As per Intent Market Research, the IV Dressing Market was valued at USD 1.3 Million in 2024-e and will surpass USD 2.2 Million by 2030; growing at a CAGR of 7.7% during 2025-2030.

The IV dressing market is a critical segment within the broader wound care and medical supplies industry, catering to the growing need for infection prevention, wound healing, and patient safety in healthcare settings. As intravenous (IV) therapy becomes increasingly widespread across various patient demographics, the demand for advanced IV dressing solutions continues to rise. These dressings are essential for safeguarding the IV catheter site, reducing the risk of infection, and promoting optimal healing, especially in high-risk patient groups such as those in hospitals and home healthcare. The market is influenced by factors such as the increasing prevalence of chronic diseases, the expanding healthcare infrastructure, and the growing awareness regarding the importance of infection control.

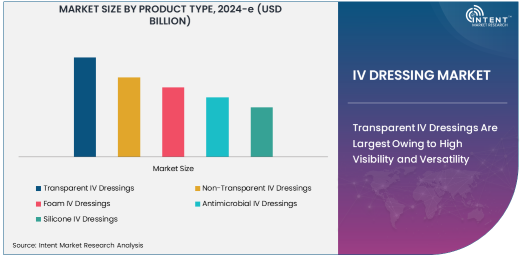

Transparent IV Dressings Are Largest Owing to High Visibility and Versatility

Transparent IV dressings dominate the IV dressing market due to their versatility and practical benefits for both healthcare professionals and patients. These dressings offer clear visibility of the catheter insertion site, enabling quick assessments for any signs of infection, inflammation, or other complications. The clear nature of these dressings makes them particularly useful in hospital settings, where frequent monitoring of IV sites is necessary. They are widely used across various applications, including surgical wounds, trauma wounds, and chronic conditions requiring prolonged IV access. Transparent IV dressings also have superior adhesion, making them an ideal choice for patients with active lifestyles or those who need longer-term catheter placements.

The transparency of these dressings aids in reducing unnecessary dressing changes, thus lowering the overall risk of infections and promoting faster healing. As healthcare providers continue to prioritize both patient comfort and safety, transparent IV dressings are expected to remain the largest segment of the market. With technological advances in materials, these dressings are also becoming more durable, breathable, and flexible, which further enhances their market appeal.

Hospitals Lead the End-User Industry with High Volume IV Usage

Hospitals represent the largest end-user industry in the IV dressing market due to the high volume of intravenous therapies conducted in these settings. IV therapy is a standard procedure in hospitals for administering medications, fluids, and blood products, which creates a constant demand for IV dressings to secure catheter sites and prevent complications like infections. Hospitals require a wide range of IV dressing solutions that can cater to different patient needs, including those undergoing surgery, long-term treatments, or trauma recovery. This heavy reliance on IV dressings makes hospitals the largest consumers of these products, further driving the growth of the market.

In addition, hospitals typically have stringent hygiene protocols and infection prevention strategies, which increases the use of high-quality, advanced IV dressings such as antimicrobial and transparent options. The consistent need for IV access, coupled with rising patient numbers, ensures that hospitals remain the dominant force in the market, making up a significant portion of the global demand for IV dressings.

Surgical Wounds Segment is Fastest Growing Owing to Increased Surgical Procedures

The surgical wounds segment is the fastest growing in the IV dressing market, driven by the increase in surgical procedures worldwide. As medical technology advances, the volume of both elective and emergency surgeries has been steadily rising. This results in a greater need for postoperative care, including the use of IV dressings to protect surgical wounds and facilitate recovery. Surgical wounds often require delicate handling and protection, and advanced IV dressings play a key role in preventing infections and promoting optimal healing.

The demand for surgical wound care products, including IV dressings, is also increasing with the rise in minimally invasive surgeries and outpatient procedures. These surgeries often necessitate IV therapy, which increases the need for dressings that can ensure secure catheter placement while reducing the risk of complications. As the number of surgeries grows globally, the surgical wounds segment is expected to maintain a rapid growth trajectory in the coming years.

Online Retail is Fastest Growing Distribution Channel Owing to Convenience and Accessibility

The online retail segment is the fastest growing distribution channel in the IV dressing market, driven by the increasing preference for convenience and accessibility among healthcare providers and consumers. With the rise of e-commerce platforms, hospitals, clinics, and home healthcare providers are increasingly purchasing medical supplies online. Online retail offers numerous advantages, including faster procurement, competitive pricing, and the ability to access a wide variety of IV dressings from different manufacturers. Furthermore, the ability to have products delivered directly to healthcare facilities or patients' homes adds to the appeal of online purchasing.

The convenience of online retail allows healthcare providers to place orders at any time, making it an essential distribution channel, especially for clinics and home healthcare markets. With the increasing adoption of e-commerce platforms for medical supplies, online retail is poised to continue its rapid growth in the IV dressing market.

North America Is Largest Region Owing to Robust Healthcare Infrastructure

North America is the largest region in the IV dressing market, driven by the region's robust healthcare infrastructure, high healthcare spending, and widespread adoption of advanced medical technologies. The United States, in particular, accounts for a significant share of the market, with a high demand for IV dressing products in hospitals, clinics, and home healthcare settings. The region’s well-established healthcare system, coupled with a growing aging population and an increasing number of chronic disease cases, further fuels the demand for IV dressing solutions.

North American healthcare facilities are also more likely to adopt high-quality, advanced IV dressings, such as antimicrobial and transparent dressings, which enhance patient outcomes. Moreover, the region's focus on infection control, patient safety, and improved healthcare standards supports the strong growth of the IV dressing market.

Competitive Landscape

Leading companies in the IV dressing market include 3M Health Care, Smith & Nephew, Medtronic, ConvaTec, and Baxter International, among others. These companies have established a strong foothold by offering a wide range of IV dressing solutions catering to various medical applications, including surgical wounds, trauma wounds, and chronic conditions. Their product portfolios include both advanced dressings, such as antimicrobial and silicone-based options, as well as traditional transparent and non-transparent dressings.

The competitive landscape is characterized by continuous product innovation, with manufacturers focusing on improving the performance, comfort, and durability of their IV dressings. In addition, companies are increasingly collaborating with healthcare providers to develop customized solutions tailored to specific patient needs. With an emphasis on expanding their market presence through both offline and online distribution channels, leading companies are well-positioned to capitalize on the growing demand for IV dressings globally.

The competitive landscape is characterized by continuous product innovation, with manufacturers focusing on improving the performance, comfort, and durability of their IV dressings. In addition, companies are increasingly collaborating with healthcare providers to develop customized solutions tailored to specific patient needs. With an emphasis on expanding their market presence through both offline and online distribution channels, leading companies are well-positioned to capitalize on the growing demand for IV dressings globally.

Recent Developments:

- 3M Health Care recently launched a new antimicrobial IV dressing designed to enhance patient comfort and reduce infection risks during IV treatments.

- Smith & Nephew has expanded its product range in the wound care space, including advanced IV dressings that support faster healing and infection prevention.

- Medtronic acquired Mazor Robotics, and the move is expected to enhance their ability to offer advanced medical devices like IV-related products.

- ConvaTec entered a strategic partnership with a leading healthcare provider to increase the availability of IV dressing solutions in hospitals.

- Baxter International received regulatory approval for a new range of IV dressing products designed for pediatric and geriatric patients, further expanding their market reach.

List of Leading Companies:

- 3M Health Care

- Smith & Nephew

- Medtronic

- ConvaTec

- Baxter International

- Cardinal Health

- Johnson & Johnson

- Hollister Incorporated

- Mölnlycke Health Care

- BD (Becton, Dickinson and Company)

- Covidien (Medtronic)

- DermaRite Industries, LLC

- KCI Medical

- Medline Industries

- Paul Hartmann AG

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 1.3 Million |

|

Forecasted Value (2030) |

USD 2.2 Million |

|

CAGR (2025 – 2030) |

7.7% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

IV Dressing Market Product Type (Transparent IV Dressings, Non-Transparent IV Dressings, Foam IV Dressings, Antimicrobial IV Dressings, Silicone IV Dressings), End-User (Hospitals, Clinics, Home Healthcare, Ambulatory Surgical Centers, Long-Term Care Facilities), Application (Surgical Wounds, Trauma Wounds, Chronic Wounds, Acute Wounds, Burns), and Distribution Channel (Direct Sales, Online Retail, Wholesalers, Hospitals & Clinics, Specialty Stores); |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

3M Health Care, Smith & Nephew, Medtronic, ConvaTec, Baxter International, Cardinal Health, Johnson & Johnson, Hollister Incorporated, Mölnlycke Health Care, BD (Becton, Dickinson and Company), Covidien (Medtronic), DermaRite Industries, LLC, KCI Medical, Medline Industries, Paul Hartmann AG |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. IV Dressing Market, by Product Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Transparent IV Dressings |

|

4.2. Non-Transparent IV Dressings |

|

4.3. Foam IV Dressings |

|

4.4. Antimicrobial IV Dressings |

|

4.5. Silicone IV Dressings |

|

5. IV Dressing Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Hospitals |

|

5.2. Clinics |

|

5.3. Home Healthcare |

|

5.4. Ambulatory Surgical Centers |

|

5.5. Long-term Care Facilities |

|

6. IV Dressing Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Surgical Wounds |

|

6.2. Trauma Wounds |

|

6.3. Chronic Wounds |

|

6.4. Acute Wounds |

|

6.5. Burns |

|

7. IV Dressing Market, by Distribution Channel (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Direct Sales |

|

7.2. Online Retail |

|

7.3. Wholesalers |

|

7.4. Hospitals & Clinics |

|

7.5. Specialty Stores |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America IV Dressing Market, by Product Type |

|

8.2.7. North America IV Dressing Market, by End-User |

|

8.2.8. North America IV Dressing Market, by Application |

|

8.2.9. North America IV Dressing Market, by Distribution Channel |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US IV Dressing Market, by Product Type |

|

8.2.10.1.2. US IV Dressing Market, by End-User |

|

8.2.10.1.3. US IV Dressing Market, by Application |

|

8.2.10.1.4. US IV Dressing Market, by Distribution Channel |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. 3M Health Care |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Smith & Nephew |

|

10.3. Medtronic |

|

10.4. ConvaTec |

|

10.5. Baxter International |

|

10.6. Cardinal Health |

|

10.7. Johnson & Johnson |

|

10.8. Hollister Incorporated |

|

10.9. Mölnlycke Health Care |

|

10.10. BD (Becton, Dickinson and Company) |

|

10.11. Covidien (Medtronic) |

|

10.12. DermaRite Industries, LLC |

|

10.13. KCI Medical |

|

10.14. Medline Industries |

|

10.15. Paul Hartmann AG |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the IV Dressing Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the IV Dressing Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the IV Dressing Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA