As per Intent Market Research, the Infrastructure as a Service (IaaS) Market was valued at USD 108.2 Billion in 2024-e and will surpass USD 328.8 Billion by 2030; growing at a CAGR of 20.3% during 2025-2030.

The Infrastructure as a Service (IaaS) market is a rapidly growing segment within the cloud computing industry, driven by businesses' increasing need for scalable, cost-effective, and flexible IT infrastructure. IaaS allows organizations to rent computing resources such as storage, networking, and processing power, eliminating the need for on-premise hardware investments. This model supports various industries, including IT & telecommunications, BFSI, healthcare, and manufacturing, by offering efficient, on-demand infrastructure to meet dynamic business requirements.

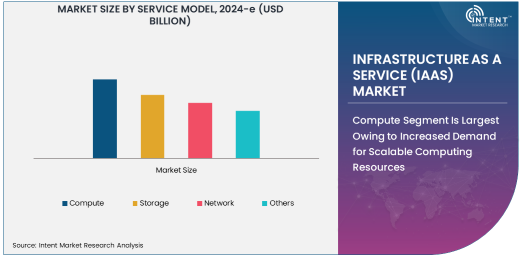

Compute Segment Is Largest Owing to Increased Demand for Scalable Computing Resources

The Infrastructure as a Service (IaaS) market has been experiencing robust growth due to the rising need for scalable, flexible, and cost-efficient cloud solutions. IaaS offers computing resources, storage, and networking infrastructure through the cloud, enabling businesses to avoid the high costs and complexity of owning and managing physical servers. Among various service models, the Compute segment leads the market, driven by the increasing demand for computing power to run applications, host websites, and support critical business operations. As businesses continue to shift towards cloud computing, the need for high-performance compute resources is becoming essential for handling large-scale, data-intensive applications, from artificial intelligence (AI) to big data analytics.

The Compute segment is rapidly expanding due to its central role in cloud infrastructure. Companies are increasingly adopting IaaS to handle workloads that require significant processing power, such as machine learning, data analysis, and high-performance computing (HPC). The growing trend of digital transformation across industries has resulted in an uptick in demand for compute services, as businesses strive to improve their agility and scalability. Furthermore, the rise in remote work, data-driven applications, and AI development is creating a steady demand for compute resources that can adapt to fluctuating workloads and optimize operational efficiency.

Hybrid Cloud Deployment Is Fastest Growing Due to Flexibility and Scalability

The Hybrid Cloud deployment model is seeing the fastest growth within the IaaS market. This model combines the benefits of both public and private clouds, offering organizations the flexibility to host workloads in the most suitable environment. The increasing preference for hybrid cloud solutions stems from the ability to maintain control over critical applications while leveraging the scalability of public cloud resources. This growing demand for hybrid cloud services is being driven by businesses looking for a balance between data security, cost-efficiency, and the need for flexibility in cloud deployments.

The Hybrid Cloud model allows organizations to optimize their existing IT infrastructure while taking advantage of the scalability and cost savings provided by public cloud services. Companies in industries such as healthcare, finance, and government are increasingly adopting hybrid cloud solutions to ensure compliance with regulations, secure sensitive data, and improve operational efficiency. The growing shift towards hybrid cloud adoption is also supported by the increasing availability of advanced technologies and services that enable seamless integration between private and public cloud environments.

IT & Telecommunications End-User Industry Is Largest Owing to High Dependence on Scalable Infrastructure

The IT & Telecommunications sector is the largest end-user industry within the IaaS market. This industry is highly dependent on scalable, cost-effective, and reliable infrastructure to support its complex network operations and data storage requirements. The demand for IaaS in this sector is driven by the need for constant network upgrades, faster data transmission, and the growing adoption of 5G technology. Telecommunication companies are leveraging IaaS to deploy software-defined networks (SDN) and network functions virtualization (NFV), which enhances the flexibility and efficiency of their infrastructure.

The IT & Telecommunications industry relies heavily on cloud computing to manage increasing data traffic, improve network performance, and offer more innovative services to customers. By adopting IaaS, telecom companies can scale their infrastructure without investing in expensive physical hardware, enabling them to meet growing demands for bandwidth, storage, and computing power. As the sector continues to evolve with new technologies like 5G and the Internet of Things (IoT), the need for robust and scalable IaaS solutions will continue to expand.

Large Enterprises Account for the Largest Share Owing to High Infrastructure Demands

In terms of organization size, Large Enterprises dominate the IaaS market. These companies tend to have extensive IT infrastructure needs and a high volume of data processing requirements. Large enterprises typically have the resources to invest in robust cloud solutions that support large-scale business operations, from global supply chains to customer relationship management (CRM). Their need for scalability, flexibility, and cost-effective solutions makes IaaS an ideal model for supporting business operations, reducing capital expenditures, and ensuring smooth business continuity.

Large enterprises benefit from the pay-as-you-go pricing model of IaaS, which allows them to scale their infrastructure based on demand. This capability is particularly important for enterprises that experience fluctuating workloads or seasonal spikes in demand. The ability to scale resources up or down as needed helps large organizations maintain operational efficiency while minimizing wasteful expenditures. As more enterprises embark on digital transformation journeys, the demand for IaaS solutions that can support complex, mission-critical operations continues to rise.

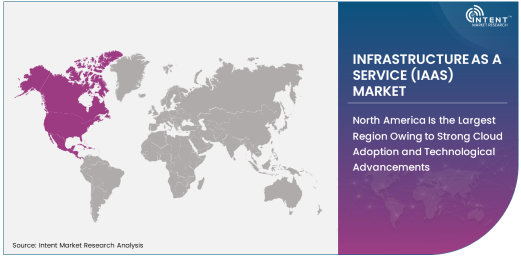

North America Is the Largest Region Owing to Strong Cloud Adoption and Technological Advancements

North America stands as the largest region in the IaaS market, owing to its early adoption of cloud technologies, well-established IT infrastructure, and presence of leading IaaS providers like Amazon Web Services (AWS), Microsoft Azure, and Google Cloud. The region has seen widespread digital transformation across industries, with businesses adopting IaaS to improve operational agility, reduce costs, and enhance scalability. Strong demand from sectors such as IT, BFSI, retail, and healthcare has further fueled the growth of IaaS in the region.

North America's position as the largest market is also supported by the region's advanced technological landscape, which fosters innovation and the development of new cloud-based solutions. The increasing deployment of artificial intelligence, machine learning, and big data analytics tools within enterprises has propelled the need for more powerful and flexible infrastructure, which IaaS provides. Additionally, government initiatives aimed at promoting cloud adoption and the growing trend of remote work and digital collaboration are expected to continue driving the demand for IaaS solutions across North America.

Competitive Landscape and Leading Companies in the IaaS Market

The IaaS market is highly competitive, with several global players leading the market. Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform are the top three players, commanding the largest share of the market due to their extensive infrastructure, advanced technologies, and global reach. Other notable players include IBM Cloud, Oracle Cloud, and Alibaba Cloud, all of which are continuously innovating and expanding their service offerings to cater to the growing demand for scalable cloud infrastructure.

These companies are focusing on strengthening their market positions through strategic partnerships, acquisitions, and the launch of new services. For instance, AWS continues to enhance its cloud capabilities by introducing services in areas such as machine learning, IoT, and serverless computing. Similarly, Microsoft Azure and Google Cloud are working to build stronger hybrid cloud solutions and integrated AI services. As the IaaS market continues to mature, competition will intensify, with companies focusing on cost optimization, security enhancements, and offering tailored solutions to meet the unique needs of businesses across different industries.

List of Leading Companies:

- Amazon Web Services (AWS)

- Microsoft Azure

- Google Cloud Platform

- IBM Cloud

- Oracle Cloud

- Alibaba Cloud

- DigitalOcean

- Rackspace Technology

- Salesforce

- Huawei Cloud

- VMware

- Tencent Cloud

- SAP

- Alibaba Cloud

- Joyent

Recent Developments:

- Amazon Web Services (AWS) announced the launch of its new cloud data center in Asia-Pacific, aimed at expanding its regional presence and providing localized services to customers.

- Microsoft Azure has entered into a strategic partnership with a major telecommunications company to enhance the delivery of 5G-enabled IaaS solutions.

- Google Cloud introduced new enhanced security features for its IaaS offering, including advanced encryption and multi-factor authentication to address growing cybersecurity concerns.

- Oracle Cloud acquired a leading cloud-native technology company to bolster its cloud infrastructure services and expand its customer base in the European market.

- IBM Cloud launched a new hybrid cloud platform combining IaaS and PaaS to help businesses scale their digital transformation efforts while enhancing their hybrid cloud capabilities.

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 108.2 Billion |

|

Forecasted Value (2030) |

USD 328.8 Billion |

|

CAGR (2025 – 2030) |

20.3% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Infrastructure as a Service (IaaS) Market By Service Model (Compute, Storage, Network), By Deployment (Public Cloud, Private Cloud, Hybrid Cloud), By End-User Industry (IT & Telecommunications, BFSI, Healthcare, Manufacturing, Retail, Government), By Organization Size (Small & Medium Enterprises, Large Enterprises) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Amazon Web Services (AWS), Microsoft Azure, Google Cloud Platform, IBM Cloud, Oracle Cloud, Alibaba Cloud, DigitalOcean, Rackspace Technology, Salesforce, Huawei Cloud, VMware, Tencent Cloud, SAP, Alibaba Cloud, Joyent |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Infrastructure as a Service (IaaS) Market, by Service Model (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Compute |

|

4.2. Storage |

|

4.3. Network |

|

4.4. Others |

|

5. Infrastructure as a Service (IaaS) Market, by Deployment (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Public Cloud |

|

5.2. Private Cloud |

|

5.3. Hybrid Cloud |

|

6. Infrastructure as a Service (IaaS) Market, by End-User Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. IT & Telecommunications |

|

6.2. BFSI (Banking, Financial Services & Insurance) |

|

6.3. Healthcare |

|

6.4. Manufacturing |

|

6.5. Retail |

|

6.6. Government |

|

6.7. Others |

|

7. Infrastructure as a Service (IaaS) Market, by Organization Size (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Small & Medium Enterprises (SMEs) |

|

7.2. Large Enterprises |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Infrastructure as a Service (IaaS) Market, by Service Model |

|

8.2.7. North America Infrastructure as a Service (IaaS) Market, by Deployment |

|

8.2.8. North America Infrastructure as a Service (IaaS) Market, by End-User Industry |

|

8.2.9. North America Infrastructure as a Service (IaaS) Market, by Organization Size |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Infrastructure as a Service (IaaS) Market, by Service Model |

|

8.2.10.1.2. US Infrastructure as a Service (IaaS) Market, by Deployment |

|

8.2.10.1.3. US Infrastructure as a Service (IaaS) Market, by End-User Industry |

|

8.2.10.1.4. US Infrastructure as a Service (IaaS) Market, by Organization Size |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Amazon Web Services (AWS) |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Microsoft Azure |

|

10.3. Google Cloud Platform |

|

10.4. IBM Cloud |

|

10.5. Oracle Cloud |

|

10.6. Alibaba Cloud |

|

10.7. DigitalOcean |

|

10.8. Rackspace Technology |

|

10.9. Salesforce |

|

10.10. Huawei Cloud |

|

10.11. VMware |

|

10.12. Tencent Cloud |

|

10.13. SAP |

|

10.14. Alibaba Cloud |

|

10.15. Joyent |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Infrastructure as a Service Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Infrastructure as a Service Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Infrastructure as a Service Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA