As per Intent Market Research, the Homeopathic Products Market was valued at USD 5.7 Billion in 2024-e and will surpass USD 12.8 Billion by 2030; growing at a CAGR of 12.1% during 2025-2030.

The global homeopathic products market is witnessing significant growth driven by increasing consumer inclination toward natural and alternative therapies. Homeopathy, with its holistic approach to health, has gained popularity across diverse demographics, owing to its perceived safety and minimal side effects. The market is also buoyed by the expanding availability of products across various distribution channels and advancements in manufacturing technologies.

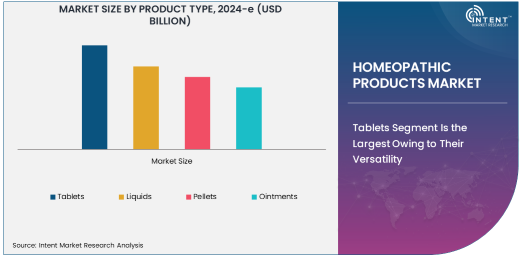

Tablets Segment Is the Largest Owing to Their Versatility

Among product types, tablets stand as the largest segment, accounting for a substantial share of the market. Tablets are preferred by consumers for their convenience, precise dosing, and longer shelf life compared to other forms like liquids or ointments. Their compact packaging and ease of use further enhance their appeal, especially for working individuals and travelers.

The growing demand for immune-boosting and stress-relief homeopathic tablets has fueled innovation in the segment. Market leaders are focusing on the development of sugar-free and vegan-friendly options to cater to diverse consumer preferences. The rising adoption of tablets for chronic conditions such as allergies and arthritis underscores their dominance in the homeopathic products market.

Immunology Application Is the Fastest Growing Owing to Rising Health Awareness

Within the application category, immunology is the fastest-growing segment. The global pandemic has heightened consumer awareness about immunity-boosting solutions, leading to a surge in demand for homeopathic products targeting immune health. These products are increasingly viewed as preventive measures against common illnesses, complementing conventional medicine.

Key players are actively investing in R&D to create formulations that enhance immunity without causing side effects. Pediatric immune boosters, in particular, are gaining traction among parents looking for natural solutions for their children’s health. As the world continues to prioritize wellness and disease prevention, the immunology application is expected to witness exponential growth.

Online Retailers Are Expanding Rapidly Due to Convenience

The online retailers segment is experiencing remarkable growth, driven by the convenience and accessibility offered by e-commerce platforms. Consumers increasingly prefer online shopping for homeopathic products due to the availability of detailed product information, reviews, and doorstep delivery. The COVID-19 pandemic further accelerated the shift toward digital channels, making online retail a dominant force in the market.

Major brands are capitalizing on this trend by enhancing their digital presence and partnering with e-commerce giants. Exclusive online discounts and subscription models are also driving customer retention. With the increasing penetration of smartphones and internet connectivity, online retail is poised to transform the distribution landscape of homeopathic products.

Pediatrics End-User Segment Leads Due to Growing Parental Preference

The pediatrics segment is a leading category in the end-user market, fueled by growing parental preference for safe and natural remedies for children. Homeopathic products are widely used for pediatric applications such as teething, colic, and minor respiratory issues, as they are perceived to be gentle and free from harmful chemicals.

The rise in demand for homeopathy among parents is supported by the availability of pediatric-specific formulations that are easy to administer, such as flavored tablets and liquids. Companies are actively marketing their products as safe alternatives to traditional medicines, further strengthening the growth of this segment.

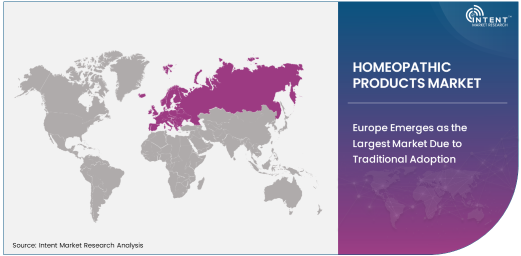

Europe Emerges as the Largest Market Due to Traditional Adoption

Europe dominates the homeopathic products market, driven by its long-standing tradition of homeopathy and widespread acceptance among consumers. Countries like Germany, France, and the United Kingdom are at the forefront, with robust demand for both over-the-counter and prescription-based homeopathic solutions.

Favorable regulatory environments and government support for complementary therapies further bolster Europe’s position in the market. The presence of well-established companies and a high level of awareness about homeopathy contribute to sustained growth in the region. Europe’s strong cultural and medical integration of homeopathy ensures its leadership in the global market.

Competitive Landscape Led by Innovation and Diversification

The competitive landscape of the homeopathic products market is characterized by the presence of several global and regional players. Leading companies such as Boiron, Schwabe Pharmaceuticals, and Heel GmbH are at the forefront, focusing on innovation, product diversification, and expanding their global footprints.

Collaborations, mergers, and acquisitions are common strategies adopted by these companies to strengthen their market positions. Additionally, the increasing focus on digital marketing and e-commerce channels has reshaped competitive dynamics. The market remains competitive yet promising, with ample opportunities for players to differentiate through quality and targeted offerings

Recent Developments:

- Boiron launched a new product line focused on plant-based immunity boosters in late 2024.

- Weleda AG expanded operations in Asia with a new manufacturing plant and retail partnerships.

- Hyland's Inc. introduced pediatric-focused cold and flu remedies in Q4 2024.

- Heel GmbH announced a strategic merger with a European herbal supplement company in January 2025.

- SBL Global received regulatory approval for a new line of dermatology-focused homeopathic solutions in December 2024

List of Leading Companies:

- Boiron

- Schwabe Group

- Nelsons

- Ainsworths

- Biologische Heilmittel Heel GmbH

- Hahnemann Laboratories, Inc.

- GMP Laboratories of America, Inc.

- SBL Global

- Hyland's, Inc.

- Mediral International Inc.

- Standard Homeopathic Company

- Weleda AG

- Fourrts

- Dr. Reckeweg & Co. GmbH

- Allen Healthcare Co

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 5.7 Billion |

|

Forecasted Value (2030) |

USD 12.8 Billion |

|

CAGR (2025 – 2030) |

12.1% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Homeopathic Products Market By Product Type (Tablets, Liquids, Pellets, Ointments), By Application (Respiratory, Neurology, Immunology, Dermatology), By Distribution Channel (Online Retailers, Pharmacies & Drugstores, Supermarkets/Hypermarkets, Specialty Stores), By End-User (Adults, Pediatrics, Geriatrics), and By Region; Global Insights & Forecast (2023 – 2030) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Boiron, Schwabe Group, Nelsons, Ainsworths, Biologische Heilmittel Heel GmbH, Hahnemann Laboratories, Inc., GMP Laboratories of America, Inc., SBL Global, Hyland's, Inc., Mediral International Inc., Standard Homeopathic Company, Weleda AG, Fourrts, Dr. Reckeweg & Co. GmbH, Allen Healthcare Co |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Homeopathic Products Market, by Product Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Tablets |

|

4.2. Liquids |

|

4.3. Pellets |

|

4.4. Ointments |

|

5. Homeopathic Products Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Respiratory |

|

5.2. Neurology |

|

5.3. Immunology |

|

5.4. Dermatology |

|

6. Homeopathic Products Market, by Distribution Channel (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Online Retailers |

|

6.2. Pharmacies & Drugstores |

|

6.3. Supermarkets/Hypermarkets |

|

6.4. Specialty Stores |

|

7. Homeopathic Products Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Adults |

|

7.2. Pediatrics |

|

7.3. Geriatrics |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Homeopathic Products Market, by Product Type |

|

8.2.7. North America Homeopathic Products Market, by Application |

|

8.2.8. North America Homeopathic Products Market, by Distribution Channel |

|

8.2.9. North America Homeopathic Products Market, by End-User |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Homeopathic Products Market, by Product Type |

|

8.2.10.1.2. US Homeopathic Products Market, by Application |

|

8.2.10.1.3. US Homeopathic Products Market, by Distribution Channel |

|

8.2.10.1.4. US Homeopathic Products Market, by End-User |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Boiron |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Schwabe Group |

|

10.3. Nelsons |

|

10.4. Ainsworths |

|

10.5. Biologische Heilmittel Heel GmbH |

|

10.6. Hahnemann Laboratories, Inc. |

|

10.7. GMP Laboratories of America, Inc. |

|

10.8. SBL Global |

|

10.9. Hyland's, Inc. |

|

10.10. Mediral International Inc. |

|

10.11. Standard Homeopathic Company |

|

10.12. Weleda AG |

|

10.13. Fourrts |

|

10.14. Dr. Reckeweg & Co. GmbH |

|

10.15. Allen Healthcare Co |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Homeopathic Products Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Homeopathic Products Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Homeopathic Products Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA