As per Intent Market Research, the Optical Lens Edger Market was valued at USD 1.8 Billion in 2024-e and will surpass USD 1.8 Billion by 2030; growing at a CAGR of 0.0% during 2025 - 2030.

The Optical Lens Edger Market is experiencing steady growth due to the increasing demand for precise, customized lenses in both the eyewear industry and medical applications. Optical lens edgers, which are used to shape and finish optical lenses, are critical tools in ensuring that lenses fit accurately into frames and meet specific visual requirements. Advancements in automation and technology have improved the efficiency, accuracy, and versatility of these devices, making them indispensable for optical laboratories, eyewear retailers, and healthcare providers worldwide.

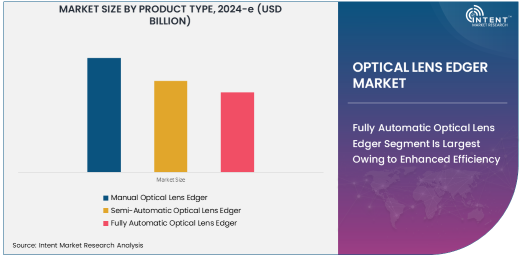

Fully Automatic Optical Lens Edger Segment Is Largest Owing to Enhanced Efficiency

The fully automatic optical lens edger segment is the largest in the market, driven by its efficiency and ability to process large volumes of lenses with minimal manual intervention. These edgers are equipped with advanced features that allow for high-precision lens shaping, reducing the risk of human error and streamlining the lens production process.

The demand for fully automatic lens edgers is increasing as eyewear retailers and optical laboratories seek to meet the growing demand for customized prescription and fashion lenses. Their ability to operate continuously with little operator oversight and deliver consistent, high-quality results makes them the preferred choice for businesses looking to enhance productivity and reduce turnaround times.

Semi-Automatic Optical Lens Edger Segment Is Fastest Growing Owing to Balance of Flexibility and Automation

The semi-automatic optical lens edger segment is the fastest-growing, as it offers a balanced solution between manual and fully automated systems. These devices provide operators with greater control over the lens edging process while incorporating automated features to improve consistency and speed.

Semi-automatic lens edgers are particularly popular in optical laboratories and smaller eyewear retailers where full automation may not be required. The flexibility of semi-automatic systems allows for both high customization and efficiency, making them an attractive option for businesses that need to process a moderate volume of lenses with varied specifications.

Prescription Lenses Segment Is Largest Application Owing to High Demand for Customized Solutions

The prescription lenses application segment is the largest in the Optical Lens Edger Market, as it directly correlates with the growing need for corrective eyewear. With increasing global rates of myopia, hyperopia, and other refractive errors, the demand for accurate and personalized prescription lenses is at an all-time high.

Optical lens edgers play a crucial role in ensuring that prescription lenses are cut to precise measurements and fitted into a wide range of frames. This segment's dominance is reinforced by ongoing advancements in lens technology, such as progressive lenses and high-index lenses, which require specialized edging processes for optimal fit and comfort.

Eyewear and Optics Retailers Segment Is Largest End-Use Industry Owing to High Volume Demand

Eyewear and optics retailers are the largest end-use industry for optical lens edgers, driven by the continuous demand for prescription and fashion eyewear. These retailers require efficient, high-quality lens edging systems to meet the fast turnaround times expected by customers, especially in the context of prescription lenses and customized eyewear.

As consumer preferences shift toward more personalized and fashionable eyewear, retailers are investing in advanced optical lens edgers to provide tailored solutions. The growing trend of online eyewear sales, coupled with the need for precise and speedy lens production, further contributes to the demand for optical lens edgers in the retail segment.

North America Is Largest Region Owing to Strong Eyewear Market and Technological Advancements

North America leads the Optical Lens Edger Market, driven by a combination of a large, established eyewear market and the adoption of cutting-edge lens technology. The region's demand for prescription lenses, coupled with its robust healthcare infrastructure, positions it as the largest market for optical lens edgers.

The presence of leading optical companies, along with high disposable incomes and consumer demand for customized eyewear, further supports market growth. Additionally, the increasing trend of personalized eyewear and the use of advanced optical technology in the region contribute to North America's dominance in the optical lens edger market.

Competitive Landscape and Key Players

The Optical Lens Edger Market is highly competitive, with key players such as Nidek Co., Ltd., Essilor International, and ZEISS Group leading the industry. These companies focus on advancing technology, offering a range of manual, semi-automatic, and fully automatic lens edgers to cater to diverse market needs.

The competitive dynamics of the market are shaped by product innovations, such as integration with digital measurement systems and enhanced precision cutting capabilities. Additionally, companies are expanding their geographic reach through strategic partnerships, acquisitions, and investments in R&D to maintain their leadership position and meet the growing demand for customized and efficient optical lens edging solutions.

Recent Developments:

- Essilor International launched a new fully automatic optical lens edger that integrates AI for faster lens processing.

- Zeiss International introduced a next-gen optical lens edger with enhanced precision, designed for high-volume optical labs.

- Nidek Co., Ltd. announced the release of an automated lens edger that features smart calibration for precision lens crafting.

- Hoya Corporation developed a semi-automatic optical lens edger designed to meet the needs of small-scale optical businesses.

- Satisloh AG unveiled a new range of fully automated optical lens edgers, focused on sustainability and reducing energy consumption in the production process.

List of Leading Companies:

- Essilor International S.A.

- Nikon Corporation

- Hoya Corporation

- Zeiss International

- Satisloh AG

- Shanghai Optics, Inc.

- OptoTech Optikmaschinen GmbH

- Schneider Optical Machines GmbH

- Topcon Corporation

- Nidek Co., Ltd.

- Coburn Technologies, Inc.

- D.W. Morgan

- Luneau Technology Group

- JOSAN Optical Machinery

- MEI Srl

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 1.1 Billion |

|

Forecasted Value (2030) |

USD 1.8 Billion |

|

CAGR (2025 – 2030) |

8.0% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Global Optical Lens Edger Market by Product Type (Manual Optical Lens Edger, Semi-Automatic Optical Lens Edger, Fully Automatic Optical Lens Edger), by End-Use Industry (Eyewear and Optics Retailers, Optical Laboratories, Hospitals and Clinics), by Application (Prescription Lenses, Sunglasses and Fashion Lenses, Medical Devices) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Essilor International S.A., Nikon Corporation, Hoya Corporation, Zeiss International, Satisloh AG, Shanghai Optics, Inc., Schneider Optical Machines GmbH, Topcon Corporation, Nidek Co., Ltd., Coburn Technologies, Inc., D.W. Morgan, Luneau Technology Group, MEI Srl |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Optical Lens Edger Market, by Product Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Manual Optical Lens Edger |

|

4.2. Semi-Automatic Optical Lens Edger |

|

4.3. Fully Automatic Optical Lens Edger |

|

5. Optical Lens Edger Market, by End-Use Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Eyewear and Optics Retailers |

|

5.2. Optical Laboratories |

|

5.3. Hospitals and Clinics |

|

6. Optical Lens Edger Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Prescription Lenses |

|

6.2. Sunglasses and Fashion Lenses |

|

6.3. Medical Devices |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Optical Lens Edger Market, by Product Type |

|

7.2.7. North America Optical Lens Edger Market, by End-Use Industry |

|

7.2.8. North America Optical Lens Edger Market, by Application |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Optical Lens Edger Market, by Product Type |

|

7.2.9.1.2. US Optical Lens Edger Market, by End-Use Industry |

|

7.2.9.1.3. US Optical Lens Edger Market, by Application |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Essilor International S.A. |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Nikon Corporation |

|

9.3. Hoya Corporation |

|

9.4. Zeiss International |

|

9.5. Satisloh AG |

|

9.6. Shanghai Optics, Inc. |

|

9.7. OptoTech Optikmaschinen GmbH |

|

9.8. Schneider Optical Machines GmbH |

|

9.9. Topcon Corporation |

|

9.10. Nidek Co., Ltd. |

|

9.11. Coburn Technologies, Inc. |

|

9.12. D.W. Morgan |

|

9.13. Luneau Technology Group |

|

9.14. JOSAN Optical Machinery |

|

9.15. MEI Srl |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Global Optical Lens Edger Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Global Optical Lens Edger Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Global Optical Lens Edger Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA