functionality. As demand for joint reconstruction procedures increases, the use of metal materials in implants will continue to dominate, with ongoing research into new metal alloys and surface coatings to enhance performance and reduce complications.

North America Is Largest Region Due to Advanced Healthcare Infrastructure and High Adoption Rates

North America is the largest region in the joint reconstruction market, driven by advanced healthcare infrastructure, high adoption rates of joint replacement surgeries, and a growing elderly population. The United States, in particular, has a high incidence of joint-related disorders, particularly among the aging population, leading to a significant demand for joint reconstruction procedures. The region also benefits from the availability of state-of-the-art medical technologies and highly skilled orthopedic surgeons, ensuring the widespread adoption of joint replacement surgeries.

In addition to the aging population, increasing awareness of joint reconstruction options and improvements in healthcare access are contributing to the growth of the market in North America. The presence of leading medical device manufacturers and orthopedic implant companies in the region also supports market expansion, with ongoing innovations in surgical techniques and implant materials. As the demand for joint reconstruction procedures continues to rise, North America is expected to maintain its dominant position in the global market.

Competitive Landscape and Leading Companies

The joint reconstruction market is highly competitive, with several global players focusing on innovation, product development, and strategic partnerships to maintain market leadership. Leading companies in the market include Zimmer Biomet, Stryker Corporation, DePuy Synthes (Johnson & Johnson), and Smith & Nephew, which offer a wide range of joint reconstruction products for knee, hip, and shoulder surgeries. These companies are investing heavily in research and development to improve implant designs, enhance material properties, and integrate advanced surgical technologies, such as robotics and computer-assisted surgery.

As the market continues to evolve, competition is intensifying, with a focus on delivering customized and patient-specific solutions to improve surgical outcomes. Companies are also exploring the use of new materials, such as ceramic and composite, to further enhance implant performance and longevity. The competitive landscape is expected to remain dynamic, with ongoing advancements in joint reconstruction technologies and the growing adoption of minimally invasive surgical techniques driving market growth.

Recent Developments:

- In December 2024, Zimmer Biomet Holdings, Inc. announced the launch of a new 3D-printed knee implant designed to improve patient outcomes and reduce recovery times.

- In November 2024, Stryker Corporation introduced a next-generation hip replacement system that incorporates advanced materials for enhanced durability and mobility.

- In October 2024, Medtronic PLC unveiled a robotic-assisted system for knee joint replacement surgeries to improve precision and patient recovery.

- In September 2024, Johnson & Johnson (DePuy Synthes) launched a new ceramic hip implant designed to reduce wear and improve longevity in younger patients.

- In August 2024, Smith & Nephew Plc announced the acquisition of an orthopedic robotics company to enhance its joint reconstruction portfolio with robotic-assisted surgery solutions.

List of Leading Companies:

- Zimmer Biomet Holdings, Inc.

- Stryker Corporation

- Johnson & Johnson (DePuy Synthes)

- Smith & Nephew Plc

- Medtronic PLC

- Exactech, Inc.

- DJO Global, Inc.

- CONMED Corporation

- Arthrex, Inc.

- B. Braun Melsungen AG

- NuVasive, Inc.

- Wright Medical Group N.V.

- MicroPort Scientific Corporation

- Healthcare Co., Ltd. (HDC)

- KCI Medical

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 15.4 Billion |

|

Forecasted Value (2030) |

USD 25.6 Billion |

|

CAGR (2025 – 2030) |

7.6% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Joint Reconstruction Market by Product Type (Knee Reconstruction Devices, Hip Reconstruction Devices, Shoulder Reconstruction Devices, Ankle Reconstruction Devices, Elbow Reconstruction Devices), Material (Metal, Polyethylene, Ceramic, Composite), Procedure Type (Total Joint Replacement, Partial Joint Replacement, Revision Surgery), End-User (Hospitals, Orthopedic Clinics, Ambulatory Surgical Centers) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Zimmer Biomet Holdings, Inc., Stryker Corporation, Johnson & Johnson (DePuy Synthes), Smith & Nephew Plc, Medtronic PLC, Exactech, Inc., DJO Global, Inc., CONMED Corporation, Arthrex, Inc., B. Braun Melsungen AG, NuVasive, Inc., Wright Medical Group N.V., MicroPort Scientific Corporation, Healthcare Co., Ltd. (HDC), KCI Medical |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Joint Reconstruction Market, by Product Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Knee Reconstruction Devices |

|

4.2. Hip Reconstruction Devices |

|

4.3. Shoulder Reconstruction Devices |

|

4.4. Ankle Reconstruction Devices |

|

4.5. Elbow Reconstruction Devices |

|

5. Joint Reconstruction Market, by Material (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Metal |

|

5.2. Polyethylene |

|

5.3. Ceramic |

|

5.4. Composite |

|

6. Joint Reconstruction Market, by Procedure Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Total Joint Replacement |

|

6.2. Partial Joint Replacement |

|

6.3. Revision Surgery |

|

7. Joint Reconstruction Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Hospitals |

|

7.2. Orthopedic Clinics |

|

7.3. Ambulatory Surgical Centers |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Joint Reconstruction Market, by Product Type |

|

8.2.7. North America Joint Reconstruction Market, by Material |

|

8.2.8. North America Joint Reconstruction Market, by Procedure Type |

|

8.2.9. North America Joint Reconstruction Market, by End-User |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Joint Reconstruction Market, by Product Type |

|

8.2.10.1.2. US Joint Reconstruction Market, by Material |

|

8.2.10.1.3. US Joint Reconstruction Market, by Procedure Type |

|

8.2.10.1.4. US Joint Reconstruction Market, by End-User |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Zimmer Biomet Holdings, Inc. |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Stryker Corporation |

|

10.3. Johnson & Johnson (DePuy Synthes) |

|

10.4. Smith & Nephew Plc |

|

10.5. Medtronic PLC |

|

10.6. Exactech, Inc. |

|

10.7. DJO Global, Inc. |

|

10.8. CONMED Corporation |

|

10.9. Arthrex, Inc. |

|

10.10. B. Braun Melsungen AG |

|

10.11. NuVasive, Inc. |

|

10.12. Wright Medical Group N.V. |

|

10.13. MicroPort Scientific Corporation |

|

10.14. Healthcare Co., Ltd. (HDC) |

|

10.15. KCI Medical |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Joint Reconstruction Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Joint Reconstruction Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Joint Reconstruction Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA