As per Intent Market Research, the Industrial Maintenance Coatings Market was valued at USD 12.5 Billion in 2024-e and will surpass USD 18.1 Billion by 2030; growing at a CAGR of 6.4% during 2025-2030.

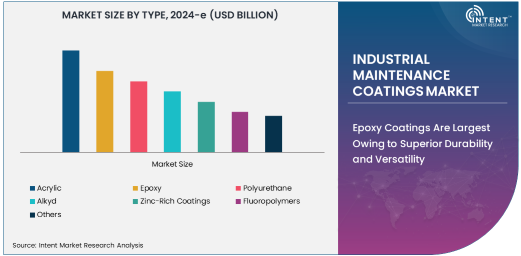

Epoxy Coatings Are Largest Owing to Superior Durability and Versatility

The industrial maintenance coatings market is critical for protecting infrastructure and equipment across a range of industries. Among the various coating types, epoxy coatings hold the largest market share due to their superior durability, chemical resistance, and versatility. Epoxy coatings are widely used in industrial environments where surfaces are exposed to harsh chemicals, abrasion, and moisture. Their ability to form a hard, protective layer makes them ideal for applications in oil & gas, construction, and manufacturing.

The popularity of epoxy coatings is also driven by their excellent adhesion properties and long lifespan, which reduce maintenance costs over time. In addition, advancements in epoxy formulations, such as low-VOC and water-based variants, are further boosting their adoption in environmentally conscious industries. As the demand for robust protective coatings continues to rise across sectors, epoxy coatings remain the preferred choice for industrial applications.

Corrosion Protection Application Is Largest Due to Growing Infrastructure Needs

Corrosion protection is the largest application segment in the industrial maintenance coatings market, driven by the need to safeguard infrastructure and equipment from degradation. Industries such as oil & gas, marine, and construction face significant challenges from corrosion caused by exposure to moisture, chemicals, and harsh environmental conditions. Maintenance coatings designed for corrosion protection provide a critical barrier that extends the lifespan of assets, reducing costly repairs and replacements.

With increasing investments in infrastructure development and the expansion of industrial facilities globally, the demand for corrosion protection coatings has surged. This trend is particularly strong in regions with extreme climates or high levels of industrial pollution, where the risk of corrosion is elevated. As industries continue to prioritize asset protection and long-term cost savings, corrosion protection remains the dominant application in the industrial maintenance coatings market.

Oil & Gas End-User Is Largest Owing to Harsh Operating Conditions

The oil & gas sector is the largest end-user of industrial maintenance coatings, driven by the industry's need to protect infrastructure, pipelines, and equipment from extreme operating conditions. Oil rigs, refineries, and transportation systems are constantly exposed to harsh environmental factors such as saltwater, chemicals, and high temperatures, which can lead to corrosion, abrasion, and structural damage. Industrial coatings provide a durable barrier that ensures operational efficiency and safety in this critical sector.

The growing investments in upstream and downstream oil & gas activities, particularly in emerging markets, further fuel the demand for maintenance coatings. With a strong focus on minimizing downtime and maintenance costs, oil & gas operators are increasingly adopting advanced coating technologies to enhance the durability and performance of their assets. This sustained demand secures the oil & gas sector’s position as the leading end-user in the industrial maintenance coatings market.

Water-Based Coatings Are Fastest Growing Owing to Environmental Compliance

Water-based coatings are the fastest-growing technology segment in the industrial maintenance coatings market, driven by stringent environmental regulations and the rising demand for eco-friendly solutions. These coatings are characterized by low VOC emissions, making them a preferred choice in industries that prioritize sustainability and worker safety. Advancements in water-based formulations have also improved their performance, enabling them to provide excellent durability, corrosion resistance, and aesthetic appeal.

The adoption of water-based coatings is particularly prominent in regions with strict environmental standards, such as Europe and North America. Additionally, industries like automotive, aerospace, and construction are increasingly turning to water-based coatings to align with global sustainability initiatives. As industries continue to transition toward greener alternatives, water-based coatings are expected to witness robust growth in the coming years.

Asia Pacific Region Is Largest Due to Expanding Industrial and Construction Activities

The Asia Pacific region holds the largest share of the industrial maintenance coatings market, driven by rapid industrialization, urbanization, and infrastructure development in countries like China, India, and Southeast Asia. The region’s booming construction sector and expanding oil & gas and automotive industries are major contributors to the demand for maintenance coatings. Additionally, the harsh climatic conditions in parts of Asia Pacific, such as high humidity and extreme temperatures, necessitate the use of protective coatings to prevent corrosion and abrasion.

Government investments in large-scale infrastructure projects and industrial facilities further amplify the demand for maintenance coatings in the region. With a strong focus on economic development and industrial growth, Asia Pacific is expected to maintain its dominance in the industrial maintenance coatings market over the forecast period.

Leading Companies and Competitive Landscape

The industrial maintenance coatings market is highly competitive, with prominent players such as PPG Industries, Akzo Nobel N.V., Sherwin-Williams, Jotun, and Axalta Coating Systems leading the market. These companies focus on product innovation, offering advanced coating solutions that cater to diverse industrial needs, including corrosion resistance, chemical protection, and environmental compliance.

The competitive landscape is also marked by collaborations, mergers, and acquisitions aimed at expanding market reach and enhancing product portfolios. Additionally, leading players are investing heavily in R&D to develop sustainable and high-performance coatings, such as water-based and low-VOC formulations, to meet the evolving demands of industries. With a growing emphasis on eco-friendly solutions and technological advancements, the competition in the industrial maintenance coatings market is expected to remain intense.

Recent Developments:

- AkzoNobel N.V. launched a new range of eco-friendly industrial maintenance coatings aimed at improving corrosion protection and reducing environmental impact.

- PPG Industries, Inc. unveiled a cutting-edge corrosion-resistant coating designed for use in the aerospace and defense sectors to extend the lifespan of aircraft and equipment.

- Sherwin-Williams Company expanded its product portfolio by introducing high-performance coatings for the marine industry, focusing on anti-corrosion and weathering resistance.

- BASF SE announced a strategic partnership with a leading oil & gas company to develop specialized coatings for offshore platforms and subsea equipment.

- RPM International Inc. introduced an advanced, high-durability industrial maintenance coating designed for power plants, improving asset protection against extreme operating conditions.

List of Leading Companies:

- Microsoft Corporation

- Meta Platforms, Inc.

- NVIDIA Corporation

- Unity Technologies

- Epic Games, Inc.

- Siemens AG

- PTC Inc.

- Honeywell International Inc.

- Bosch Group

- IBM Corporation

- Schneider Electric

- Dassault Systèmes

- Autodesk, Inc.

- Trimble Inc.

- Ericsson

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 12.5 Billion |

|

Forecasted Value (2030) |

USD 18.1 Billion |

|

CAGR (2025 – 2030) |

6.4% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Industrial Maintenance Coatings Market By Product Type (Epoxy Coatings, Polyurethane Coatings, Acrylic Coatings, Alkyd Coatings, Zinc Coatings) and By End-Use Industry (Automotive, Aerospace & Defense, Oil & Gas, Marine, Construction, Power Generation, Chemical & Petrochemical, Food & Beverage, Paper & Pulp) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Microsoft Corporation, Meta Platforms, Inc., NVIDIA Corporation, Unity Technologies, Epic Games, Inc., Siemens AG, PTC Inc., Honeywell International Inc., Bosch Group, IBM Corporation, Schneider Electric, Dassault Systèmes, Autodesk, Inc., Trimble Inc., Ericsson |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Industrial Maintenance Coatings Market, by Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Acrylic |

|

4.2. Epoxy |

|

4.3. Polyurethane |

|

4.4. Alkyd |

|

4.5. Zinc-Rich Coatings |

|

4.6. Fluoropolymers |

|

4.7. Others |

|

5. Industrial Maintenance Coatings Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Corrosion Protection |

|

5.2. Abrasion Resistance |

|

5.3. Chemical Resistance |

|

5.4. Thermal Resistance |

|

5.5. Decorative Purposes |

|

5.6. Others |

|

6. Industrial Maintenance Coatings Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Oil & Gas |

|

6.2. Energy & Power |

|

6.3. Marine |

|

6.4. Aerospace |

|

6.5. Automotive |

|

6.6. Construction |

|

6.7. Others |

|

7. Industrial Maintenance Coatings Market, by Technology (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Solvent-Based Coatings |

|

7.2. Water-Based Coatings |

|

7.3. Powder Coatings |

|

7.4. UV-Cured Coatings |

|

7.5. Others |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Industrial Maintenance Coatings Market, by Type |

|

8.2.7. North America Industrial Maintenance Coatings Market, by Application |

|

8.2.8. North America Industrial Maintenance Coatings Market, by End-User |

|

8.2.9. North America Industrial Maintenance Coatings Market, by Technology |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Industrial Maintenance Coatings Market, by Type |

|

8.2.10.1.2. US Industrial Maintenance Coatings Market, by Application |

|

8.2.10.1.3. US Industrial Maintenance Coatings Market, by End-User |

|

8.2.10.1.4. US Industrial Maintenance Coatings Market, by Technology |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Akzo Nobel N.V. |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. PPG Industries, Inc. |

|

10.3. Sherwin-Williams Company |

|

10.4. RPM International Inc. |

|

10.5. Axalta Coating Systems |

|

10.6. Nippon Paint Holdings Co., Ltd. |

|

10.7. BASF SE |

|

10.8. Jotun Group |

|

10.9. Hempel A/S |

|

10.10. Kansai Paint Co., Ltd. |

|

10.11. Tikkurila Oyj |

|

10.12. DuluxGroup Limited |

|

10.13. Berger Paints India Limited |

|

10.14. Teknos Group |

|

10.15. Benjamin Moore & Co. |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Industrial Maintenance Coatings Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Industrial Maintenance Coatings Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Industrial Maintenance Coatings Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA