As per Intent Market Research, the Infertility Drugs Market was valued at USD 3.0 Billion in 2024-e and will surpass USD 17.2 Billion by 2030; growing at a CAGR of 34.0% during 2025 - 2030.

The Infertility Drugs Market is witnessing robust growth driven by the increasing prevalence of infertility globally, coupled with advancements in fertility treatments. Infertility affects both men and women, prompting a rising demand for effective treatments. Infertility drugs, including clomiphene citrate, gonadotropins, and letrozole, play a critical role in aiding conception by stimulating ovulation and improving reproductive health. As lifestyle changes, delayed marriages, and environmental factors contribute to fertility challenges, the market for infertility drugs has become increasingly essential, particularly in fertility clinics and hospitals where treatment is provided.

In recent years, there has been a surge in demand for infertility treatments, particularly among women experiencing hormonal imbalances or ovulation issues. The growing awareness of available infertility treatments, alongside technological advancements in assisted reproductive technologies (ART), has further contributed to the market's expansion. Additionally, increased insurance coverage for fertility treatments and the rising success rates of infertility treatments have bolstered market growth, making infertility drugs more accessible to a wider range of patients.

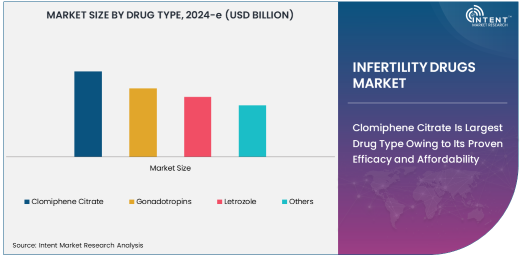

Clomiphene Citrate Is Largest Drug Type Owing to Its Proven Efficacy and Affordability

Clomiphene citrate is the largest drug type in the infertility drugs market due to its long-established efficacy and affordability in treating female infertility. This selective estrogen receptor modulator (SERM) is commonly used to induce ovulation in women who have irregular ovulation cycles or anovulation, and it is often the first-line treatment for women with polycystic ovary syndrome (PCOS). Clomiphene citrate works by stimulating the release of hormones necessary for ovulation, increasing the chances of conception.

The drug's widespread use in fertility clinics and hospitals, combined with its cost-effectiveness compared to other fertility drugs, has helped establish clomiphene citrate as a cornerstone in the management of female infertility. It has been proven to be successful in stimulating ovulation and improving pregnancy rates, making it a popular choice among healthcare providers. As a result, clomiphene citrate continues to dominate the infertility drug market, particularly in regions where affordability and accessibility to treatments are significant concerns.

Gonadotropins Are Fastest Growing Drug Type Due to Advanced Treatment Options

Gonadotropins are the fastest-growing drug type in the infertility drugs market, driven by their increasingly important role in assisted reproductive technologies (ART), such as in vitro fertilization (IVF). Gonadotropins, including human chorionic gonadotropin (hCG), follicle-stimulating hormone (FSH), and luteinizing hormone (LH), are used to stimulate the ovaries and increase the number of eggs produced during fertility treatments. They are often used in combination with other fertility drugs to maximize the chances of conception in women undergoing ART.

The growth in ART procedures, including IVF and egg freezing, has significantly boosted the demand for gonadotropins. These drugs allow for precise control over ovarian stimulation, leading to better outcomes in IVF cycles. Additionally, the increasing number of fertility clinics offering ART services has led to greater access to gonadotropins, driving the segment’s growth. As ART technologies continue to advance, gonadotropins are expected to see further adoption, making them one of the fastest-growing drug types in the infertility drugs market.

Fertility Clinics Are Largest End-Use Industry Due to High Volume of Specialized Treatments

Fertility clinics are the largest end-use industry in the infertility drugs market, owing to their specialized focus on treating infertility through a variety of methods, including the administration of infertility drugs. Fertility clinics offer comprehensive treatment programs that combine medications with assisted reproductive technologies such as IVF, intrauterine insemination (IUI), and egg donation. These clinics are well-equipped with advanced diagnostic tools and treatment options tailored to address the specific causes of infertility, whether it’s hormonal imbalances, ovulation disorders, or male infertility.

The concentrated focus on infertility treatments in fertility clinics makes them the primary location for the prescription and administration of infertility drugs. The increasing success rates of fertility treatments in these clinics, along with growing societal acceptance of fertility procedures, have contributed to the rising number of patients seeking care. Fertility clinics also provide personalized care and ongoing support throughout the treatment process, further cementing their role as the largest end-use industry for infertility drugs.

North America Is Largest Region Due to High Prevalence and Advanced Healthcare Infrastructure

North America is the largest region in the infertility drugs market, primarily due to the high prevalence of infertility, advanced healthcare infrastructure, and strong patient awareness of fertility treatments. The United States, in particular, has seen a growing demand for fertility services, driven by factors such as delayed childbearing, lifestyle changes, and the availability of advanced fertility treatments like IVF. In addition, North America has well-established fertility clinics that offer a wide range of infertility treatments, including the use of infertility drugs such as clomiphene citrate and gonadotropins.

The region benefits from robust healthcare policies, including insurance coverage for fertility treatments in some areas, which makes infertility drugs more accessible. Furthermore, the increasing availability of cutting-edge ART technologies, along with favorable reimbursement policies for fertility treatments, has helped North America maintain its dominance in the market. As fertility awareness continues to rise and more people seek treatment, North America is expected to continue leading the infertility drugs market.

Leading Companies and Competitive Landscape

The infertility drugs market is competitive, with several key players providing a wide range of products designed to address both male and female infertility. Prominent companies in this market include Merck & Co., Inc., Eli Lilly and Company, Bayer AG, Ferring Pharmaceuticals, and Sandoz, which offer a variety of infertility drugs, including clomiphene citrate, gonadotropins, and letrozole. These companies lead the market through their innovative approaches to fertility treatments, clinical research, and partnerships with fertility clinics and healthcare providers.

The competitive landscape is also characterized by ongoing product innovation, with companies focusing on improving the efficacy, safety, and delivery methods of infertility drugs. Additionally, the growing trend of personalized fertility treatments has encouraged companies to develop drugs that cater to specific patient needs, further driving competition. As the demand for infertility treatments continues to rise, leading companies are investing in new drug development, partnerships, and expanding their global presence to strengthen their positions in the market.

Recent Developments:

- Merck & Co. announced the launch of a new infertility drug aimed at improving the success rates of in vitro fertilization (IVF) treatments.

- Bayer AG expanded its fertility product portfolio by acquiring a leading player in the hormonal therapy space.

- Ferring Pharmaceuticals launched a new gonadotropin-based drug for female infertility that promises fewer side effects and higher efficacy.

- Eli Lilly and Company received FDA approval for its new oral drug for ovulation induction in women with polycystic ovary syndrome (PCOS).

- AbbVie Inc. entered a strategic partnership with a fertility clinic to enhance accessibility and distribution of its infertility treatment drugs worldwide.

List of Leading Companies:

- Merck & Co.

- Bayer AG

- Ferring Pharmaceuticals

- Eli Lilly and Company

- Sandoz (Novartis)

- Pfizer Inc.

- HCG Pharmaceuticals

- Icosavax, Inc.

- OvaScience

- AbbVie Inc.

- Sanofi

- Teva Pharmaceutical Industries

- Boehringer Ingelheim

- Zydus Cadila

- Mylan N.V.

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 3.0 Billion |

|

Forecasted Value (2030) |

USD 17.2 Billion |

|

CAGR (2025 – 2030) |

34.0% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Global Infertility Drugs Market by Drug Type (Clomiphene Citrate, Gonadotropins, Letrozole); Application (Female Infertility, Male Infertility); End-Use Industry (Fertility Clinics, Hospitals, Homecare) and by Region |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Merck & Co., Bayer AG, Ferring Pharmaceuticals, Eli Lilly and Company, Sandoz (Novartis), Pfizer Inc., Icosavax, Inc., OvaScience, AbbVie Inc., Sanofi, Teva Pharmaceutical Industries, Boehringer Ingelheim, Mylan N.V. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Infertility Drugs Market, by Drug Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Clomiphene Citrate |

|

4.2. Gonadotropins |

|

4.3. Letrozole |

|

4.4. Others |

|

5. Infertility Drugs Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Female Infertility |

|

5.2. Male Infertility |

|

6. Infertility Drugs Market, by End-Use Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Fertility Clinics |

|

6.2. Hospitals |

|

6.3. Homecare |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Infertility Drugs Market, by Drug Type |

|

7.2.7. North America Infertility Drugs Market, by Application |

|

7.2.8. North America Infertility Drugs Market, by End-Use Industry |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Infertility Drugs Market, by Drug Type |

|

7.2.9.1.2. US Infertility Drugs Market, by Application |

|

7.2.9.1.3. US Infertility Drugs Market, by End-Use Industry |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Merck & Co. |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Bayer AG |

|

9.3. Ferring Pharmaceuticals |

|

9.4. Eli Lilly and Company |

|

9.5. Sandoz (Novartis) |

|

9.6. Pfizer Inc. |

|

9.7. HCG Pharmaceuticals |

|

9.8. Icosavax, Inc. |

|

9.9. OvaScience |

|

9.10. AbbVie Inc. |

|

9.11. Sanofi |

|

9.12. Teva Pharmaceutical Industries |

|

9.13. Boehringer Ingelheim |

|

9.14. Zydus Cadila |

|

9.15. Mylan N.V. |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Infertility Drugs Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Infertility Drugs Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Infertility Drugs Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA