As per Intent Market Research, the HLA Typing Transplant Diagnostics Services Market was valued at USD 0.8 billion in 2024-e and will surpass USD 1.6 billion by 2030; growing at a CAGR of 10.2% during 2025 - 2030.

The HLA Typing Transplant Diagnostics Services market plays a pivotal role in ensuring the success of organ and stem cell transplants, enabling the accurate matching of donors and recipients. The growing demand for organ transplantation worldwide is driven by increasing incidences of organ failure due to chronic diseases, aging populations, and advancements in transplant procedures. These services are crucial in reducing transplant rejection and improving patient outcomes. As the demand for organ and stem cell transplants rises, the need for precise HLA typing technology is expanding, making it a critical component in modern transplantation medicine.

In addition, the market is supported by advancements in molecular diagnostic technologies, including PCR-based testing, sequencing, and microarray technologies, which have significantly improved the accuracy and efficiency of HLA typing. The increasing adoption of these technologies by hospitals, diagnostic laboratories, and biopharmaceutical companies is further driving market growth. With rising investments in healthcare infrastructure and the expanding scope of personalized medicine, HLA typing services are expected to continue evolving and become increasingly integral to transplantation medicine.

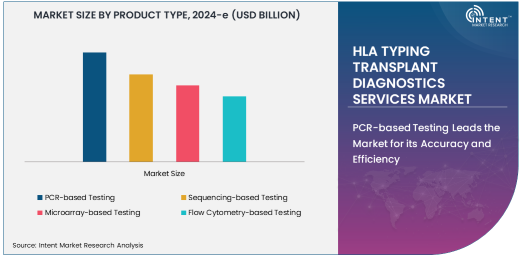

PCR-based Testing Leads the Market for its Accuracy and Efficiency

PCR-based testing is the largest segment in the HLA Typing Transplant Diagnostics Services market, owing to its high accuracy, efficiency, and cost-effectiveness. Polymerase chain reaction (PCR) technology is widely used for amplifying DNA sequences, allowing for the rapid and precise identification of human leukocyte antigens (HLAs) in transplant candidates. This method offers superior sensitivity and specificity, ensuring accurate donor-recipient matching, which is essential for the success of organ and stem cell transplants.

PCR-based testing has become the standard for HLA typing due to its ability to detect even minute quantities of DNA, making it particularly useful for cases where donor DNA samples are limited or degraded. The technology's ability to deliver results quickly is also a significant advantage, especially in time-sensitive transplant procedures. As demand for transplantations increases, PCR-based testing continues to dominate the market due to its unmatched reliability and proven performance.

Sequencing-based Testing Shows Rapid Growth in Precision Medicine

Sequencing-based testing is the fastest-growing segment in the HLA Typing Transplant Diagnostics Services market, driven by its potential to provide more detailed and precise information about the genetic makeup of both donors and recipients. Next-generation sequencing (NGS) allows for comprehensive analysis of HLA genes, offering high-resolution typing and the ability to detect rare alleles that may not be identified through conventional methods.

Sequencing technology's growing popularity is largely attributed to its accuracy and ability to inform more personalized treatment plans. By providing a higher level of detail about HLA compatibility, sequencing-based testing is becoming increasingly important in stem cell transplantation, where perfect HLA matches are crucial for reducing the risk of graft-versus-host disease (GVHD). As healthcare continues to embrace precision medicine, sequencing-based testing is expected to grow rapidly, offering a more robust tool for transplant diagnostics.

Hospitals Dominate as the Leading End-User for Transplant Diagnostics

Hospitals are the largest end-user segment for HLA typing transplant diagnostics services, given their central role in performing organ and stem cell transplants. The need for accurate and timely HLA typing in hospitals is critical to ensuring successful transplant outcomes and minimizing complications such as transplant rejection. Hospitals with specialized transplant departments rely heavily on diagnostic services to perform compatibility testing for both organ and stem cell transplants, making them the primary consumers of HLA typing services.

Hospitals also benefit from the increasing availability of advanced molecular diagnostic technologies, allowing for more efficient and precise testing. As the number of transplant surgeries continues to rise, hospitals remain the largest market segment, with a growing reliance on accurate transplant diagnostics to improve patient care. Additionally, advancements in laboratory capabilities and greater access to sophisticated HLA typing technologies are further driving demand within hospital settings.

Direct Sales Remain the Leading Distribution Channel

Direct sales are the dominant distribution channel for HLA typing transplant diagnostics services, as hospitals and diagnostic laboratories typically purchase testing services directly from manufacturers or service providers. This distribution model ensures better control over the quality of services and enables healthcare providers to customize the diagnostics to meet specific transplant needs. Furthermore, direct sales help build long-term relationships between service providers and end-users, fostering trust and ensuring the availability of high-quality diagnostic services.

While distributors and online retailers contribute to the market, direct sales remain the preferred method for procuring HLA typing services due to the need for precise, reliable, and often time-sensitive results. The ability to provide on-site testing and support further solidifies direct sales as the primary distribution channel, especially in the context of hospital and research institution needs.

North America Leads as the Largest Regional Market for HLA Typing Services

North America is the largest regional market for HLA typing transplant diagnostics services, driven by well-established healthcare infrastructure, advanced medical technologies, and a high demand for organ and stem cell transplants. The United States, in particular, is a key player, with a large number of transplant surgeries performed annually and a robust healthcare system that heavily relies on advanced diagnostic services. The increasing incidence of chronic diseases and the aging population are further fueling the demand for HLA typing services in this region.

Additionally, the presence of leading biotechnology and diagnostic companies in North America contributes to the region's dominance, with continued advancements in HLA typing technologies being developed and commercialized. As the market continues to evolve, North America is expected to maintain its position as the largest market, particularly with the rising trend of precision medicine and personalized transplant care.

Competitive Landscape: Innovation Drives Growth in the HLA Typing Market

The HLA typing transplant diagnostics services market is highly competitive, with key players such as Thermo Fisher Scientific, Illumina, and Bio-Rad Laboratories leading the charge. Companies are focused on innovations such as higher-resolution testing, automation, and integration with healthcare systems to streamline the transplant process and enhance compatibility testing.

As the demand for precision medicine grows, competition among providers is intensifying, with a focus on offering more efficient, accurate, and scalable testing solutions. Companies are also pursuing strategic partnerships with hospitals, biopharmaceutical companies, and research institutions to expand their market presence and enhance their service offerings. With ongoing technological advancements, the competitive landscape will continue to evolve, with an increasing emphasis on innovation and service integration to meet the needs of the transplant diagnostics market.

Recent Developments:

- In December 2024, Thermo Fisher Scientific Inc. launched an advanced NGS platform for high-resolution HLA typing in organ transplantation.

- In November 2024, Bio-Rad Laboratories introduced a new PCR-based diagnostic kit for improved accuracy in HLA typing for stem cell transplants.

- In October 2024, Illumina, Inc. expanded its portfolio with a cutting-edge sequencing solution for HLA testing, aimed at enhancing transplant compatibility.

- In September 2024, F. Hoffmann-La Roche AG announced a partnership with leading transplant centers to develop a next-generation HLA typing assay using real-time PCR.

- In August 2024, QIAGEN N.V. received approval for a new HLA typing microarray-based diagnostic tool to streamline transplant patient testing.

List of Leading Companies:

- Thermo Fisher Scientific Inc.

- Bio-Rad Laboratories, Inc.

- Illumina, Inc.

- F. Hoffmann-La Roche AG

- Abbott Laboratories

- QIAGEN N.V.

- GenDx

- Becton, Dickinson and Company (BD)

- SeraCare Life Sciences, Inc.

- Luminex Corporation

- Medipost Co., Ltd.

- Sequenom (now part of LabCorp)

- Organ Transplant Technologies, Inc.

- HLA Typing Services, Inc.

- Bio-Techne Corporation

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 0.8 Billion |

|

Forecasted Value (2030) |

USD 1.6 Billion |

|

CAGR (2025 – 2030) |

10.2% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

HLA Typing Transplant Diagnostics Services Market by Product Type (PCR-based Testing, Sequencing-based Testing, Microarray-based Testing, Flow Cytometry-based Testing), Technology (PCR Technology, Sequencing Technology, Microarray Technology, Flow Cytometry), End-User (Hospitals, Diagnostic Laboratories, Research Institutions, Biopharmaceutical Companies), Application (Organ Transplantation, Stem Cell Transplantation), Distribution Channel (Direct Sales, Distributors, Online Retailers) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Thermo Fisher Scientific Inc., Bio-Rad Laboratories, Inc., Illumina, Inc., F. Hoffmann-La Roche AG, Abbott Laboratories, QIAGEN N.V., GenDx, Becton, Dickinson and Company (BD), SeraCare Life Sciences, Inc., Luminex Corporation, Medipost Co., Ltd., Sequenom (now part of LabCorp), Organ Transplant Technologies, Inc., HLA Typing Services, Inc., Bio-Techne Corporation |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. HLA Typing Transplant Diagnostics Services Market, by Product Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. PCR-based Testing |

|

4.2. Sequencing-based Testing |

|

4.3. Microarray-based Testing |

|

4.4. Flow Cytometry-based Testing |

|

5. HLA Typing Transplant Diagnostics Services Market, by Technology (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. PCR Technology |

|

5.2. Sequencing Technology |

|

5.3. Microarray Technology |

|

5.4. Flow Cytometry |

|

6. HLA Typing Transplant Diagnostics Services Market, by End-User (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Hospitals |

|

6.2. Diagnostic Laboratories |

|

6.3. Research Institutions |

|

6.4. Biopharmaceutical Companies |

|

7. HLA Typing Transplant Diagnostics Services Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Organ Transplantation |

|

7.2. Stem Cell Transplantation |

|

7.3. Stem Cell Transplantation |

|

8. HLA Typing Transplant Diagnostics Services Market, by Distribution Channel (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Direct Sales |

|

8.2. Distributors |

|

8.3. Online Retailers |

|

9. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

9.1. Regional Overview |

|

9.2. North America |

|

9.2.1. Regional Trends & Growth Drivers |

|

9.2.2. Barriers & Challenges |

|

9.2.3. Opportunities |

|

9.2.4. Factor Impact Analysis |

|

9.2.5. Technology Trends |

|

9.2.6. North America HLA Typing Transplant Diagnostics Services Market, by Product Type |

|

9.2.7. North America HLA Typing Transplant Diagnostics Services Market, by Technology |

|

9.2.8. North America HLA Typing Transplant Diagnostics Services Market, by End-User |

|

9.2.9. North America HLA Typing Transplant Diagnostics Services Market, by Application |

|

9.2.10. North America HLA Typing Transplant Diagnostics Services Market, by Distribution Channel |

|

9.2.11. By Country |

|

9.2.11.1. US |

|

9.2.11.1.1. US HLA Typing Transplant Diagnostics Services Market, by Product Type |

|

9.2.11.1.2. US HLA Typing Transplant Diagnostics Services Market, by Technology |

|

9.2.11.1.3. US HLA Typing Transplant Diagnostics Services Market, by End-User |

|

9.2.11.1.4. US HLA Typing Transplant Diagnostics Services Market, by Application |

|

9.2.11.1.5. US HLA Typing Transplant Diagnostics Services Market, by Distribution Channel |

|

9.2.11.2. Canada |

|

9.2.11.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

9.3. Europe |

|

9.4. Asia-Pacific |

|

9.5. Latin America |

|

9.6. Middle East & Africa |

|

10. Competitive Landscape |

|

10.1. Overview of the Key Players |

|

10.2. Competitive Ecosystem |

|

10.2.1. Level of Fragmentation |

|

10.2.2. Market Consolidation |

|

10.2.3. Product Innovation |

|

10.3. Company Share Analysis |

|

10.4. Company Benchmarking Matrix |

|

10.4.1. Strategic Overview |

|

10.4.2. Product Innovations |

|

10.5. Start-up Ecosystem |

|

10.6. Strategic Competitive Insights/ Customer Imperatives |

|

10.7. ESG Matrix/ Sustainability Matrix |

|

10.8. Manufacturing Network |

|

10.8.1. Locations |

|

10.8.2. Supply Chain and Logistics |

|

10.8.3. Product Flexibility/Customization |

|

10.8.4. Digital Transformation and Connectivity |

|

10.8.5. Environmental and Regulatory Compliance |

|

10.9. Technology Readiness Level Matrix |

|

10.10. Technology Maturity Curve |

|

10.11. Buying Criteria |

|

11. Company Profiles |

|

11.1. Thermo Fisher Scientific Inc. |

|

11.1.1. Company Overview |

|

11.1.2. Company Financials |

|

11.1.3. Product/Service Portfolio |

|

11.1.4. Recent Developments |

|

11.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

11.2. Bio-Rad Laboratories, Inc. |

|

11.3. Illumina, Inc. |

|

11.4. F. Hoffmann-La Roche AG |

|

11.5. Abbott Laboratories |

|

11.6. QIAGEN N.V. |

|

11.7. GenDx |

|

11.8. Becton, Dickinson and Company (BD) |

|

11.9. SeraCare Life Sciences, Inc. |

|

11.10. Luminex Corporation |

|

11.11. Medipost Co., Ltd. |

|

11.12. Sequenom (now part of LabCorp) |

|

11.13. Organ Transplant Technologies, Inc. |

|

11.14. HLA Typing Services, Inc. |

|

11.15. Bio-Techne Corporation |

|

12. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the HLA Typing Transplant Diagnostics Services Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the HLA Typing Transplant Diagnostics Services Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the HLA Typing Transplant Diagnostics Services Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA