As per Intent Market Research, the Opioid Use Disorder Market was valued at USD 4.3 Billion in 2024-e and will surpass USD 14.3 Billion by 2030; growing at a CAGR of 22.4% during 2025 - 2030.

The opioid use disorder (OUD) market is seeing substantial growth, driven by the escalating opioid crisis globally and the increasing need for effective treatment options. OUD is a chronic condition characterized by the compulsive use of opioids despite harmful consequences, leading to a range of physical, psychological, and social challenges. Treatment for OUD typically involves a combination of medications and behavioral therapies aimed at reducing cravings, managing withdrawal symptoms, and supporting long-term recovery. As the prevalence of opioid addiction continues to rise, there is a growing emphasis on the development of more effective treatments and rehabilitation programs to address this pressing public health issue.

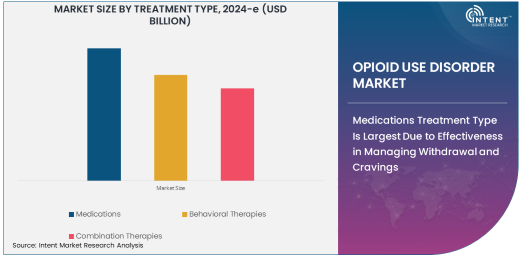

Medications Treatment Type Is Largest Due to Effectiveness in Managing Withdrawal and Cravings

Among the treatment types, medications represent the largest sub-segment in the opioid use disorder market. Medications, such as methadone, buprenorphine, and naltrexone, are widely used to help manage opioid withdrawal symptoms, reduce cravings, and prevent relapse. These medications work by acting on the opioid receptors in the brain, helping to stabilize patients and prevent the intense cravings and withdrawal symptoms that often lead to relapse.

The widespread use of opioid replacement therapies, such as methadone and buprenorphine, has proven to be highly effective in managing OUD, making medications the cornerstone of treatment. As the opioid crisis continues to grow, the demand for medication-assisted treatments is expected to increase, solidifying the dominance of this sub-segment.

Methadone Medication Type Is Largest Due to Long-Standing Efficacy in Managing OUD

In the medication type segment, methadone is the largest sub-segment due to its long-standing efficacy in managing opioid use disorder. Methadone, a synthetic opioid, has been used for decades as part of opioid replacement therapy (ORT) and is highly effective in preventing withdrawal symptoms and reducing cravings. By maintaining a stable level of opioids in the system, methadone helps individuals avoid the highs and lows associated with illicit opioid use, thus reducing the risk of relapse. Methadone has also been extensively studied, making it a well-established treatment option within the OUD market. Its widespread use in opioid treatment programs (OTPs) and healthcare facilities worldwide continues to make it the most commonly prescribed medication for OUD.

Buprenorphine Medication Type Is Fastest Growing Due to Accessibility and Reduced Risk of Abuse

Buprenorphine is the fastest-growing medication in the opioid use disorder treatment market. Buprenorphine, a partial agonist at opioid receptors, has become increasingly popular due to its lower potential for abuse compared to methadone. It is also easier to administer, often available in forms like sublingual tablets, and can be prescribed in outpatient settings, which increases its accessibility for patients. Buprenorphine has demonstrated effectiveness in reducing cravings and withdrawal symptoms while offering a safer profile, especially in terms of overdose risk. The growing shift toward outpatient treatment programs and the increased availability of buprenorphine for home use are expected to drive its adoption, making it a key player in the OUD market's expansion.

Healthcare Providers End-Use Industry Is Largest Due to Primary Role in Treatment Delivery

The healthcare providers segment is the largest end-use industry in the opioid use disorder market. Healthcare providers, including hospitals, clinics, and addiction treatment centers, are the primary institutions involved in diagnosing and treating opioid use disorder. These providers play a crucial role in delivering both pharmacological and behavioral interventions, offering medications, counseling services, and rehabilitation programs to individuals struggling with OUD. The significant focus on patient care, combined with increased government and healthcare policy support, ensures that healthcare providers continue to be the dominant segment for OUD treatment. As the opioid epidemic continues to impact public health, the demand for healthcare services tailored to addiction recovery is expected to grow substantially.

Rehabilitation Centers End-Use Industry Is Fastest Growing Due to Demand for Specialized Care

Rehabilitation centers are the fastest-growing end-use industry in the opioid use disorder market. These centers offer specialized services, including inpatient and outpatient rehabilitation programs, detoxification, counseling, and aftercare to individuals recovering from opioid addiction. As the recognition of OUD as a chronic condition grows, more patients are seeking specialized care in controlled environments that offer a comprehensive approach to recovery. Rehabilitation centers provide personalized treatment plans that include a combination of medications, therapy, and support systems to help individuals overcome addiction. With increasing awareness about the need for long-term recovery support, the demand for rehabilitation services is expected to rise, contributing to the growth of this segment.

North America Region Is Largest Market Due to High Prevalence of Opioid Use and Treatment Availability

North America holds the largest market share in the opioid use disorder market, largely due to the high prevalence of opioid use disorder and the extensive healthcare infrastructure available to treat it. The United States, in particular, has been at the forefront of addressing the opioid crisis, with widespread availability of opioid use disorder treatments and significant government initiatives to combat addiction. The establishment of opioid treatment programs (OTPs), the widespread availability of medications like methadone and buprenorphine, and the development of policies to support access to treatment contribute to the region's dominance. As the opioid epidemic continues to challenge public health in North America, the market for OUD treatments is expected to remain robust.

Competitive Landscape and Key Players

The opioid use disorder market is highly competitive, with numerous pharmaceutical companies and healthcare providers vying for leadership in treatment offerings. Key players in the market include Alkermes, Indivior, and Orexo, which develop and commercialize medications like buprenorphine and naltrexone for the treatment of OUD. Additionally, companies such as McKinsey & Company and other healthcare providers are involved in expanding access to addiction treatment services, including behavioral therapies and rehabilitation programs. The competitive landscape is shaped by ongoing research and development efforts, regulatory approvals, and the introduction of new medications and treatment models. With the rising demand for opioid use disorder treatments, market players are focusing on expanding their portfolios and improving the accessibility and effectiveness of their solutions to address the needs of an expanding patient population.

Recent Developments:

- Indivior PLC launched a new treatment for opioid use disorder, receiving FDA approval for its long-acting injectable formulation of buprenorphine.

- Alkermes announced a collaboration with a leading research institute to advance its opioid use disorder treatment pipeline, focusing on new formulations of naltrexone.

- Hikma Pharmaceuticals received regulatory approval for its generic version of naloxone, a life-saving drug used to reverse opioid overdoses, expanding its portfolio in addiction treatment.

- Reckitt Benckiser Group introduced a new digital tool designed to assist in the behavioral treatment of opioid use disorder, offering virtual therapy sessions and support.

- Janssen Pharmaceuticals launched a nationwide campaign to raise awareness about opioid use disorder treatment options, highlighting the benefits of its opioid addiction medications.

List of Leading Companies:

- Indivior PLC

- Alkermes

- Hikma Pharmaceuticals

- Mylan Pharmaceuticals

- Pfizer Inc.

- Teva Pharmaceutical Industries

- Reckitt Benckiser Group

- Orexo AB

- Janssen Pharmaceuticals (Johnson & Johnson)

- Nalych GmbH

- Heron Therapeutics

- Braeburn Pharmaceuticals

- Catalent, Inc.

- Elanco Animal Health

- Sanofi

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 4.3 Billion |

|

Forecasted Value (2030) |

USD 14.3 Billion |

|

CAGR (2025 – 2030) |

22.4% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Global Opioid Use Disorder Market by Treatment Type (Medications, Behavioral Therapies, Combination Therapies), by Medication Type (Methadone, Buprenorphine, Naltrexone, Naloxone), by End-Use Industry (Healthcare Providers, Pharmaceutical Companies, Rehabilitation Centers) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Indivior PLC, Alkermes, Hikma Pharmaceuticals, Mylan Pharmaceuticals, Pfizer Inc., Teva Pharmaceutical Industries, Orexo AB, Janssen Pharmaceuticals (Johnson & Johnson), Nalych GmbH, Heron Therapeutics, Braeburn Pharmaceuticals, Catalent, Inc., Sanofi |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Opioid Use Disorder Market, by Treatment Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Medications |

|

4.2. Behavioral Therapies |

|

4.3. Combination Therapies |

|

5. Opioid Use Disorder Market, by Medication Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Methadone |

|

5.2. Buprenorphine |

|

5.3. Naltrexone |

|

5.4. Naloxone |

|

6. Opioid Use Disorder Market, by End-Use Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Healthcare Providers |

|

6.2. Pharmaceutical Companies |

|

6.3. Rehabilitation Centers |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Opioid Use Disorder Market, by Treatment Type |

|

7.2.7. North America Opioid Use Disorder Market, by Medication Type |

|

7.2.8. North America Opioid Use Disorder Market, by End-Use Industry |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Opioid Use Disorder Market, by Treatment Type |

|

7.2.9.1.2. US Opioid Use Disorder Market, by Medication Type |

|

7.2.9.1.3. US Opioid Use Disorder Market, by End-Use Industry |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. Indivior PLC |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Alkermes |

|

9.3. Hikma Pharmaceuticals |

|

9.4. Mylan Pharmaceuticals |

|

9.5. Pfizer Inc. |

|

9.6. Teva Pharmaceutical Industries |

|

9.7. Reckitt Benckiser Group |

|

9.8. Orexo AB |

|

9.9. Janssen Pharmaceuticals (Johnson & Johnson) |

|

9.10. Nalych GmbH |

|

9.11. Heron Therapeutics |

|

9.12. Braeburn Pharmaceuticals |

|

9.13. Catalent, Inc. |

|

9.14. Elanco Animal Health |

|

9.15. Sanofi |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Global Opioid Use Disorder Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Global Opioid Use Disorder Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Global Opioid Use Disorder Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA