As per Intent Market Research, the High-K and ALD CVD Metal Precursors Market was valued at USD 3.0 billion in 2024-e and will surpass USD 4.8 billion by 2030; growing at a CAGR of 8.0% during 2024 - 2030.

The high-K and ALD CVD metal precursors market is integral to the production of advanced semiconductors, memory devices, and other electronic components that drive technological innovation across various industries. High-K materials, Atomic Layer Deposition (ALD), and Chemical Vapor Deposition (CVD) technologies are pivotal in enhancing the performance and efficiency of microelectronic devices. High-K materials, with their high dielectric constant, are used to fabricate the thin insulating layers in semiconductor devices, which are essential for reducing power consumption and improving performance. ALD and CVD are key deposition techniques that enable the precise and uniform application of these materials on semiconductor wafers, facilitating the production of next-generation integrated circuits.

The market for high-K and ALD CVD metal precursors has grown significantly, driven by the increasing demand for smaller, faster, and more energy-efficient electronic devices. As the need for advanced technologies like 5G, AI, and IoT intensifies, the demand for high-quality metal precursors for semiconductor fabrication continues to rise. These precursors play a crucial role in achieving the precise thin films required for the fabrication of semiconductor devices, memory devices, and logic devices, making them indispensable in modern electronics manufacturing.

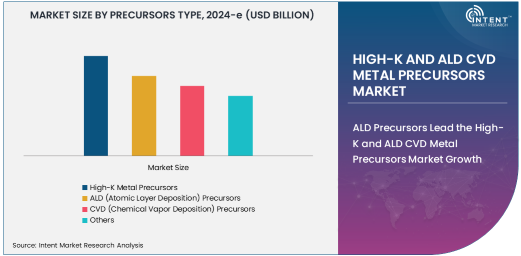

ALD Precursors Lead the High-K and ALD CVD Metal Precursors Market Growth

Among the different types of precursors, ALD (Atomic Layer Deposition) precursors are experiencing the fastest growth in the high-K and ALD CVD metal precursors market. ALD is a cutting-edge deposition technique used for fabricating thin films with atomic precision. This precision is essential for the production of semiconductor devices with smaller geometries, which is a growing trend in the semiconductor industry. The ability of ALD to deposit highly uniform and conformal thin films makes it ideal for the creation of high-performance components used in memory devices, logic devices, and integrated circuits. ALD precursors are crucial for depositing metal oxide, nitride, and other high-K dielectric materials in semiconductor manufacturing, and their demand is driven by the shift towards advanced semiconductor nodes that require extreme precision.

As semiconductor devices continue to scale down, ALD has become the preferred method for depositing thin films for high-K dielectrics and other materials. This trend is expected to accelerate with the development of new technologies like 3D NAND memory, advanced logic devices, and photonic devices. ALD’s ability to produce high-quality films at low temperatures also positions it as a key technology in the fabrication of future-generation electronics, which require increasingly complex material deposition techniques. With semiconductor fabrication advancing toward smaller and more complex structures, ALD precursors are anticipated to drive significant market growth in the coming years.

Tantalum (Ta) Metal Precursors Dominate in Semiconductor Fabrication

In terms of material types, tantalum (Ta) metal precursors hold the largest share in the high-K and ALD CVD metal precursors market. Tantalum is widely used in the semiconductor industry due to its excellent properties, including high melting point, corrosion resistance, and stable chemical behavior, which make it ideal for use in high-performance devices. Tantalum-based precursors are extensively employed in the deposition of tantalum films for semiconductor interconnects, capacitors, and gate electrodes. These applications are critical for the performance of memory devices, logic devices, and photonic devices, making tantalum an essential material in the semiconductor fabrication process.

The demand for tantalum metal precursors has been rising steadily, driven by the increased complexity of semiconductor devices and the miniaturization of integrated circuits. As the trend towards smaller, more energy-efficient devices continues, tantalum remains a material of choice for manufacturers looking to achieve high performance and reliability in their devices. The development of advanced manufacturing techniques, including ALD and CVD, further enhances the efficiency and application of tantalum precursors, ensuring their continued prominence in semiconductor fabrication.

Semiconductor Fabrication Drives the Largest Share in End-Use Applications

Among the various end-use applications, semiconductor fabrication represents the largest segment in the high-K and ALD CVD metal precursors market. The growing demand for semiconductors, driven by advancements in mobile devices, computing, and emerging technologies like AI, IoT, and 5G, is a key factor contributing to the substantial growth in this segment. High-K and ALD CVD metal precursors are crucial in the fabrication of semiconductor devices, enabling the precise deposition of thin films required for manufacturing integrated circuits, transistors, and memory chips. The increasing complexity of semiconductor devices and the continuous push toward smaller, more powerful chips are directly boosting the demand for advanced precursors.

Additionally, the ongoing evolution in semiconductor manufacturing processes, including the shift to smaller nodes, more advanced packaging technologies, and the rise of 3D ICs (integrated circuits), further intensifies the need for high-quality metal precursors. As the semiconductor industry moves toward more advanced technologies such as quantum computing and edge computing, the demand for high-performance metal precursors will continue to grow, making semiconductor fabrication the largest end-use segment in the high-K and ALD CVD metal precursors market.

Asia-Pacific Leads as the Fastest-Growing Region in the High-K and ALD CVD Metal Precursors Market

The Asia-Pacific (APAC) region is expected to witness the fastest growth in the high-K and ALD CVD metal precursors market, primarily due to the booming semiconductor industry in countries such as China, South Korea, Taiwan, and Japan. The APAC region is home to some of the world’s largest semiconductor manufacturers, including Samsung Electronics, TSMC, and Intel, which are increasingly adopting advanced deposition technologies such as ALD and CVD for their high-performance chips. This region’s dominance in semiconductor production is fueling the demand for high-K and ALD CVD metal precursors.

Moreover, APAC's growing focus on the development of emerging technologies, such as 5G infrastructure, AI applications, and advanced computing, is driving the need for more sophisticated and precise semiconductor components. The rise of local semiconductor fabs and government initiatives to support the semiconductor industry further contribute to the region's growth. With rapid advancements in semiconductor technology and increasing investments in research and development, APAC is poised to remain the fastest-growing region in the high-K and ALD CVD metal precursors market for the foreseeable future.

Competitive Landscape: Key Players and Market Dynamics

The high-K and ALD CVD metal precursors market is highly competitive, with numerous global and regional players vying for market share. Key companies involved in the production of high-quality metal precursors include Air Products and Chemicals, Merck Group, Honeywell International, Tokyo Ohka Kogyo Co., and Linde PLC. These companies are actively engaged in expanding their product portfolios, forming strategic partnerships, and enhancing their research and development capabilities to address the evolving needs of the semiconductor industry.

The competitive landscape is characterized by continuous innovation, with companies investing heavily in new materials, advanced deposition techniques, and customized solutions for semiconductor manufacturing. To maintain their competitive edge, market players are focusing on providing high-performance, cost-effective solutions that meet the demands of the rapidly evolving semiconductor industry. Additionally, regulatory frameworks and industry standards play a significant role in shaping the market, ensuring that manufacturers adhere to stringent quality and safety requirements.

Recent Developments:

- Merck Group introduced new high-performance CVD metal precursors for semiconductor applications, enhancing deposition efficiency.

- Air Products and Chemicals, Inc. expanded its portfolio of ALD precursors with a new product line designed for advanced logic and memory device manufacturing.

- Praxair Technology, Inc. partnered with leading semiconductor manufacturers to supply specialized metal precursors for next-generation electronic components.

- Dow Inc. announced the launch of a series of innovative high-K materials aimed at improving semiconductor device performance.

- Versum Materials, Inc. completed the acquisition of a metal precursor provider, strengthening its position in the ALD and CVD market.

List of Leading Companies:

- Air Products and Chemicals, Inc.

- Merck Group

- The Linde Group

- Praxair Technology, Inc.

- Kanto Chemical Co., Inc.

- Versum Materials, Inc.

- Dow Inc.

- Entegris, Inc.

- Albemarle Corporation

- Honeywell International Inc.

- JSR Corporation

- Tokyo Ohka Kogyo Co., Ltd. (TOK)

- Advanced Materials Technologies Ltd.

- Cabot Microelectronics Corporation

- Air Liquide S.A.

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 3.0 billion |

|

Forecasted Value (2030) |

USD 4.8 billion |

|

CAGR (2025 – 2030) |

8.0% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

High-K and ALD CVD Metal Precursors Market By Precursors Type (High-K Metal Precursors, ALD Precursors, CVD Precursors), By Material Type (Tantalum, Cobalt, Titanium, Ruthenium, Copper), By Application (Semiconductor Fabrication, Memory Devices, Logic Devices, Photovoltaic Cells,) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Air Products and Chemicals, Inc., Merck Group, The Linde Group, Praxair Technology, Inc., Kanto Chemical Co., Inc., Versum Materials, Inc., Dow Inc., Entegris, Inc., Albemarle Corporation, Honeywell International Inc., JSR Corporation, Tokyo Ohka Kogyo Co., Ltd. (TOK), Advanced Materials Technologies Ltd., Cabot Microelectronics Corporation, Air Liquide S.A. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. High-K and ALD CVD Metal Precursors Market, by Precursors Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. High-K Metal Precursors |

|

4.2. ALD (Atomic Layer Deposition) Precursors |

|

4.3. CVD (Chemical Vapor Deposition) Precursors |

|

4.4. Others |

|

5. High-K and ALD CVD Metal Precursors Market, by Material Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Tantalum (Ta) |

|

5.2. Cobalt (Co) |

|

5.3. Titanium (Ti) |

|

5.4. Ruthenium (Ru) |

|

5.5. Copper (Cu) |

|

5.6. Other Metals |

|

6. High-K and ALD CVD Metal Precursors Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Semiconductor Fabrication |

|

6.2. Memory Devices |

|

6.3. Logic Devices |

|

6.4. Photovoltaic Cells |

|

6.5. Others |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America High-K and ALD CVD Metal Precursors Market, by Precursors Type |

|

7.2.7. North America High-K and ALD CVD Metal Precursors Market, by Material Type |

|

7.2.8. North America High-K and ALD CVD Metal Precursors Market, by Application |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US High-K and ALD CVD Metal Precursors Market, by Precursors Type |

|

7.2.9.1.2. US High-K and ALD CVD Metal Precursors Market, by Material Type |

|

7.2.9.1.3. US High-K and ALD CVD Metal Precursors Market, by Application |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Air Products and Chemicals, Inc. |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Merck Group |

|

9.3. The Linde Group |

|

9.4. Praxair Technology, Inc. |

|

9.5. Kanto Chemical Co., Inc. |

|

9.6. Versum Materials, Inc. |

|

9.7. Dow Inc. |

|

9.8. Entegris, Inc. |

|

9.9. Albemarle Corporation |

|

9.10. Honeywell International Inc. |

|

9.11. JSR Corporation |

|

9.12. Tokyo Ohka Kogyo Co., Ltd. (TOK) |

|

9.13. Advanced Materials Technologies Ltd. |

|

9.14. Cabot Microelectronics Corporation |

|

9.15. Air Liquide S.A. |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the High-K and ALD CVD Metal Precursors Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the High-K and ALD CVD Metal Precursors Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the High-K and ALD CVD Metal Precursors Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA