As per Intent Market Research, the Industrial Starch Market was valued at USD 116.1 Billion in 2024-e and will surpass USD 169.1 Billion by 2030; growing at a CAGR of 6.5% during 2025-2030.

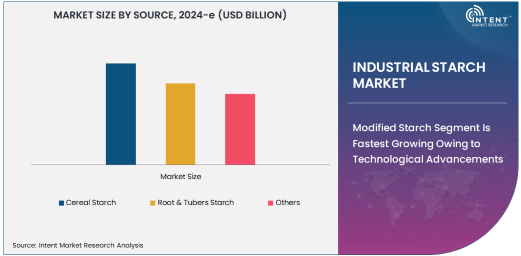

The industrial starch market is a crucial component of the global economy, with starch being derived from various sources such as cereals, root & tubers, and other plants. Cereal starch holds the largest share within this market due to its wide application across industries. Cereal-based starches are favored for their ability to offer cost-effective solutions, excellent consistency, and high performance in a range of products. Cereal starch is particularly essential in food & beverage products, pharmaceuticals, and other industrial uses, making it a key ingredient in diverse manufacturing processes.

The demand for cereal starch continues to rise as consumer preferences evolve towards healthier and more natural ingredients in processed foods. This segment is expected to retain its dominance due to its adaptability in both the food and non-food industries. The use of cereal starch in food products like sauces, soups, and baked goods is particularly strong, contributing to its growth as a significant market player.

Modified Starch Segment Is Fastest Growing Owing to Technological Advancements

The modified starch segment is the fastest growing due to continuous advancements in starch processing technologies. Modified starch is increasingly preferred across industries because of its enhanced functionalities, such as improved texture, stability, and resistance to heat. This form of starch finds substantial use in the food & beverage sector, pharmaceuticals, and other industrial applications. Its ability to cater to the evolving needs of the food industry, such as clean-label products, gluten-free formulations, and increased shelf life, propels the demand for modified starch.

The growing preference for clean-label products, as well as the demand for healthier food alternatives, is further driving the growth of modified starch. As food manufacturers focus on creating innovative food products with more natural and simple ingredients, the modified starch market is set to experience significant growth in the coming years. These innovations in product formulations are crucial in meeting the diverse consumer needs and trends of today’s market.

Food & Beverages Segment Is Largest Due to Rising Demand for Processed Foods

Among the various applications of industrial starch, the food & beverages segment is the largest and most significant in terms of consumption. The growing demand for processed and convenience foods has led to an increased reliance on industrial starches, particularly those derived from cereals and modified starch types. The versatility of starch as a thickener, stabilizer, and gelling agent makes it an indispensable ingredient in food production, especially in soups, sauces, snacks, dairy products, and baked goods.

This segment’s growth is fueled by the ongoing trend toward healthier eating habits and an increased consumer interest in clean-label products. As manufacturers continue to innovate and offer starch-based solutions that align with these demands, the food & beverage segment is poised for sustained dominance in the industrial starch market. Furthermore, the increasing adoption of starch in plant-based food products further expands the scope of its applications.

Powder Form Is Largest Due to Ease of Use and Cost-Effectiveness

In terms of form, the powder form of industrial starch dominates the market due to its cost-effectiveness and ease of use across multiple applications. Powdered starch is widely preferred in food & beverage manufacturing, as it can be easily incorporated into a variety of products. The powdered form also offers significant advantages in terms of storage, transport, and processing, making it ideal for bulk production and industrial-scale applications.

The versatility and adaptability of powdered starch contribute to its widespread usage across multiple industries, including food processing, textiles, and pharmaceuticals. Its ability to be used as a thickening agent, binding agent, and stabilizer in various products further enhances its demand. This segment is expected to maintain its position as the largest form in the industrial starch market as demand for cost-efficient solutions increases.

Asia Pacific Region Is Fastest Growing Due to Expanding Manufacturing Capacities

The Asia Pacific region is experiencing the fastest growth in the industrial starch market, driven by rapid urbanization, an expanding middle class, and increasing manufacturing activities across countries such as China, India, and Southeast Asia. The food & beverage sector in particular is booming due to rising consumer disposable incomes and changing dietary preferences, contributing significantly to the growth of industrial starch demand in the region. Additionally, as major food and beverage companies expand their production facilities in Asia, the region is witnessing a surge in the need for industrial starches.

This region’s competitive advantage lies in its large-scale agricultural output, particularly in terms of starch-producing crops like rice, wheat, and corn, which fuel the industrial starch supply chain. Moreover, government initiatives aimed at promoting sustainable industrial practices and improving food safety are expected to further bolster the market’s growth in Asia Pacific.

Leading Companies and Competitive Landscape

The industrial starch market is characterized by the presence of several global players that dominate key segments, including Cargill, Archer Daniels Midland Company (ADM), Ingredion Incorporated, and Tate & Lyle. These companies are focusing on expanding their product portfolios through innovations in modified starches and enhancing their distribution channels to reach emerging markets. Strategic mergers, acquisitions, and partnerships are common as these companies look to strengthen their foothold in the market.

The competitive landscape is marked by a focus on technological advancements in starch processing and product customization to meet diverse industry demands. As the market continues to evolve, companies are likely to invest heavily in research and development to stay ahead of market trends, particularly in the areas of sustainability and clean-label food products.

Recent Developments:

- Cargill, Inc. launched a new line of plant-based starch solutions for the food industry.

- Ingredion announced the acquisition of a European starch manufacturing facility to expand its production capacity.

- Roquette Frères S.A. received regulatory approval for its new bio-based starch product for pharmaceutical applications.

- Tate & Lyle PLC entered into a strategic partnership with a leading textile company to develop starch-based solutions for the textile industry.

- Archer Daniels Midland Company completed the expansion of its starch plant in North America to meet growing demand.

List of Leading Companies:

- Cargill, Inc.

- Archer Daniels Midland Company

- Ingredion Incorporated

- Tate & Lyle PLC

- Roquette Frères

- Sumitomo Chemical Co., Ltd.

- China National Chemical Corporation

- Bunge Limited

- AGRANA Group

- Grain Processing Corporation

- The Tereos Group

- DuPont de Nemours, Inc.

- Global Bio-chem Technology Group Company Limited

- Maize Products

- LG Chem

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 116.1 Billion |

|

Forecasted Value (2030) |

USD 169.1 Billion |

|

CAGR (2025 – 2030) |

6.5% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Industrial Starch Market By Source (Corn Starch, Wheat Starch, Potato Starch, Cassava Starch, Tapioca Starch), By Type (Native Starch, Modified Starch, Derivatives Starch) and By End-Use Industry (Food & Beverages, Paper & Pulp, Pharmaceuticals & Healthcare, Textile & Apparel, Construction, Chemical Processing, Adhesives & Sealants, Animal Feed, Biofuels) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Cargill, Inc., Archer Daniels Midland Company, Ingredion Incorporated, Tate & Lyle PLC, Roquette Frères, Sumitomo Chemical Co., Ltd., China National Chemical Corporation, Bunge Limited, AGRANA Group, Grain Processing Corporation, The Tereos Group, DuPont de Nemours, Inc., Global Bio-chem Technology Group Company Limited, Maize Products, LG Chem |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Industrial Starch Market, by Source (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Cereal Starch |

|

4.2. Root & Tubers Starch |

|

4.3. Others |

|

5. Industrial Starch Market, by Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Modified Starch |

|

5.2. Native Starch |

|

5.3. Others |

|

6. Industrial Starch Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Food & Beverages |

|

6.2. Pharmaceuticals |

|

6.3. Textiles |

|

6.4. Paper |

|

6.5. Others |

|

7. Industrial Starch Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Food & Beverages |

|

7.2. Paper & Pulp |

|

7.3. Textile Industry |

|

7.4. Others |

|

8. Industrial Starch Market, by Form (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Powder |

|

8.2. Liquid |

|

8.3. Gel |

|

8.4. Others |

|

9. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

9.1. Regional Overview |

|

9.2. North America |

|

9.2.1. Regional Trends & Growth Drivers |

|

9.2.2. Barriers & Challenges |

|

9.2.3. Opportunities |

|

9.2.4. Factor Impact Analysis |

|

9.2.5. Technology Trends |

|

9.2.6. North America Industrial Starch Market, by Source |

|

9.2.7. North America Industrial Starch Market, by Type |

|

9.2.8. North America Industrial Starch Market, by Application |

|

9.2.9. North America Industrial Starch Market, by End-User |

|

9.2.10. North America Industrial Starch Market, by Form |

|

9.2.11. By Country |

|

9.2.11.1. US |

|

9.2.11.1.1. US Industrial Starch Market, by Source |

|

9.2.11.1.2. US Industrial Starch Market, by Type |

|

9.2.11.1.3. US Industrial Starch Market, by Application |

|

9.2.11.1.4. US Industrial Starch Market, by End-User |

|

9.2.11.1.5. US Industrial Starch Market, by Form |

|

9.2.11.2. Canada |

|

9.2.11.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

9.3. Europe |

|

9.4. Asia-Pacific |

|

9.5. Latin America |

|

9.6. Middle East & Africa |

|

10. Competitive Landscape |

|

10.1. Overview of the Key Players |

|

10.2. Competitive Ecosystem |

|

10.2.1. Level of Fragmentation |

|

10.2.2. Market Consolidation |

|

10.2.3. Product Innovation |

|

10.3. Company Share Analysis |

|

10.4. Company Benchmarking Matrix |

|

10.4.1. Strategic Overview |

|

10.4.2. Product Innovations |

|

10.5. Start-up Ecosystem |

|

10.6. Strategic Competitive Insights/ Customer Imperatives |

|

10.7. ESG Matrix/ Sustainability Matrix |

|

10.8. Manufacturing Network |

|

10.8.1. Locations |

|

10.8.2. Supply Chain and Logistics |

|

10.8.3. Product Flexibility/Customization |

|

10.8.4. Digital Transformation and Connectivity |

|

10.8.5. Environmental and Regulatory Compliance |

|

10.9. Technology Readiness Level Matrix |

|

10.10. Technology Maturity Curve |

|

10.11. Buying Criteria |

|

11. Company Profiles |

|

11.1. Cargill, Inc. |

|

11.1.1. Company Overview |

|

11.1.2. Company Financials |

|

11.1.3. Product/Service Portfolio |

|

11.1.4. Recent Developments |

|

11.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

11.2. Archer Daniels Midland Company |

|

11.3. Ingredion Incorporated |

|

11.4. Tate & Lyle PLC |

|

11.5. Roquette Frères |

|

11.6. Sumitomo Chemical Co., Ltd. |

|

11.7. China National Chemical Corporation |

|

11.8. Bunge Limited |

|

11.9. AGRANA Group |

|

11.10. Grain Processing Corporation |

|

11.11. The Tereos Group |

|

11.12. DuPont de Nemours, Inc. |

|

11.13. Global Bio-chem Technology Group Company Limited |

|

11.14. Maize Products |

|

11.15. LG Chem |

|

12. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Industrial Starch Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Industrial Starch Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Industrial Starch Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA