As per Intent Market Research, the In-Vitro Toxicology Testing Market was valued at USD 3.9 Billion in 2024-e and will surpass USD 7.2 Billion by 2030; growing at a CAGR of 10.9% during 2025 - 2030.

The in-vitro toxicology testing market has gained significant momentum over the past few years, driven by the increasing need for safer, more efficient alternatives to traditional animal testing. In-vitro toxicology testing refers to the use of laboratory-based methods, such as cell-based assays, biochemical assays, and organ-on-a-chip systems, to assess the toxic effects of substances. These tests are widely employed across multiple industries, including pharmaceuticals, biotechnology, chemicals, and cosmetics, to evaluate the safety profile of new products and compounds. The shift toward in-vitro testing has been spurred by stricter regulatory standards and growing ethical concerns about animal testing, along with the demand for faster and more cost-effective solutions in drug development and product testing.

As the market grows, several innovative technologies are revolutionizing the toxicology testing landscape. In-vitro toxicology testing not only provides quicker results but also offers more precise data on the safety of substances, which helps to accelerate the drug development process. The adoption of advanced cell-based assays, organ-on-a-chip technology, and other 3D culture systems have significantly enhanced testing capabilities, further boosting market growth. Additionally, the growing trend of personalized medicine and precision therapeutics has increased the need for tailored toxicology testing, enabling the market to expand across multiple applications and industries.

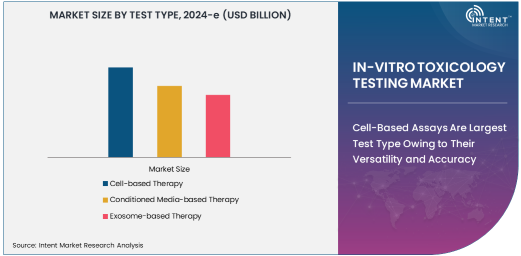

Cell-Based Assays Are Largest Test Type Owing to Their Versatility and Accuracy

Cell-based assays dominate the in-vitro toxicology testing market, making them the largest test type segment. These assays are widely used due to their high accuracy, ability to replicate the biological responses of human tissues, and their ability to screen a wide variety of substances, including pharmaceuticals, chemicals, and cosmetics. In these tests, cells are exposed to the substance of interest, and various biological responses are measured, such as cell viability, metabolic activity, and gene expression. The ability to use human cells in these assays allows for more relevant results compared to traditional animal testing methods, providing crucial data for drug safety assessments.

Cell-based assays offer unparalleled versatility and are applicable in diverse industries, making them the go-to method for assessing the potential toxicity of compounds at an early stage in development. Furthermore, advancements in high-throughput screening technologies have enhanced the ability to conduct large-scale cell-based assays, increasing their demand among pharmaceutical companies and contract research organizations (CROs). As the demand for accurate, human-relevant data grows, cell-based assays will continue to dominate the in-vitro toxicology testing market, driving their widespread adoption in drug development and regulatory testing.

Organ-on-a-Chip Technology Is Fastest Growing Test Type Due to Its Advanced Capabilities

Organ-on-a-chip technology is the fastest-growing segment within the in-vitro toxicology testing market, owing to its advanced capabilities in mimicking the complex biology of human organs. This innovative technology involves the use of microfluidic devices that replicate the physiological environment of human organs, allowing researchers to study the effects of substances on tissue-specific functions in real time. Organ-on-a-chip systems can simulate the behavior of multiple organs simultaneously, offering a more comprehensive view of a compound's systemic effects compared to traditional testing methods.

The growing adoption of organ-on-a-chip technology is driven by its ability to provide more accurate, human-relevant data, which is critical in drug discovery and development. This technology reduces the reliance on animal testing and enables researchers to test the safety and efficacy of new drugs and chemicals in a highly controlled, human-like environment. As regulatory agencies increasingly emphasize the need for non-animal testing methods, the market for organ-on-a-chip technology is expected to expand rapidly, with continued advancements leading to more robust and predictive testing models.

Contract Research Organizations (CROs) Are Largest End-Use Industry Due to High Demand for Outsourced Services

Contract Research Organizations (CROs) represent the largest end-use industry in the in-vitro toxicology testing market, owing to the increasing outsourcing of toxicology testing services by pharmaceutical, biotechnology, and chemical companies. CROs specialize in providing outsourced research and testing services, including toxicology testing, to support the development and regulatory approval of new compounds. As the complexity of drug development processes increases, many pharmaceutical and biotech companies prefer to work with CROs to access specialized expertise and advanced testing technologies without investing heavily in their own in-house testing facilities.

CROs play a pivotal role in the pharmaceutical and biotechnology industries, offering services that accelerate drug development timelines and ensure compliance with regulatory requirements. By outsourcing in-vitro toxicology testing to CROs, companies can benefit from cost-effective, high-quality services, thereby reducing time-to-market for new drugs and chemicals. The growing demand for regulatory-compliant testing, along with the need for specialized toxicology services, will continue to drive the dominance of CROs in the in-vitro toxicology testing market, positioning them as key players in the industry’s growth.

North America Is Largest Region Owing to Strong Regulatory Framework and R&D Investment

North America is the largest region in the in-vitro toxicology testing market, driven by a robust regulatory framework and significant investments in research and development. The United States, in particular, is home to many leading pharmaceutical companies, research institutions, and CROs, making it a hub for in-vitro toxicology testing. Regulatory agencies like the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) have established stringent safety standards, pushing for the adoption of in-vitro testing methods to replace animal testing. This has resulted in strong demand for innovative toxicology testing solutions in the region.

The region also benefits from advanced healthcare infrastructure, high levels of research funding, and a growing focus on reducing the costs and time associated with drug development. North America’s emphasis on scientific innovation, coupled with increasing pressure for ethical testing practices, positions it as the dominant player in the global in-vitro toxicology testing market. Furthermore, the presence of key market players in the region continues to foster growth, making North America a critical market for in-vitro toxicology testing technologies.

Leading Companies and Competitive Landscape

The in-vitro toxicology testing market is highly competitive, with several key players at the forefront of technological advancements and market expansion. Leading companies in the market include Thermo Fisher Scientific, Lonza Group, Charles River Laboratories, Agilent Technologies, and Corning Incorporated. These companies are focused on offering innovative, cutting-edge solutions in in-vitro toxicology testing, including advanced cell-based assays, organ-on-a-chip systems, and biochemical assays.

The competitive landscape is characterized by ongoing research and development efforts to introduce more sophisticated and human-relevant testing models, as well as strategic partnerships and collaborations between industry players and academic institutions. Companies are also investing in high-throughput testing technologies, which enable large-scale testing and faster time-to-market for new drugs. As the demand for non-animal testing alternatives continues to grow, these leading players are well-positioned to dominate the in-vitro toxicology testing market by providing cost-effective, high-quality solutions to meet the evolving needs of the pharmaceutical, biotechnology, and chemical industries.

Recent Developments:

- Charles River Laboratories announced the expansion of its in-vitro toxicology testing services with a new state-of-the-art facility focused on advanced cell-based assays.

- Eurofins Scientific introduced a new range of organ-on-a-chip systems for toxicology testing, enhancing predictive capabilities for pharmaceutical safety testing.

- Covance expanded its portfolio by acquiring a leading provider of in-vitro toxicology testing technologies, further strengthening its position in the pharmaceutical industry.

- Lonza Group partnered with a biotech firm to develop next-generation in-vitro toxicology testing solutions for personalized medicine applications.

- Syngenta launched a new initiative to provide advanced in-vitro testing for chemical toxicity, supporting regulatory compliance for agricultural chemicals.

List of Leading Companies:

- Charles River Laboratories

- Eurofins Scientific

- Covance (Labcorp Drug Development)

- Syngenta International AG

- BASF SE

- Toxys B.V.

- Lonza Group

- In Vitro ADMET Laboratories

- Pharmacology & Toxicology Services, Inc. (PTS)

- Harlan Laboratories

- Covance Laboratories

- Wuxi AppTec

- Integra LifeSciences

- Merck Group

- Labcorp Drug Development

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 3.9 Billion |

|

Forecasted Value (2030) |

USD 7.2 Billion |

|

CAGR (2025 – 2030) |

10.9% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Global In-Vitro Toxicology Testing Market by Test Type (Cell-based Assays, Biochemical Assays, Organ-on-a-chip), by Application (Pharmaceutical and Biotechnology, Chemical Industry), by End-Use Industry (Contract Research Organizations (CROs), Government Research Institutes), and by Region |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Charles River Laboratories, Eurofins Scientific, Covance (Labcorp Drug Development), Syngenta International AG, BASF SE, Toxys B.V., In Vitro ADMET Laboratories, Pharmacology & Toxicology Services, Inc. (PTS), Harlan Laboratories, Covance Laboratories, Wuxi AppTec, Integra LifeSciences, Labcorp Drug Development |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. In-Vitro Toxicology Testing Market, by Test Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Cell-based Assays |

|

4.2. Biochemical Assays |

|

4.3. Organ-on-a-chip |

|

5. In-Vitro Toxicology Testing Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Pharmaceutical and Biotechnology |

|

5.2. Chemical Industry |

|

5.3. Others |

|

6. In-Vitro Toxicology Testing Market, by End-Use Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Contract Research Organizations (CROs) |

|

6.2. Government Research Institutes |

|

6.3. Others |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America In-Vitro Toxicology Testing Market, by Test Type |

|

7.2.7. North America In-Vitro Toxicology Testing Market, by Application |

|

7.2.8. North America In-Vitro Toxicology Testing Market, by End-Use Industry |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US In-Vitro Toxicology Testing Market, by Test Type |

|

7.2.9.1.2. US In-Vitro Toxicology Testing Market, by Application |

|

7.2.9.1.3. US In-Vitro Toxicology Testing Market, by End-Use Industry |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Charles River Laboratories |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Eurofins Scientific |

|

9.3. Covance (Labcorp Drug Development) |

|

9.4. Syngenta International AG |

|

9.5. BASF SE |

|

9.6. Toxys B.V. |

|

9.7. Lonza Group |

|

9.8. In Vitro ADMET Laboratories |

|

9.9. Pharmacology & Toxicology Services, Inc. (PTS) |

|

9.10. Harlan Laboratories |

|

9.11. Covance Laboratories |

|

9.12. Wuxi AppTec |

|

9.13. Integra LifeSciences |

|

9.14. Merck Group |

|

9.15. Labcorp Drug Development |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the In-Vitro Toxicology Testing Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the In-Vitro Toxicology Testing Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the In-Vitro Toxicology Testing Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA