As per Intent Market Research, the Hyperscale Data Center Market was valued at USD 41.4 Billion in 2024-e and will surpass USD 247.6 Billion by 2030; growing at a CAGR of 34.7% during 2025-2030.

The hyperscale data center market is growing rapidly, driven by the increasing demand for large-scale, efficient, and flexible computing infrastructure. Hyperscale data centers are designed to accommodate vast amounts of data and enable high-performance computing for a variety of industries, including IT and telecom, BFSI, healthcare, retail, and more. These data centers are often used by large enterprises and cloud service providers to support critical business applications, data storage, and complex analytics, providing the scalability and reliability needed to handle vast amounts of digital information.

The increasing adoption of cloud computing, big data analytics, and the growing need for disaster recovery and data backup solutions are some of the major factors propelling the growth of hyperscale data centers. As businesses increasingly rely on digital operations and data-driven decision-making, the demand for data center services is surging. Hyperscale data centers enable organizations to scale their infrastructure efficiently, lower costs, and optimize performance, positioning them as a critical component of the digital transformation underway across industries.

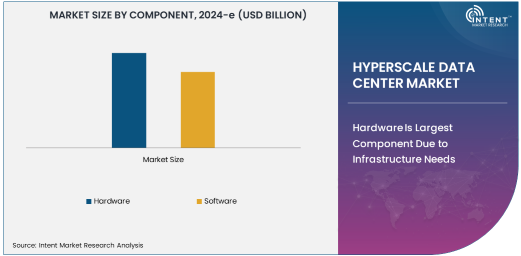

Hardware Is Largest Component Due to Infrastructure Needs

Hardware is the largest component in the hyperscale data center market, primarily due to the need for powerful physical infrastructure to support computing and storage functions. Hyperscale data centers require high-performance servers, storage devices, networking equipment, and cooling systems, all of which are critical to maintaining efficient operations. The demand for more efficient, cost-effective, and powerful hardware components is continually increasing as businesses scale up their digital operations and storage needs.

As technologies evolve, the hardware required for hyperscale data centers is becoming increasingly sophisticated. Innovations in server designs, storage systems, and network infrastructure are helping organizations reduce operational costs and increase performance. The hardware segment is expected to maintain its dominance in the market as data storage needs continue to grow and computing power requirements become more demanding.

Cloud Solutions Are Largest Solution Due to Rising Adoption of Cloud Services

Cloud solutions are the largest solution type in the hyperscale data center market, driven by the rapid growth of cloud computing services. As businesses across industries adopt cloud-based applications, platforms, and services, the demand for scalable data center infrastructure is increasing. Cloud solutions provide the flexibility, scalability, and cost-effectiveness that organizations require to manage their workloads, process data, and run business applications with high performance and minimal downtime.

The cloud offers numerous advantages, including reduced capital expenditures, ease of scalability, and access to powerful computing resources on-demand. Hyperscale data centers play a vital role in supporting cloud service providers by housing massive amounts of data and ensuring that cloud services are delivered efficiently to end-users. As cloud adoption continues to expand globally, cloud solutions remain the largest and most critical component of the hyperscale data center market.

IT & Telecom Is Fastest Growing End-User Industry Due to Data Demand and Network Expansion

The IT and telecom industry is the fastest-growing end-user in the hyperscale data center market, driven by the increasing demand for data storage, network expansion, and high-performance computing capabilities. With the rise of technologies such as 5G, the Internet of Things (IoT), and big data analytics, telecom operators and IT companies need robust data center infrastructure to support the growing volume of data traffic and the need for low-latency services. Hyperscale data centers offer these companies the ability to efficiently manage vast amounts of data and ensure high availability for mission-critical applications.

As digital transformation accelerates across industries, telecom companies are investing heavily in data center infrastructure to support the deployment of next-generation networks, including 5G and edge computing solutions. The increasing reliance on cloud-based platforms and digital services further drives the demand for hyperscale data centers in the IT and telecom sector, positioning it as the fastest-growing end-user industry.

Data Storage Is Largest Application Due to Increasing Volume of Digital Data

Data storage is the largest application in the hyperscale data center market, driven by the exponential growth in digital data generated by businesses, consumers, and connected devices. Organizations across industries are creating and storing vast amounts of data, from transactional information to customer records and multimedia files, all of which require efficient and scalable storage solutions. Hyperscale data centers provide the necessary infrastructure to store, manage, and secure this growing volume of data, offering high-capacity storage systems that ensure data is always accessible.

As more organizations embrace data-driven decision-making, the need for reliable, scalable data storage solutions becomes increasingly important. With the rise of cloud computing and big data analytics, the demand for data storage continues to grow, making it the dominant application in the hyperscale data center market. These data centers are equipped with advanced storage technologies, such as solid-state drives and high-density storage systems, to meet the needs of modern enterprises.

Cloud Deployment Type Is Largest Due to Scalability and Cost Efficiency

Cloud deployment is the largest deployment type in the hyperscale data center market, driven by the cost efficiency, scalability, and flexibility offered by cloud-based infrastructure. Cloud deployment allows organizations to access computing resources on-demand, scale infrastructure as needed, and minimize upfront capital expenditures. It enables companies to run business applications, store data, and perform analytics without having to invest in large on-premises infrastructure.

With the growing trend of digital transformation and the increasing adoption of cloud computing, cloud deployment continues to dominate the hyperscale data center market. Companies are increasingly shifting from traditional on-premises infrastructure to cloud-based solutions to take advantage of the scalability and cost savings offered by hyperscale data centers. As more organizations move their workloads to the cloud, the demand for cloud-based hyperscale data centers will continue to increase.

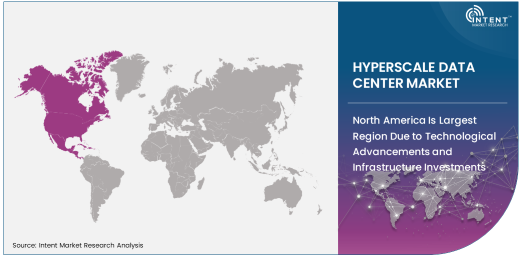

North America Is Largest Region Due to Technological Advancements and Infrastructure Investments

North America is the largest region in the hyperscale data center market, driven by technological advancements, a strong IT infrastructure, and significant investments in data center development. The United States, in particular, is home to many of the world’s leading cloud service providers, including Amazon Web Services (AWS), Microsoft Azure, and Google Cloud, all of which rely on hyperscale data centers to deliver their services. The region’s advanced technological ecosystem, coupled with a highly developed digital economy, positions North America as the dominant player in the market.

In addition to the presence of major cloud providers, North America has a well-established network of telecom companies, financial institutions, and government agencies, all of which contribute to the demand for hyperscale data centers. The region’s investments in cutting-edge technologies such as AI, machine learning, and big data analytics also drive the need for scalable data center infrastructure. As a result, North America remains the largest and most advanced region in the hyperscale data center market.

Competitive Landscape

The hyperscale data center market is highly competitive, with a large number of players offering various products and services to meet the growing demand for digital infrastructure. Key market participants include major cloud service providers, data center operators, and technology companies that specialize in hardware and software solutions for data centers. These companies are focusing on expanding their infrastructure to meet the needs of industries such as IT, telecom, BFSI, and healthcare, as well as offering innovative solutions that improve performance, reduce energy consumption, and enhance security.

As the market continues to evolve, companies are increasingly investing in innovations such as edge computing, energy-efficient technologies, and software-defined data centers to stay ahead of the competition. Strategic partnerships, acquisitions, and technology advancements will continue to shape the competitive landscape of the hyperscale data center market, with companies striving to meet the growing demand for scalable and cost-effective data center solutions.

Recent Developments:

- In December 2024, Amazon Web Services (AWS) announced the expansion of its hyperscale data centers in Asia Pacific, enhancing cloud service availability across the region.

- In November 2024, Google Cloud opened a new hyperscale data center in Europe to meet the growing demand for AI and machine learning capabilities.

- In October 2024, Microsoft Corporation revealed plans to build multiple new hyperscale data centers across North America to support the increasing demand for Azure services.

- In September 2024, Digital Realty Trust acquired a significant land parcel in North America to build a new hyperscale data center facility.

- In August 2024, Facebook (Meta Platforms) launched a sustainability-focused hyperscale data center in Oregon, using renewable energy to power its operations.

List of Leading Companies:

- Amazon Web Services (AWS)

- Google Cloud

- Microsoft Corporation

- Equinix, Inc.

- Digital Realty Trust, Inc.

- Alibaba Cloud

- Apple Inc.

- Facebook (Meta Platforms Inc.)

- Huawei Technologies

- IBM Corporation

- NTT Communications

- Oracle Corporation

- Rackspace Technology

- Intel Corporation

- Cisco Systems, Inc

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 41.4 Billion |

|

Forecasted Value (2030) |

USD 247.6 Billion |

|

CAGR (2025 – 2030) |

34.7% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Hyperscale Data Center Market by Component (Hardware, Software), Solution (Cloud Solutions, Data Center Infrastructure Management (DCIM), Virtualization Solutions), End-User Industry (IT & Telecom, BFSI, Healthcare & Life Sciences, Retail, Government & Defense, Energy & Utilities), Deployment Type (On-Premises, Cloud), Application (Data Storage, Big Data Analytics, Disaster Recovery, Backup & Archiving) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Amazon Web Services (AWS), Google Cloud, Microsoft Corporation, Equinix, Inc., Digital Realty Trust, Inc., Alibaba Cloud, Apple Inc., Facebook (Meta Platforms Inc.), Huawei Technologies, IBM Corporation, NTT Communications, Oracle Corporation, Rackspace Technology, Intel Corporation, Cisco Systems, Inc |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Hyperscale Data Center Market, by Component (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Hardware |

|

4.2. Software |

|

5. Hyperscale Data Center Market, by Solution (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Cloud Solutions |

|

5.2. Data Center Infrastructure Management (DCIM) |

|

5.3. Virtualization Solutions |

|

6. Hyperscale Data Center Market, by End-User Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. IT & Telecom |

|

6.2. BFSI (Banking, Financial Services & Insurance) |

|

6.3. Healthcare & Life Sciences |

|

6.4. Retail |

|

6.5. Government & Defense |

|

6.6. Energy & Utilities |

|

7. Hyperscale Data Center Market, by Deployment Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. On-Premises |

|

7.2. Cloud |

|

8. Hyperscale Data Center Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Data Storage |

|

8.2. Big Data Analytics |

|

8.3. Disaster Recovery |

|

8.4. Backup & Archiving |

|

9. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

9.1. Regional Overview |

|

9.2. North America |

|

9.2.1. Regional Trends & Growth Drivers |

|

9.2.2. Barriers & Challenges |

|

9.2.3. Opportunities |

|

9.2.4. Factor Impact Analysis |

|

9.2.5. Technology Trends |

|

9.2.6. North America Hyperscale Data Center Market, by Component |

|

9.2.7. North America Hyperscale Data Center Market, by Solution |

|

9.2.8. North America Hyperscale Data Center Market, by End-User Industry |

|

9.2.9. North America Hyperscale Data Center Market, by Deployment Type |

|

9.2.10. North America Hyperscale Data Center Market, by Application |

|

9.2.11. By Country |

|

9.2.11.1. US |

|

9.2.11.1.1. US Hyperscale Data Center Market, by Component |

|

9.2.11.1.2. US Hyperscale Data Center Market, by Solution |

|

9.2.11.1.3. US Hyperscale Data Center Market, by End-User Industry |

|

9.2.11.1.4. US Hyperscale Data Center Market, by Deployment Type |

|

9.2.11.1.5. US Hyperscale Data Center Market, by Application |

|

9.2.11.2. Canada |

|

9.2.11.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

9.3. Europe |

|

9.4. Asia-Pacific |

|

9.5. Latin America |

|

9.6. Middle East & Africa |

|

10. Competitive Landscape |

|

10.1. Overview of the Key Players |

|

10.2. Competitive Ecosystem |

|

10.2.1. Level of Fragmentation |

|

10.2.2. Market Consolidation |

|

10.2.3. Product Innovation |

|

10.3. Company Share Analysis |

|

10.4. Company Benchmarking Matrix |

|

10.4.1. Strategic Overview |

|

10.4.2. Product Innovations |

|

10.5. Start-up Ecosystem |

|

10.6. Strategic Competitive Insights/ Customer Imperatives |

|

10.7. ESG Matrix/ Sustainability Matrix |

|

10.8. Manufacturing Network |

|

10.8.1. Locations |

|

10.8.2. Supply Chain and Logistics |

|

10.8.3. Product Flexibility/Customization |

|

10.8.4. Digital Transformation and Connectivity |

|

10.8.5. Environmental and Regulatory Compliance |

|

10.9. Technology Readiness Level Matrix |

|

10.10. Technology Maturity Curve |

|

10.11. Buying Criteria |

|

11. Company Profiles |

|

11.1. Amazon Web Services (AWS) |

|

11.1.1. Company Overview |

|

11.1.2. Company Financials |

|

11.1.3. Product/Service Portfolio |

|

11.1.4. Recent Developments |

|

11.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

11.2. Google Cloud |

|

11.3. Microsoft Corporation |

|

11.4. Equinix, Inc. |

|

11.5. Digital Realty Trust, Inc. |

|

11.6. Alibaba Cloud |

|

11.7. Apple Inc. |

|

11.8. Facebook (Meta Platforms Inc.) |

|

11.9. Huawei Technologies |

|

11.10. IBM Corporation |

|

11.11. NTT Communications |

|

11.12. Oracle Corporation |

|

11.13. Rackspace Technology |

|

11.14. Intel Corporation |

|

11.15. Cisco Systems, Inc |

|

12. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Hyperscale Data Center Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Hyperscale Data Center Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Hyperscale Data Center Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA