As per Intent Market Research, the Urgent Care Apps Market was valued at USD 6.0 Billion in 2024-e and will surpass USD 18.1 Billion by 2030; growing at a CAGR of 20.2% during 2025 - 2030.

The urgent care apps market is experiencing rapid growth, driven by the increasing demand for immediate medical attention, especially in light of the growing telehealth adoption and the need for convenient healthcare solutions. These apps provide users with quick access to healthcare services, enabling them to consult healthcare professionals for non-emergency conditions without the need to visit a physical clinic. Urgent care apps are transforming the way people access healthcare, making it more accessible, affordable, and efficient. The continued shift toward digital healthcare platforms and the rise in smartphone usage are expected to propel the market forward in the coming years.

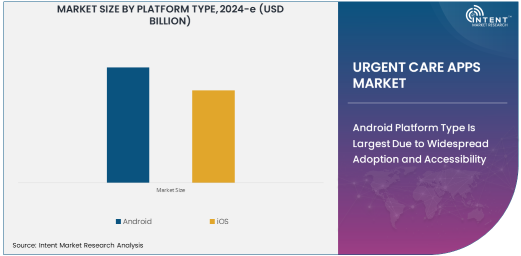

Android Platform Type Is Largest Due to Widespread Adoption and Accessibility

Among the platform types, Android holds the largest share of the urgent care apps market. The widespread adoption of Android smartphones globally, especially in emerging markets, makes it the preferred platform for urgent care app providers. Android's open-source nature allows for a wider range of app customization and development, enabling healthcare providers to create flexible and scalable solutions tailored to a diverse user base.

Additionally, the availability of Android apps across various price points, from budget to premium smartphones, ensures that a larger population can access urgent care services through their devices. As smartphone penetration continues to grow, the demand for Android-based urgent care apps is expected to increase steadily.

Telemedicine Service Type Is Fastest Growing Due to Increased Adoption of Remote Healthcare

Telemedicine is the fastest-growing service type in the urgent care apps market, driven by the growing preference for remote consultations. Telemedicine allows patients to receive medical care remotely, reducing the need for in-person visits, which is especially beneficial in urgent situations where time and convenience are of the essence. The COVID-19 pandemic significantly accelerated the adoption of telemedicine, and its popularity has persisted as both patients and healthcare providers recognize the value of remote healthcare services. With advancements in video conferencing technology, secure communication platforms, and the ability to conduct consultations via smartphones, telemedicine is poised to continue driving growth in the urgent care apps market.

Healthcare Providers End-Use Industry Is Largest Due to Need for Efficient Care Delivery

In the end-use industry segment, healthcare providers represent the largest market for urgent care apps. Healthcare providers, including hospitals, clinics, and private practitioners, are increasingly adopting urgent care apps to streamline their services, improve patient engagement, and reduce the burden on physical facilities.

These apps allow healthcare providers to offer consultations, schedule appointments, and manage patient data efficiently, contributing to more effective care delivery. As the healthcare sector embraces digital tools to improve service delivery and operational efficiency, the adoption of urgent care apps by healthcare providers is expected to remain strong, especially as demand for convenient healthcare services continues to rise.

Telehealth Providers End-Use Industry Is Fastest Growing Due to Expanding Remote Healthcare Infrastructure

The telehealth providers industry is experiencing the fastest growth in the urgent care apps market. With the expanding infrastructure for remote healthcare, telehealth providers are leveraging urgent care apps to enhance their offerings and meet the increasing demand for accessible healthcare. These apps allow telehealth providers to offer urgent care consultations, appointment scheduling, and follow-up care without the need for physical interaction, ensuring continuous care delivery.

As telehealth providers scale their operations to accommodate the rising demand for remote healthcare services, the adoption of urgent care apps in this sector is set to grow rapidly, supported by advancements in healthcare technologies and increasing consumer acceptance of virtual healthcare solutions.

North America Region Is Largest Market Due to Advanced Healthcare Systems and Technology Adoption

North America dominates the urgent care apps market, driven by its advanced healthcare infrastructure and widespread adoption of technology. The United States, in particular, has been a leader in telehealth and urgent care app adoption, with both healthcare providers and patients embracing digital healthcare solutions. Regulatory support, such as the introduction of telemedicine reimbursement policies and favorable government initiatives, has further accelerated the growth of the market in this region. Additionally, North America’s high smartphone penetration and growing focus on improving healthcare accessibility and convenience contribute to the strong demand for urgent care apps. As technology continues to advance, North America is expected to maintain its position as the largest market for urgent care apps.

Competitive Landscape and Key Players

The competitive landscape of the urgent care apps market is characterized by the presence of several key players offering a wide range of solutions for both healthcare providers and end-users. Leading companies in the market include Teladoc Health, MDTech, Babylon Health, and Doctor on Demand, which provide telemedicine services, virtual consultations, and appointment scheduling through their apps. These companies are continuously innovating their platforms by integrating features such as AI-driven diagnostics, real-time video consultations, and electronic health record (EHR) integration. As the market evolves, competition is intensifying with both established players and new entrants focusing on enhancing user experience, expanding service offerings, and ensuring regulatory compliance. Partnerships with healthcare providers, insurance companies, and telehealth networks are likely to shape the competitive dynamics of the urgent care apps market in the coming years.

Recent Developments:

- Teladoc Health announced a partnership with major health insurance providers to expand its telehealth services and offer discounted urgent care services through their platform.

- HealthTap launched a new feature that allows users to access virtual consultations with board-certified healthcare professionals for urgent care needs.

- Doctor on Demand expanded its reach by integrating with major employers to provide urgent care services as part of employee wellness programs.

- Babylon Health introduced a new AI-powered triage system in its urgent care app, helping patients quickly identify the severity of their condition and seek appropriate care.

- Practo launched a new urgent care platform in India, offering instant doctor consultations and access to medical advice for common illnesses and conditions.

List of Leading Companies:

- Teladoc Health

- MDTech

- HealthTap

- American Well

- Babylon Health

- LiveHealth Online

- Doctor on Demand

- HealthHero

- Push Doctor

- MyTelemedicine

- 98point6

- MeMD

- Practo

- Heal

- Pager

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 6.0 Billion |

|

Forecasted Value (2030) |

USD 18.1 Billion |

|

CAGR (2025 – 2030) |

20.2% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Global Urgent Care Apps Market by Platform Type (Android, iOS), by Service Type (Telemedicine, Appointment Scheduling, Virtual Consultations), by End-Use Industry (Healthcare Providers, Insurance Companies, Telehealth Providers) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Teladoc Health, MDTech, HealthTap, American Well, Babylon Health, LiveHealth Online, HealthHero, Push Doctor, MyTelemedicine, 98point6, MeMD, Practo, Pager |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Urgent Care Apps Market, by Platform Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Android |

|

4.2. iOS |

|

5. Urgent Care Apps Market, by Service Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Telemedicine |

|

5.2. Appointment Scheduling |

|

5.3. Virtual Consultations |

|

6. Urgent Care Apps Market, by End-Use Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Healthcare Providers |

|

6.2. Insurance Companies |

|

6.3. Telehealth Providers |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Urgent Care Apps Market, by Platform Type |

|

7.2.7. North America Urgent Care Apps Market, by Service Type |

|

7.2.8. North America Urgent Care Apps Market, by End-Use Industry |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Urgent Care Apps Market, by Platform Type |

|

7.2.9.1.2. US Urgent Care Apps Market, by Service Type |

|

7.2.9.1.3. US Urgent Care Apps Market, by End-Use Industry |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Teladoc Health |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. MDTech |

|

9.3. HealthTap |

|

9.4. American Well |

|

9.5. Babylon Health |

|

9.6. LiveHealth Online |

|

9.7. Doctor on Demand |

|

9.8. HealthHero |

|

9.9. Push Doctor |

|

9.10. MyTelemedicine |

|

9.11. 98point6 |

|

9.12. MeMD |

|

9.13. Practo |

|

9.14. Heal |

|

9.15. Pager |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Global Urgent Care Apps Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Global Urgent Care Apps Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Global Urgent Care Apps Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA