As per Intent Market Research, the Industrial Transmission Substation Market was valued at USD 14.7 billion in 2023 and will surpass USD 20.8 billion by 2030; growing at a CAGR of 5.1% during 2024 - 2030.

The industrial transmission substation market is integral to the efficient transmission and distribution of electrical power across regions and industries. Substations play a crucial role in converting voltage levels from high to low, ensuring the stable flow of electricity through transmission networks. With the global emphasis on upgrading infrastructure, modernizing grids, and integrating renewable energy sources, the market for industrial transmission substations is witnessing substantial growth. Key components such as circuit breakers, transformers, switchgear, and busbars are essential for the seamless operation of these substations, making them critical for industrial development.

As power generation capacities expand and energy consumption grows, the need for substations that support higher voltages, advanced technologies, and more efficient operations is increasing. This demand is further accelerated by the growing adoption of renewable energy sources, which require new types of substations to integrate energy into the grid. The focus is shifting towards more reliable, safer, and cost-effective solutions, driving the market towards innovations in technology and design.

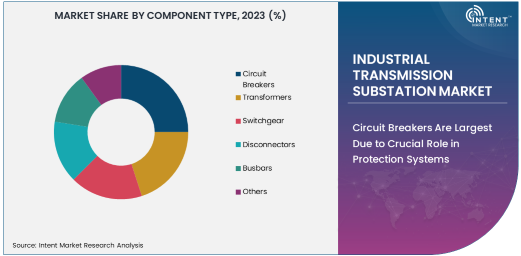

Circuit Breakers Are Largest Due to Crucial Role in Protection Systems

The circuit breaker segment is the largest in the industrial transmission substation market, primarily due to its vital role in ensuring the safety and reliability of substations. Circuit breakers are essential for interrupting fault currents and protecting electrical circuits from damage caused by overloads or short circuits. Their primary function is to provide rapid disconnection in case of abnormal conditions, preventing further damage to equipment and ensuring the safe operation of the substation.

The growing need for protection systems in power transmission and distribution networks is driving the demand for circuit breakers. These components are particularly important in high-voltage substations where the risk of faults is higher. As industries expand and the demand for electricity grows, the circuit breaker segment is poised to maintain its dominance, making it a critical component in the design and operation of modern substations.

Gas-Insulated Substations Are Fastest Growing Due to Space Efficiency and Reliability

Gas-insulated substations (GIS) are the fastest-growing segment in the industrial transmission substation market, owing to their compact design and reliability. GIS technology uses sulfur hexafluoride (SF6) gas to insulate electrical components, allowing for a more compact substation design compared to traditional air-insulated substations (AIS). This compactness makes GIS ideal for urban environments or areas with limited space for substation infrastructure.

In addition to space efficiency, GIS offers superior performance, especially in harsh environmental conditions, due to its high insulation properties and resistance to environmental influences like pollution and moisture. As cities expand and the need for space-saving solutions in electrical infrastructure grows, the demand for GIS technology continues to rise, making it the fastest-growing substation technology in the market.

High Voltage Substations Are Largest Due to Growing Power Demands

High-voltage substations (above 110 kV) represent the largest segment in the industrial transmission substation market, driven by the increasing demand for power transmission over long distances. These substations are essential for transferring electricity from power plants to distribution networks, where the voltage is stepped down for consumption. With the global rise in industrialization and population growth, the need for high-capacity substations to manage and distribute electricity efficiently is critical.

High-voltage substations also play a pivotal role in integrating renewable energy sources such as wind and solar power into the grid. As the focus on clean energy increases, the need for robust high-voltage substations to accommodate the varying and unpredictable nature of renewable energy becomes more pronounced. This growing demand for reliable and efficient power transmission infrastructure ensures the continued dominance of the high-voltage substation segment.

Power Generation Industry Is Largest End-Use Segment Due to Energy Infrastructure Expansion

The power generation industry is the largest end-use segment in the industrial transmission substation market, driven by the continuous expansion of global energy infrastructure. Power generation plants, whether fossil fuel-based, nuclear, or renewable, require substations to step up the voltage for transmission across the grid. The increasing demand for electricity to support economic growth, urbanization, and technological advancements has significantly increased the need for substations that can handle high voltages and ensure efficient power distribution.

In addition to traditional power generation, the rising demand for renewable energy sources such as wind, solar, and hydropower further fuels the need for specialized substations. These plants require advanced transmission solutions that can handle fluctuating power inputs from renewable sources. As the energy sector continues to evolve, the power generation industry remains the largest consumer of industrial transmission substations.

North America Is Largest Region Due to Strong Energy Infrastructure

North America is the largest region in the industrial transmission substation market, owing to its well-established energy infrastructure and ongoing investments in upgrading power transmission systems. The United States and Canada are leaders in the deployment of advanced substations, including GIS and AIS technologies, to meet the growing energy demands of both urban and industrial sectors. Additionally, the increasing adoption of renewable energy sources in North America has further stimulated the demand for modern substations that can efficiently integrate diverse energy inputs into the grid.

North America’s strong industrial base, coupled with significant government initiatives aimed at upgrading power grids and improving energy efficiency, positions the region as the largest market for industrial transmission substations. The region’s focus on infrastructure development, smart grid technologies, and renewable energy adoption continues to drive the growth of the substation market, ensuring its continued leadership on the global stage.

Competitive Landscape

The industrial transmission substation market is highly competitive, with numerous global and regional players vying for market share. Key players in the market include Siemens AG, ABB Ltd., General Electric, Schneider Electric, and Mitsubishi Electric, which are at the forefront of technology development and innovation in substation equipment. These companies invest heavily in research and development to create advanced substation solutions that meet the growing demand for high-performance, reliable, and efficient transmission systems.

The competitive landscape is also influenced by the trend towards digitalization and automation, with companies increasingly offering smart substation solutions that integrate monitoring and control systems. This shift towards smart grid technologies is driving innovation and enabling companies to offer more comprehensive, integrated solutions to meet the evolving needs of the energy and industrial sectors. Partnerships, mergers, and acquisitions also play a significant role as companies look to expand their product offerings and enhance their market presence.

Recent Developments:

- In December 2024, Siemens AG launched a new range of modular substations designed to reduce installation time and improve efficiency for industrial applications.

- In November 2024, General Electric (GE) announced the successful commissioning of a large gas-insulated substation (GIS) for a major power generation facility in the Middle East.

- In October 2024, ABB Ltd. unveiled its advanced substation automation solution aimed at improving real-time monitoring and control in industrial transmission substations.

- In September 2024, Mitsubishi Electric Corporation secured a contract to provide high-voltage switchgear and transformers for a new industrial transmission substation in Southeast Asia.

- In August 2024, Schneider Electric SE completed the installation of a hybrid substation for a renewable energy plant, optimizing electricity transmission and integration with the power grid.

List of Leading Companies:

- Siemens AG

- ABB Ltd.

- Schneider Electric SE

- General Electric (GE)

- Mitsubishi Electric Corporation

- Eaton Corporation

- Toshiba Corporation

- Hitachi, Ltd.

- Hyundai Electric & Energy Systems Co.

- Bharat Heavy Electricals Limited (BHEL)

- Larsen & Toubro Limited

- Crompton Greaves

- Alstom Grid

- Emerson Electric Co.

- Crompton Greaves Consumer Electricals

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 14.7 billion |

|

Forecasted Value (2030) |

USD 20.8 billion |

|

CAGR (2024 – 2030) |

5.1% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Industrial Transmission Substation Market By Component Type (Circuit Breakers, Transformers, Switchgear, Disconnectors, Busbars), By Substation Type (Indoor Substation, Outdoor Substation), By Voltage Level (High Voltage (Above 110 kV), Medium Voltage (11 kV to 110 kV), Low Voltage (Below 11 kV)), By Technology Type (Gas-Insulated Substation (GIS), Air-Insulated Substation (AIS), Hybrid Substation, Modular Substation), By End-Use Industry (Power Generation, Oil & Gas, Mining, Renewable Energy, Heavy Industrial Applications) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Siemens AG, ABB Ltd., Schneider Electric SE, General Electric (GE), Mitsubishi Electric Corporation, Eaton Corporation, Toshiba Corporation, Hitachi, Ltd., Hyundai Electric & Energy Systems Co., Bharat Heavy Electricals Limited (BHEL), Larsen & Toubro Limited, Crompton Greaves, Alstom Grid, Emerson Electric Co., Crompton Greaves Consumer Electricals |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Industrial Transmission Substation Market, by Component Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Circuit Breakers |

|

4.2. Transformers |

|

4.3. Switchgear |

|

4.4. Disconnectors |

|

4.5. Busbars |

|

4.6. Others |

|

5. Industrial Transmission Substation Market, by Substation Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Indoor Substation |

|

5.2. Outdoor Substation |

|

6. Industrial Transmission Substation Market, by Voltage Level (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. High Voltage (Above 110 kV) |

|

6.2. Medium Voltage (11 kV to 110 kV) |

|

6.3. Low Voltage (Below 11 kV) |

|

7. Industrial Transmission Substation Market, by Technology Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Gas-Insulated Substation (GIS) |

|

7.2. Air-Insulated Substation (AIS) |

|

7.3. Hybrid Substation |

|

7.4. Modular Substation |

|

8. Industrial Transmission Substation Market, by End-Use Industry (Market Size & Forecast: USD Million, 2022 – 2030) |

|

8.1. Power Generation |

|

8.2. Oil & Gas |

|

8.3. Mining |

|

8.4. Renewable Energy |

|

8.5. Heavy Industrial Applications |

|

9. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

9.1. Regional Overview |

|

9.2. North America |

|

9.2.1. Regional Trends & Growth Drivers |

|

9.2.2. Barriers & Challenges |

|

9.2.3. Opportunities |

|

9.2.4. Factor Impact Analysis |

|

9.2.5. Technology Trends |

|

9.2.6. North America Industrial Transmission Substation Market, by Component Type |

|

9.2.7. North America Industrial Transmission Substation Market, by Substation Type |

|

9.2.8. North America Industrial Transmission Substation Market, by Voltage Level |

|

9.2.9. North America Industrial Transmission Substation Market, by Technology Type |

|

9.2.10. North America Industrial Transmission Substation Market, by End-Use Industry |

|

9.2.11. By Country |

|

9.2.11.1. US |

|

9.2.11.1.1. US Industrial Transmission Substation Market, by Component Type |

|

9.2.11.1.2. US Industrial Transmission Substation Market, by Substation Type |

|

9.2.11.1.3. US Industrial Transmission Substation Market, by Voltage Level |

|

9.2.11.1.4. US Industrial Transmission Substation Market, by Technology Type |

|

9.2.11.1.5. US Industrial Transmission Substation Market, by End-Use Industry |

|

9.2.11.2. Canada |

|

9.2.11.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

9.3. Europe |

|

9.4. Asia-Pacific |

|

9.5. Latin America |

|

9.6. Middle East & Africa |

|

10. Competitive Landscape |

|

10.1. Overview of the Key Players |

|

10.2. Competitive Ecosystem |

|

10.2.1. Level of Fragmentation |

|

10.2.2. Market Consolidation |

|

10.2.3. Product Innovation |

|

10.3. Company Share Analysis |

|

10.4. Company Benchmarking Matrix |

|

10.4.1. Strategic Overview |

|

10.4.2. Product Innovations |

|

10.5. Start-up Ecosystem |

|

10.6. Strategic Competitive Insights/ Customer Imperatives |

|

10.7. ESG Matrix/ Sustainability Matrix |

|

10.8. Manufacturing Network |

|

10.8.1. Locations |

|

10.8.2. Supply Chain and Logistics |

|

10.8.3. Product Flexibility/Customization |

|

10.8.4. Digital Transformation and Connectivity |

|

10.8.5. Environmental and Regulatory Compliance |

|

10.9. Technology Readiness Level Matrix |

|

10.10. Technology Maturity Curve |

|

10.11. Buying Criteria |

|

11. Company Profiles |

|

11.1. Siemens AG |

|

11.1.1. Company Overview |

|

11.1.2. Company Financials |

|

11.1.3. Product/Service Portfolio |

|

11.1.4. Recent Developments |

|

11.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

11.2. ABB Ltd. |

|

11.3. Schneider Electric SE |

|

11.4. General Electric (GE) |

|

11.5. Mitsubishi Electric Corporation |

|

11.6. Eaton Corporation |

|

11.7. Toshiba Corporation |

|

11.8. Hitachi, Ltd. |

|

11.9. Hyundai Electric & Energy Systems Co. |

|

11.10. Bharat Heavy Electricals Limited (BHEL) |

|

11.11. Larsen & Toubro Limited |

|

11.12. Crompton Greaves |

|

11.13. Alstom Grid |

|

11.14. Emerson Electric Co. |

|

11.15. Crompton Greaves Consumer Electricals |

|

12. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Industrial Transmission Substation Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Industrial Transmission Substation Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Industrial Transmission Substation Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA