As per Intent Market Research, the Urine Collection Bags Market was valued at USD 1.1 Billion in 2024-e and will surpass USD 1.8 Billion by 2030; growing at a CAGR of 8.7% during 2025 - 2030.

The urine collection bags market plays a critical role in managing the collection and storage of urine, particularly for individuals who are bedridden, elderly, or experiencing medical conditions that require urinary drainage. These devices are essential in healthcare settings and homecare environments, ensuring hygienic and efficient urine management. The market includes disposable and reusable urine collection bags, which are made from various materials such as PVC, silicone, and rubber. Given the increasing geriatric population and rising incidences of chronic diseases such as kidney disorders and urinary incontinence, the demand for urine collection bags continues to grow. Additionally, advancements in product designs and materials are further boosting the market's expansion.

The market is also impacted by factors such as the prevalence of hospital-acquired infections (HAIs), healthcare provider requirements for high-quality, reliable products, and an increasing awareness of the importance of hygiene in urinary care. Innovations in material science have led to the development of more comfortable, durable, and safer urine collection bags. These advancements are not only meeting the demands of healthcare providers but are also enhancing the quality of life for patients who rely on these products for daily management.

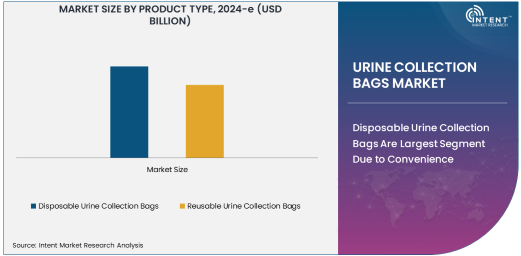

Disposable Urine Collection Bags Are Largest Segment Due to Convenience

Disposable urine collection bags are the largest segment in the urine collection bags market due to their convenience and hygiene benefits. Disposable bags are typically used for short-term collection purposes, especially in clinical settings or during hospital stays. They are favored for their ability to eliminate the risk of cross-contamination and ensure a high level of infection control. These bags are commonly used in hospitals, clinics, and emergency care units where patients require temporary urine collection solutions.

The ease of use and disposal of these bags contribute to their dominance in the market. Given that disposable urine collection bags are intended for one-time use, they are designed for single-patient use, preventing the risk of infection or contamination between different individuals. The widespread adoption of disposable products in healthcare environments, driven by the need for sanitary and safe medical practices, ensures that disposable urine collection bags remain the most commonly used option in the market.

PVC Is Largest Material Type Owing to Cost-Effectiveness and Durability

PVC (Polyvinyl Chloride) is the largest material type in the urine collection bags market, owing to its cost-effectiveness, durability, and flexibility. PVC is widely used in the manufacturing of both disposable and reusable urine collection bags due to its excellent resistance to chemicals and environmental stress. It provides a reliable and inexpensive solution for urine collection in healthcare settings and homecare environments.

The material's ability to be easily molded into different shapes and sizes also makes it ideal for creating urine collection bags that are user-friendly and highly functional. Additionally, PVC is lightweight, making the bags easy to transport and handle. Its affordability compared to other materials like silicone or rubber contributes to its widespread use in the market, ensuring that it remains the preferred material choice for urine collection bags across various applications.

Medium Capacity Urine Collection Bags Are Fastest Growing Segment

Medium capacity (500 ml to 1L) urine collection bags are the fastest-growing segment in the market, driven by the growing demand for bags that strike a balance between compactness and capacity. These bags are ideal for patients who require moderate urine collection volumes, particularly in hospital settings or homecare environments where patients may need to use the bags for longer periods.

The shift toward medium capacity bags is largely due to their versatility, as they cater to a wide range of patient needs, from those undergoing surgical procedures to individuals with chronic conditions such as incontinence or urinary retention. Their growing popularity is also attributed to the increased emphasis on patient comfort and the need for products that can support extended use without compromising hygiene or safety. As the number of patients requiring long-term urine collection solutions rises, medium capacity urine collection bags are becoming the preferred choice for many healthcare providers.

Healthcare Providers Are Largest End-Use Industry

Healthcare providers, including hospitals and clinics, are the largest end-use industry in the urine collection bags market, driven by the high volume of medical procedures and inpatient care where urine collection is necessary. Hospitals and clinics require large quantities of urine collection bags for patients undergoing surgeries, receiving treatments, or those with urinary retention or incontinence.

In addition to their role in patient care, healthcare providers are also focused on ensuring the safety and hygiene of their patients, making the proper choice of urine collection bags crucial. The ongoing rise in healthcare-associated infections (HAIs) further emphasizes the need for high-quality, disposable urine collection bags, particularly in hospitals. The large-scale demand from healthcare providers ensures their dominant position in the market, driving growth and innovation in this segment.

North America Is Largest Region Owing to Advanced Healthcare Infrastructure

North America is the largest region in the urine collection bags market, owing to its advanced healthcare infrastructure, high patient volume, and strong demand for medical products that ensure comfort and hygiene. The United States, in particular, is a major contributor to the growth of this market, driven by the high number of hospital admissions and surgeries, as well as the growing elderly population in the region who require urine collection solutions for conditions such as incontinence or urinary retention.

North America's highly developed healthcare systems and widespread awareness of hygiene standards contribute to the increased adoption of urine collection bags. Moreover, the presence of leading medical device manufacturers and distributors in this region ensures the availability of a wide range of products that meet the diverse needs of healthcare providers. The growing demand for long-term care in nursing homes and other healthcare facilities further supports the dominance of North America in the market.

Leading Companies and Competitive Landscape

The urine collection bags market is highly competitive, with a number of prominent players driving innovation and expanding their product portfolios. Leading companies in the market include B. Braun Melsungen AG, Coloplast A/S, Hollister Incorporated, and Medtronic. These companies offer a wide range of urine collection solutions, including both disposable and reusable products, catering to the needs of healthcare providers, hospitals, and patients worldwide.

The competitive landscape is characterized by a strong focus on product innovation, such as the development of more comfortable, secure, and hygienic urine collection bags. Key players are also concentrating on expanding their geographic presence and increasing their market share through strategic partnerships, acquisitions, and collaborations. As demand for urine collection bags continues to rise, companies are working to enhance product offerings and improve customer satisfaction, positioning themselves as leaders in the market.

Recent Developments:

- Hollister Incorporated launched an innovative line of anti-bacterial urine collection bags designed for extended wear.

- ConvaTec Group PLC acquired a urology product firm, expanding its portfolio in the urine collection and incontinence management market.

- Medtronic PLC announced a new, more eco-friendly version of its urine collection bags made from recyclable materials.

- B. Braun Melsungen AG introduced a new line of pediatric-friendly urine collection bags for hospital use.

- Teleflex Incorporated partnered with a leading healthcare provider to supply urine collection bags to long-term care facilities.

List of Leading Companies:

- B. Braun Melsungen AG

- Hollister Incorporated

- Medtronic PLC

- Coloplast A/S

- ConvaTec Group PLC

- Amsino International Inc.

- Teleflex Incorporated

- Smiths Medical

- Cardinal Health, Inc.

- Essity AB

- Dynarex Corporation

- Molnlycke Health Care

- Shiley Medical Products

- Medi-Globe GmbH

- Sterimed Group

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 1.1 Billion |

|

Forecasted Value (2030) |

USD 1.8 Billion |

|

CAGR (2025 – 2030) |

8.7% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Global Urine Collection Bags Market by Product Type (Disposable Urine Collection Bags, Reusable Urine Collection Bags), by Material (PVC, Silicone, Rubber), by Capacity (Small, Medium, Large), by Application (Hospital and Clinical Use, Homecare), by End-Use Industry (Healthcare Providers, Nursing Homes and Long-Term Care), and by Region |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

B. Braun Melsungen AG, Hollister Incorporated, Medtronic PLC, Coloplast A/S, ConvaTec Group PLC, Amsino International Inc., Smiths Medical, Cardinal Health, Inc., Essity AB, Dynarex Corporation, Molnlycke Health Care, Shiley Medical Products, Sterimed Group |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Urine Collection Bags Market, by Product Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Disposable Urine Collection Bags |

|

4.2. Reusable Urine Collection Bags |

|

5. Urine Collection Bags Market, by Material (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. PVC (Polyvinyl Chloride) |

|

5.2. Silicone |

|

5.3. Rubber |

|

6. Urine Collection Bags Market, by Capacity (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Small (Up to 500 ml) |

|

6.2. Medium (500 ml to 1L) |

|

6.3. Large (Above 1L) |

|

7. Urine Collection Bags Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Hospital and Clinical Use |

|

7.2. Homecare |

|

7.3. Others |

|

8. Urine Collection Bags Market, by End-Use Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Healthcare Providers (Hospitals & Clinics) |

|

8.2. Nursing Homes and Long-Term Care |

|

8.3. Others |

|

9. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

9.1. Regional Overview |

|

9.2. North America |

|

9.2.1. Regional Trends & Growth Drivers |

|

9.2.2. Barriers & Challenges |

|

9.2.3. Opportunities |

|

9.2.4. Factor Impact Analysis |

|

9.2.5. Technology Trends |

|

9.2.6. North America Urine Collection Bags Market, by Product Type |

|

9.2.7. North America Urine Collection Bags Market, by Material |

|

9.2.8. North America Urine Collection Bags Market, by Capacity |

|

9.2.9. North America Urine Collection Bags Market, by Application |

|

9.2.10. North America Urine Collection Bags Market, by End-Use Industry |

|

9.2.11. By Country |

|

9.2.11.1. US |

|

9.2.11.1.1. US Urine Collection Bags Market, by Product Type |

|

9.2.11.1.2. US Urine Collection Bags Market, by Material |

|

9.2.11.1.3. US Urine Collection Bags Market, by Capacity |

|

9.2.11.1.4. US Urine Collection Bags Market, by Application |

|

9.2.11.1.5. US Urine Collection Bags Market, by End-Use Industry |

|

9.2.11.2. Canada |

|

9.2.11.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

9.3. Europe |

|

9.4. Asia-Pacific |

|

9.5. Latin America |

|

9.6. Middle East & Africa |

|

10. Competitive Landscape |

|

10.1. Overview of the Key Players |

|

10.2. Competitive Ecosystem |

|

10.2.1. Level of Fragmentation |

|

10.2.2. Market Consolidation |

|

10.2.3. Product Innovation |

|

10.3. Company Share Analysis |

|

10.4. Company Benchmarking Matrix |

|

10.4.1. Strategic Overview |

|

10.4.2. Product Innovations |

|

10.5. Start-up Ecosystem |

|

10.6. Strategic Competitive Insights/ Customer Imperatives |

|

10.7. ESG Matrix/ Sustainability Matrix |

|

10.8. Manufacturing Network |

|

10.8.1. Locations |

|

10.8.2. Supply Chain and Logistics |

|

10.8.3. Product Flexibility/Customization |

|

10.8.4. Digital Transformation and Connectivity |

|

10.8.5. Environmental and Regulatory Compliance |

|

10.9. Technology Readiness Level Matrix |

|

10.10. Technology Maturity Curve |

|

10.11. Buying Criteria |

|

11. Company Profiles |

|

11.1. B. Braun Melsungen AG |

|

11.1.1. Company Overview |

|

11.1.2. Company Financials |

|

11.1.3. Product/Service Portfolio |

|

11.1.4. Recent Developments |

|

11.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

11.2. Hollister Incorporated |

|

11.3. Medtronic PLC |

|

11.4. Coloplast A/S |

|

11.5. ConvaTec Group PLC |

|

11.6. Amsino International Inc. |

|

11.7. Teleflex Incorporated |

|

11.8. Smiths Medical |

|

11.9. Cardinal Health, Inc. |

|

11.10. Essity AB |

|

11.11. Dynarex Corporation |

|

11.12. Molnlycke Health Care |

|

11.13. Shiley Medical Products |

|

11.14. Medi-Globe GmbH |

|

11.15. Sterimed Group |

|

12. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Global Urine Collection Bags Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Global Urine Collection Bags Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Global Urine Collection Bags Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA