As per Intent Market Research, the Generic Sterile Injectable Market was valued at USD 38.9 billion in 2024-e and will surpass USD 88.8 billion by 2030; growing at a CAGR of 12.5% during 2025 - 2030.

The generic injectable market plays a crucial role in the global pharmaceutical industry, providing cost-effective alternatives to branded injectable medications. With a growing emphasis on affordability and accessibility of healthcare, particularly in emerging markets, generic injectables have gained significant traction. These products are increasingly used across a wide range of therapeutic applications, offering therapeutic equivalence to their branded counterparts. The market has seen growth across various segments, driven by factors such as the aging population, increasing prevalence of chronic diseases, and rising demand for cost-effective medical solutions. This report focuses on key segments within the generic injectable market, highlighting both the largest and fastest-growing subsegments.

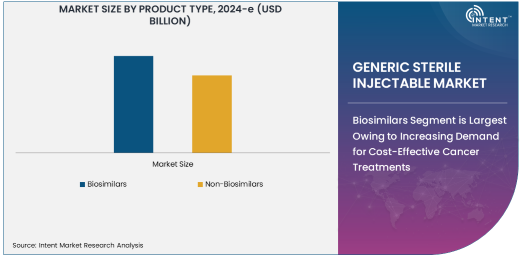

Biosimilars Segment is Largest Owing to Increasing Demand for Cost-Effective Cancer Treatments

Among the various product types within the generic injectable market, biosimilars represent the largest subsegment. Biosimilars are biologic medical products that are highly similar to already approved reference products, offering significant cost savings compared to branded biologics. The increasing demand for biosimilars can be attributed to the growing prevalence of chronic diseases such as cancer and autoimmune disorders, which require expensive biologic therapies. Furthermore, many patents for branded biologics are expiring, leading to a surge in biosimilar approvals and market entry. As healthcare systems and insurance providers increasingly focus on reducing treatment costs, biosimilars are expected to dominate the injectable market, providing access to life-saving treatments at a fraction of the cost.

The oncology therapeutic application is particularly significant for biosimilars, as the demand for cancer treatments continues to rise globally. Cancer therapies are often among the most expensive treatments, making biosimilars a more affordable alternative for both patients and healthcare providers. This trend is expected to continue, with biosimilars accounting for a growing share of the oncology injectable market. Additionally, the approval of more biosimilars in various therapeutic areas is poised to enhance their adoption, thereby reinforcing their position as the largest subsegment within the generic injectable market.

Oncology Segment is Fastest Growing Owing to Rising Cancer Incidences

In terms of therapeutic applications, oncology is the fastest growing subsegment in the generic injectable market. The global rise in cancer cases, combined with the high cost of cancer treatments, has led to a growing demand for more affordable alternatives, particularly generic injectables. Cancer is a leading cause of death worldwide, with increasing numbers of people being diagnosed with the disease each year. As a result, there is a pressing need for cost-effective treatment options that can be provided on a larger scale, which is where generic injectables play a vital role. Chemotherapies and immunotherapies, which often come in injectable forms, are seeing a significant shift towards more affordable generics.

The growth of the oncology segment is also fueled by advancements in treatment regimens that require more frequent administration of injectable drugs, further driving the demand for generic injectables. Generic oncology injectables are poised for strong growth as healthcare providers seek ways to make cancer treatment more accessible while keeping costs under control. In addition, biosimilars within the oncology space, which offer comparable efficacy to branded products, are expected to contribute to this growth trend, particularly as patents for biologic oncology treatments expire.

Hospitals Segment is Largest Owing to Dominance in Medical Settings

The largest end-user industry for generic injectables is hospitals. Hospitals serve as the primary point of care for patients requiring injectable treatments, especially for chronic conditions, surgeries, and cancer therapies. Hospitals are equipped with the necessary infrastructure and resources to handle injectable medications, making them the leading consumer of generic injectables. The demand for affordable medications within hospital settings, driven by budget constraints and the need for efficient care, positions hospitals as the largest subsegment in the generic injectable market.

In addition, hospitals often purchase injectables in large quantities due to the high volume of patients they serve. This volume buying further cements hospitals’ role as the dominant end-user industry. The hospital segment’s position is also strengthened by the fact that hospitals are increasingly adopting generic drugs as part of their cost-saving measures, particularly in oncology and cardiovascular treatments. As a result, hospitals are expected to maintain their leading role in the generic injectable market.

Direct Sales Segment is Fastest Growing Owing to Shift Toward Cost-Effective Channels

The fastest-growing distribution channel for generic injectables is direct sales. Pharmaceutical companies are increasingly engaging in direct sales strategies to reach healthcare providers and institutions, bypassing third-party distributors. This approach allows for more control over pricing and product distribution, aligning with the growing demand for affordable medications. Direct sales also enable pharmaceutical companies to forge closer relationships with hospitals, clinics, and other healthcare providers, which is crucial for the success of generic injectables in the market.

This trend is particularly important as healthcare systems around the world place a greater emphasis on cost-effectiveness. The ability to offer competitive pricing while maintaining high product quality through direct sales is a significant driver of market growth. The increase in direct sales is expected to continue as pharmaceutical companies look for ways to enhance their market reach and build a more efficient distribution system for generic injectables.

Vials Segment is Largest Owing to Popularity and Convenience

Among the various formulation types, vials represent the largest subsegment in the generic injectable market. Vials are widely used for the packaging of injectable medications, especially in hospital settings, due to their convenience, ease of use, and cost-effectiveness. Vials allow for multiple doses of medication to be extracted, which is advantageous for healthcare providers managing patients who require consistent dosing. This makes vials particularly popular for a variety of therapeutic applications, including oncology and cardiovascular treatments.

The large volume of injectable drugs used in hospitals, combined with the relatively lower cost of vial packaging compared to other formulations, ensures that vials continue to dominate the generic injectable market. As the demand for injectable drugs increases, particularly in oncology, the vial segment is expected to maintain its leadership position in terms of both volume and market share.

Regional Outlook: North America is Largest Market Due to High Healthcare Spending

North America holds the largest share of the global generic injectable market. The region benefits from well-established healthcare infrastructure, high healthcare spending, and a favorable regulatory environment for generic drugs. The U.S., in particular, is the largest consumer of generic injectables, with a large and aging population that drives the demand for injectable treatments, especially in therapeutic areas like oncology and cardiovascular diseases. Moreover, the U.S. FDA has been proactive in approving generic drugs, ensuring a steady flow of cost-effective options for the market.

In addition, the increasing preference for generic drugs, particularly in the hospital and outpatient settings, further strengthens North America's position as the largest market. The region is also seeing significant growth in the adoption of biosimilars, which is expected to continue as more biologic patents expire. As a result, North America remains the dominant region in the global generic injectable market, with continued growth anticipated in the coming years.

Competitive Landscape

The generic injectable market is highly competitive, with numerous players vying for market share. Leading companies such as Teva Pharmaceuticals, Sandoz, Mylan (Viatris), and Pfizer dominate the market, offering a wide range of injectable drugs across various therapeutic areas. These companies are investing heavily in expanding their portfolios of generic injectables, with a focus on oncology, cardiovascular, and infectious disease treatments. Furthermore, the entry of biosimilars into the market has intensified competition, as companies race to launch more affordable alternatives to branded biologic drugs.

The market is also seeing strategic partnerships, mergers, and acquisitions as companies aim to enhance their capabilities in manufacturing, R&D, and distribution. In addition, regulatory approvals and the expiration of patents for branded drugs continue to play a significant role in shaping the competitive landscape. As the market continues to grow, the focus on cost-effectiveness and high-quality injectable drugs will remain key drivers for success.

Recent Developments:

- Pfizer Inc. announced the launch of a new generic sterile injectable for oncology applications, expanding its oncology treatment portfolio.

- Teva Pharmaceutical Industries received FDA approval for a generic sterile injectable used in the treatment of heart disease, strengthening its cardiovascular portfolio.

- Fresenius Kabi AG has entered into an acquisition agreement with a major sterile injectable manufacturer to increase its production capabilities in the U.S. market.

- Amgen Inc. launched a new biosimilar sterile injectable for treating autoimmune diseases, competing with top-selling biologics in the market.

- Mylan (Viatris) completed the merger with Upjohn, increasing its capacity to provide generic injectables, expanding global market reach, and creating a stronger supply chain for its sterile injectables

List of Leading Companies:

- Pfizer Inc.

- Teva Pharmaceutical Industries Ltd.

- Novartis AG (Sandoz)

- Mylan N.V. (Viatris)

- Amgen Inc.

- Sanofi S.A.

- Fresenius Kabi AG

- Baxter International Inc.

- Eli Lilly and Co.

- Boehringer Ingelheim GmbH

- Dr. Reddy's Laboratories Ltd.

- Cipla Ltd.

- Hikma Pharmaceuticals PLC

- Apotex Inc.

- Aurobindo Pharma

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 38.9 Billion |

|

Forecasted Value (2030) |

USD 88.8 Billion |

|

CAGR (2025 – 2030) |

12.5% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Generic Injectable Market By Product Type (Biosimilars, Non-Biosimilars), By Therapeutic Application (Oncology, Cardiovascular Diseases, Neurological Disorders, Diabetes, Infectious Diseases), By End-User Industry (Hospitals, Clinics, Retail Pharmacies, Online Pharmacies), By Distribution Channel (Direct Sales, Third-Party Distributors, Online Sales), and By Formulation Type (Vials, Pre-Filled Syringes, Ampoules) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Pfizer Inc., Teva Pharmaceutical Industries Ltd., Novartis AG (Sandoz), Mylan N.V. (Viatris), Amgen Inc., Sanofi S.A., Fresenius Kabi AG, Baxter International Inc., Eli Lilly and Co., Boehringer Ingelheim GmbH, Dr. Reddy's Laboratories Ltd., Cipla Ltd., Hikma Pharmaceuticals PLC, Apotex Inc., Aurobindo Pharma |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Generic Sterile Injectable Market, by Product Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Biosimilars |

|

4.2. Non-Biosimilars |

|

5. Generic Sterile Injectable Market, by Therapeutic Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Oncology |

|

5.2. Cardiovascular Diseases |

|

5.3. Neurological Disorders |

|

5.4. Diabetes |

|

5.5. Infectious Diseases |

|

5.6. Others |

|

6. Generic Sterile Injectable Market, by End-User Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Hospitals |

|

6.2. Clinics |

|

6.3. Retail Pharmacies |

|

6.4. Online Pharmacies |

|

7. Generic Sterile Injectable Market, by Distribution Channel (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Direct Sales |

|

7.2. Third-Party Distributors |

|

7.3. Online Sales |

|

8. Generic Sterile Injectable Market, by Formulation Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Vials |

|

8.2. Pre-Filled Syringes |

|

8.3. Ampoules |

|

8.4. Others |

|

9. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

9.1. Regional Overview |

|

9.2. North America |

|

9.2.1. Regional Trends & Growth Drivers |

|

9.2.2. Barriers & Challenges |

|

9.2.3. Opportunities |

|

9.2.4. Factor Impact Analysis |

|

9.2.5. Technology Trends |

|

9.2.6. North America Generic Sterile Injectable Market, by Product Type |

|

9.2.7. North America Generic Sterile Injectable Market, by Therapeutic Application |

|

9.2.8. North America Generic Sterile Injectable Market, by End-User Industry |

|

9.2.9. North America Generic Sterile Injectable Market, by Distribution Channel |

|

9.2.10. North America Generic Sterile Injectable Market, by Formulation Type |

|

9.2.11. By Country |

|

9.2.11.1. US |

|

9.2.11.1.1. US Generic Sterile Injectable Market, by Product Type |

|

9.2.11.1.2. US Generic Sterile Injectable Market, by Therapeutic Application |

|

9.2.11.1.3. US Generic Sterile Injectable Market, by End-User Industry |

|

9.2.11.1.4. US Generic Sterile Injectable Market, by Distribution Channel |

|

9.2.11.1.5. US Generic Sterile Injectable Market, by Formulation Type |

|

9.2.11.2. Canada |

|

9.2.11.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

9.3. Europe |

|

9.4. Asia-Pacific |

|

9.5. Latin America |

|

9.6. Middle East & Africa |

|

10. Competitive Landscape |

|

10.1. Overview of the Key Players |

|

10.2. Competitive Ecosystem |

|

10.2.1. Level of Fragmentation |

|

10.2.2. Market Consolidation |

|

10.2.3. Product Innovation |

|

10.3. Company Share Analysis |

|

10.4. Company Benchmarking Matrix |

|

10.4.1. Strategic Overview |

|

10.4.2. Product Innovations |

|

10.5. Start-up Ecosystem |

|

10.6. Strategic Competitive Insights/ Customer Imperatives |

|

10.7. ESG Matrix/ Sustainability Matrix |

|

10.8. Manufacturing Network |

|

10.8.1. Locations |

|

10.8.2. Supply Chain and Logistics |

|

10.8.3. Product Flexibility/Customization |

|

10.8.4. Digital Transformation and Connectivity |

|

10.8.5. Environmental and Regulatory Compliance |

|

10.9. Technology Readiness Level Matrix |

|

10.10. Technology Maturity Curve |

|

10.11. Buying Criteria |

|

11. Company Profiles |

|

11.1. Pfizer Inc. |

|

11.1.1. Company Overview |

|

11.1.2. Company Financials |

|

11.1.3. Product/Service Portfolio |

|

11.1.4. Recent Developments |

|

11.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

11.2. Teva Pharmaceutical Industries Ltd. |

|

11.3. Novartis AG (Sandoz) |

|

11.4. Mylan N.V. (Viatris) |

|

11.5. Amgen Inc. |

|

11.6. Sanofi S.A. |

|

11.7. Fresenius Kabi AG |

|

11.8. Baxter International Inc. |

|

11.9. Eli Lilly and Co. |

|

11.10. Boehringer Ingelheim GmbH |

|

11.11. Dr. Reddy's Laboratories Ltd. |

|

11.12. Cipla Ltd. |

|

11.13. Hikma Pharmaceuticals PLC |

|

11.14. Apotex Inc. |

|

11.15. Aurobindo Pharma |

|

12. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Generic Sterile Injectable Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Generic Sterile Injectable Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Generic Sterile Injectable Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

parent market and relevant adjacencies to measure the impact of them on the Generic Injectable Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Generic Injectable Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA