As per Intent Market Research, the Glass Manufacturing Market was valued at USD 80.1 billion in 2024-e and will surpass USD 100.3 billion by 2030; growing at a CAGR of 3.8% during 2025 - 2030.

The glass manufacturing market is a significant sector within the global materials industry, driven by its wide range of applications across multiple industries, including construction, automotive, packaging, electronics, and solar energy. Glass, due to its versatility, transparency, and durability, plays an integral role in many essential products, from windows and bottles to electronic devices and renewable energy solutions. With increasing industrialization and urbanization, the demand for glass has continued to rise, especially in emerging economies. Furthermore, the shift towards more sustainable, energy-efficient, and eco-friendly glass products is fueling innovation within the market, creating opportunities for growth.

Technological advancements, such as the development of energy-efficient glass and the use of recycled glass in manufacturing processes, are enhancing the industry's ability to meet both environmental and performance demands. The market is also benefiting from growing applications in renewable energy, where glass is used in the production of solar panels. As the need for high-performance and environmentally responsible materials continues to grow, the glass manufacturing market is expected to experience robust demand across various sectors, with key players focusing on both innovation and sustainability to maintain a competitive edge.

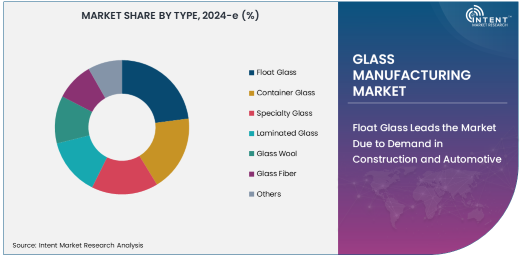

Float Glass Leads the Market Due to Demand in Construction and Automotive

Float glass holds the largest share in the glass manufacturing market, driven by its widespread use in the construction and automotive industries. This type of glass is produced through the float process, where molten glass is floated over a bed of molten metal to create a smooth, uniform thickness. The resulting product is ideal for use in windows, facades, mirrors, and architectural glazing due to its clarity, strength, and versatility.

The growth in the construction and real estate sectors, coupled with increasing demand for energy-efficient buildings, has contributed significantly to the demand for float glass. In the automotive industry, float glass is extensively used for windshields, side windows, and rear windows due to its durability and ability to be molded into various shapes. The increasing focus on vehicle safety, improved aerodynamics, and design innovation further drives the demand for float glass in automotive applications. As these industries continue to expand, the float glass segment is expected to maintain its dominance in the glass manufacturing market.

Glass Fiber is the Fastest Growing Segment, Driven by Demand in Electronics and Renewable Energy

Glass fiber is the fastest-growing segment within the glass manufacturing market, driven by its growing applications in electronics, automotive, and renewable energy. Glass fiber is known for its lightweight, high-strength properties and is used in a wide range of applications, including reinforcing composite materials for industries such as aerospace, automotive, and construction. It is particularly valued for its role in enhancing the structural integrity of lightweight components, making it a critical material for energy-efficient vehicles and infrastructure.

The renewable energy sector is also a significant driver of the growth in glass fiber demand, particularly in the production of wind turbines and solar panels. The increasing adoption of wind and solar energy technologies has resulted in a higher need for durable and lightweight materials, where glass fiber plays a crucial role in enhancing the performance of these systems. With the rising focus on sustainable energy solutions, glass fiber is positioned for continued growth, making it a key segment to watch within the glass manufacturing market.

Construction Industry Dominates the End-Use Market for Glass Products

The construction industry is the largest end-user of glass products, accounting for a significant portion of the overall demand. Glass is an essential material in construction, used for windows, facades, doors, and other architectural elements that require transparency, durability, and aesthetic appeal. As urbanization and infrastructure development continue to grow globally, especially in emerging markets, the demand for glass in construction is expected to rise.

Additionally, the construction industry's growing emphasis on energy-efficient buildings and green construction has further boosted the demand for specialized glass products. For example, energy-efficient and low-emissivity glass, which helps regulate temperature and reduce energy consumption, is increasingly used in residential, commercial, and industrial buildings. The growing trend toward smart buildings, which incorporate automated systems and sustainable materials, is also driving innovation in the glass sector, creating new opportunities for the market.

Asia Pacific Region Experiences Rapid Growth, Led by China and India

The Asia Pacific region is experiencing the fastest growth in the glass manufacturing market, driven by the rapid industrialization, urbanization, and infrastructural development in countries such as China, India, and Southeast Asian nations. The region's expanding construction and automotive sectors, coupled with the increasing demand for consumer electronics and renewable energy, are significantly contributing to the growth of the glass market.

China, as the largest producer and consumer of glass products, plays a pivotal role in the global market, with its vast manufacturing capacity and growing demand for glass in construction, automotive, and electronics. India is also emerging as a key growth market, with substantial investments in infrastructure projects, automotive manufacturing, and the adoption of renewable energy technologies. As these countries continue to develop, the Asia Pacific region is expected to remain a key growth driver for the global glass manufacturing market.

Competitive Landscape and Leading Companies

The glass manufacturing market is highly competitive, with several global and regional players focusing on innovation, sustainability, and efficiency to maintain their market position. Leading companies in the market include Saint-Gobain, Owens Corning, NSG Group, Asahi Glass Co., and Corning Inc., which are known for their extensive product portfolios and advanced manufacturing capabilities. These companies are focusing on developing specialized glass products that cater to diverse industries such as construction, automotive, electronics, and renewable energy.

Competition in the market is also driven by the increasing demand for eco-friendly and energy-efficient glass products, prompting companies to invest in research and development to produce sustainable and high-performance solutions. Strategic partnerships, mergers, acquisitions, and investments in new technologies are common in the market as companies seek to expand their market presence and meet the evolving needs of customers. As the demand for glass continues to grow across various industries, leading players are expected to play a critical role in shaping the future of the glass manufacturing market.

Recent Developments:

- In December 2024, Corning Inc. launched a new line of eco-friendly glass products aimed at reducing energy consumption in commercial buildings.

- In November 2024, Saint-Gobain acquired a specialty glass manufacturing facility to strengthen its portfolio in high-performance glass products.

- In October 2024, PPG Industries unveiled a new glass coating technology designed to enhance the durability and efficiency of solar panels.

- In September 2024, Guardian Industries expanded its production capacity for automotive glass to meet the rising demand in the electric vehicle sector.

- In August 2024, SCHOTT AG announced a partnership with a major tech company to develop advanced glass components for next-generation electronic devices.

List of Leading Companies:

- Saint-Gobain

- Corning Inc.

- Guardian Industries

- Asahi Glass Co. Ltd.

- Nippon Sheet Glass Co. Ltd.

- AGC Inc.

- SCHOTT AG

- PPG Industries

- Vitro S.A.B. de C.V.

- China National Glass Industrial Group Corporation

- Owens-Illinois Inc.

- Euroglas GmbH

- Xinyi Glass Holdings Limited

- Fenzi S.p.A.

- RHI Magnesita

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 80.1 billion |

|

Forecasted Value (2030) |

USD 100.3 billion |

|

CAGR (2025 – 2030) |

3.8% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Glass Manufacturing Market By Type (Float Glass, Container Glass, Specialty Glass, Laminated Glass, Glass Wool, Glass Fiber), By Material (Soda Lime Glass, Borosilicate Glass, Lead Glass, Tempered Glass, Glass Ceramics), By Process (Batch Process, Continuous Process, Blow and Blow Process, Press and Blow Process), By End-Use Industry (Construction, Automotive, Packaging, Electronics, Solar Energy) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Saint-Gobain, Corning Inc., Guardian Industries, Asahi Glass Co. Ltd., Nippon Sheet Glass Co. Ltd., AGC Inc., SCHOTT AG, PPG Industries, Vitro S.A.B. de C.V., China National Glass Industrial Group Corporation, Owens-Illinois Inc., Euroglas GmbH, Xinyi Glass Holdings Limited, Fenzi S.p.A., RHI Magnesita |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Glass Manufacturing Market, by Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Float Glass |

|

4.2. Container Glass |

|

4.3. Specialty Glass |

|

4.4. Laminated Glass |

|

4.5. Glass Wool |

|

4.6. Glass Fiber |

|

4.7. Others |

|

5. Glass Manufacturing Market, by Material (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Soda Lime Glass |

|

5.2. Borosilicate Glass |

|

5.3. Lead Glass |

|

5.4. Tempered Glass |

|

5.5. Glass Ceramics |

|

6. Glass Manufacturing Market, by Process (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Batch Process |

|

6.2. Continuous Process |

|

6.3. Blow and Blow Process |

|

6.4. Press and Blow Process |

|

7. Glass Manufacturing Market, by End-Use Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Construction |

|

7.2. Automotive |

|

7.3. Packaging |

|

7.4. Electronics |

|

7.5. Solar Energy |

|

7.6. Others |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Glass Manufacturing Market, by Type |

|

8.2.7. North America Glass Manufacturing Market, by Material |

|

8.2.8. North America Glass Manufacturing Market, by Process |

|

8.2.9. North America Glass Manufacturing Market, by End-Use Industry |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Glass Manufacturing Market, by Type |

|

8.2.10.1.2. US Glass Manufacturing Market, by Material |

|

8.2.10.1.3. US Glass Manufacturing Market, by Process |

|

8.2.10.1.4. US Glass Manufacturing Market, by End-Use Industry |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Saint-Gobain |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Corning Inc. |

|

10.3. Guardian Industries |

|

10.4. Asahi Glass Co. Ltd. |

|

10.5. Nippon Sheet Glass Co. Ltd. |

|

10.6. AGC Inc. |

|

10.7. SCHOTT AG |

|

10.8. PPG Industries |

|

10.9. Vitro S.A.B. de C.V. |

|

10.10. China National Glass Industrial Group Corporation |

|

10.11. Owens-Illinois Inc. |

|

10.12. Euroglas GmbH |

|

10.13. Xinyi Glass Holdings Limited |

|

10.14. Fenzi S.p.A. |

|

10.15. RHI Magnesita |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Glass Manufacturing Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Glass Manufacturing Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Glass Manufacturing Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA