As per Intent Market Research, the Generative Design Market was valued at USD 2.1 billion in 2023 and will surpass USD 4.0 billion by 2030; growing at a CAGR of 9.7% during 2024 - 2030.

The generative design market is rapidly transforming product development across industries by leveraging artificial intelligence (AI) and machine learning algorithms to create optimal design solutions. By inputting specific goals, constraints, and requirements into the generative design software, engineers and designers can explore a multitude of design possibilities, resulting in more innovative, efficient, and sustainable products. The technology is proving invaluable in industries such as automotive, aerospace, and industrial manufacturing, where complex parts and structures require high precision and performance. Generative design helps reduce material waste, lower production costs, and speed up the design process, making it a game-changer for modern product development.

As industries embrace digital transformation, the demand for generative design solutions continues to surge. The technology's ability to create design alternatives that humans might not typically consider has made it essential for achieving next-level product optimization. Generative design is expected to grow significantly, especially with the increasing adoption of advanced technologies such as cloud computing and AI, which enhance its capabilities. The expansion of generative design applications is fueling its integration into various sectors, from automotive to healthcare, where customized solutions and lightweight structures are critical.

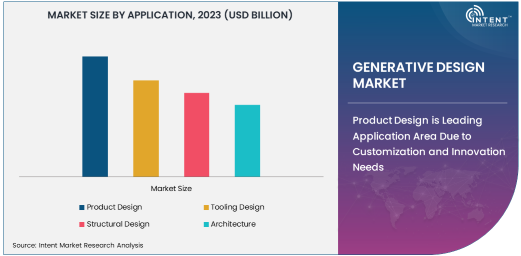

Product Design is Leading Application Area Due to Customization and Innovation Needs

Product design is the leading application area for generative design, largely driven by the increasing demand for customization and innovation. Designers and engineers in industries like automotive, aerospace, and consumer electronics are turning to generative design to create products that are more efficient, durable, and tailored to specific requirements. The technology helps accelerate the design process by offering a wide range of design alternatives that meet performance goals, material constraints, and manufacturing limits, which are otherwise time-consuming to explore manually.

The demand for personalized products, especially in the consumer electronics industry, is also driving the adoption of generative design in product design. This approach enables the creation of intricate, optimized structures that improve both functionality and aesthetic appeal. By streamlining the design process and reducing trial-and-error testing, generative design accelerates innovation, making it a key tool for companies looking to gain a competitive edge in product development.

Cloud-Based Generative Design is Fastest Growing Technology due to Scalability and Flexibility

Cloud-based generative design is the fastest-growing technology in the market, driven by the scalability and flexibility it offers. Unlike on-premise solutions, which require significant upfront investment in hardware and software infrastructure, cloud-based generative design solutions are delivered via a subscription-based model, offering users the ability to scale their design capabilities based on their needs. This technology enables real-time collaboration among designers, engineers, and other stakeholders, regardless of their location, which is particularly beneficial for global teams working on complex projects.

The shift toward cloud-based generative design is further accelerated by the increasing adoption of Industry 4.0, where smart manufacturing and data-driven design are central. Cloud solutions allow for faster processing and storage of large datasets, which are essential for the complex algorithms used in generative design. The ability to quickly iterate and optimize designs in the cloud also makes it easier for companies to reduce lead times, improve product quality, and lower costs, all of which are crucial factors in the highly competitive industries using generative design.

Automotive Industry Drives Demand for Generative Design Solutions

The automotive industry is the largest end-user of generative design solutions, owing to its need for lighter, stronger, and more efficient vehicle components. The use of generative design in automotive manufacturing allows for the development of optimized parts that are both lightweight and durable, which directly contributes to better fuel efficiency and performance. With the increasing focus on sustainability and reducing the carbon footprint of vehicles, generative design has become an invaluable tool in meeting regulatory standards while also improving the driving experience.

Generative design is applied in the creation of various automotive parts such as chassis, brackets, and structural components. Manufacturers like Ford and General Motors have been pioneers in adopting generative design to innovate their vehicle designs and improve production efficiency. As the automotive industry increasingly embraces electric vehicles (EVs) and autonomous driving technologies, generative design will play a pivotal role in developing new, high-performance, and energy-efficient vehicle components, further solidifying its importance in this sector.

North America Leads the Market Due to Technological Advancements and Industry Adoption

North America is the leading region in the generative design market, largely due to its technological advancements, early adoption of digital manufacturing techniques, and strong presence of key industry players. The region, particularly the United States, has witnessed widespread adoption of generative design solutions in industries such as automotive, aerospace, and healthcare, where innovation and product optimization are paramount. Major manufacturers in these industries are actively investing in generative design to enhance their product development processes and meet the growing demand for customized and efficient solutions.

The strong focus on digital transformation, combined with the region’s leading role in advanced manufacturing and the presence of key technology providers such as Autodesk, Dassault Systèmes, and Siemens, has enabled North America to dominate the generative design market. The region’s well-established research and development infrastructure further supports the growth of generative design technologies. As industries continue to adopt Industry 4.0 principles, North America is expected to remain at the forefront of generative design innovation and application.

Competitive Landscape and Leading Companies

The generative design market is highly competitive, with a range of established and emerging companies offering solutions to meet the growing demand for advanced product design. Key players in the market include Autodesk, Dassault Systèmes, Siemens, PTC, and Altair Engineering. These companies provide a diverse range of generative design software and platforms that cater to industries such as automotive, aerospace, and industrial manufacturing.

The competitive landscape is characterized by continuous technological innovation, as companies strive to enhance the capabilities of their generative design solutions, integrate AI and machine learning, and improve user experience. Strategic partnerships, collaborations, and acquisitions are common strategies used by companies to expand their product offerings and enter new markets. As the demand for generative design continues to grow, the market is expected to witness further advancements in cloud-based solutions, AI integration, and real-time collaboration tools, making competition more intense and fostering further innovation.

Recent Developments:

- In November 2024, Autodesk introduced new generative design features in AutoCAD, aimed at improving efficiency for engineers in the construction industry.

- In October 2024, PTC Inc. launched an upgraded version of its generative design software, enhancing its capabilities for additive manufacturing applications.

- In September 2024, Siemens AG unveiled a new generative design solution specifically designed for use in the aerospace and automotive sectors.

- In August 2024, Altair Engineering collaborated with a leading 3D printing firm to integrate generative design for additive manufacturing processes.

- In July 2024, nTopology raised funding to accelerate the development of its generative design platform, focusing on applications in advanced manufacturing and healthcare.

List of Leading Companies:

- Autodesk, Inc.

- Siemens AG

- PTC Inc.

- Dassault Systèmes

- Altair Engineering, Inc.

- nTopology, Inc.

- ANSYS, Inc.

- Hexagon AB

- Bentley Systems, Inc.

- Evolver, Inc.

- Materialise NV

- Frustum Inc.

- Dassault Systèmes

- Voxeljet AG

- Zebra Medical Vision

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 2.1 billion |

|

Forecasted Value (2030) |

USD 4.0 billion |

|

CAGR (2024 – 2030) |

9.7% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Generative Design Market By Application (Product Design, Tooling Design, Structural Design, Architecture), By Deployment Mode (Software as a Service (SaaS), License-based), By Technology (Cloud-based Generative Design, On-premise Generative Design), By End-User Industry (Automotive, Aerospace & Defense, Healthcare, Industrial Manufacturing, Consumer Electronics) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Autodesk, Inc., Siemens AG, PTC Inc., Dassault Systèmes, Altair Engineering, Inc., nTopology, Inc., ANSYS, Inc., Hexagon AB, Bentley Systems, Inc., Evolver, Inc., Materialise NV, Frustum Inc., Dassault Systèmes, Voxeljet AG, Zebra Medical Vision |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Generative Design Market, by Application (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Product Design |

|

4.2. Tooling Design |

|

4.3. Structural Design |

|

4.4. Architecture |

|

5. Generative Design Market, by Deployment Mode (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Software as a Service (SaaS) |

|

5.2. License-based |

|

6. Generative Design Market, by Technology (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Cloud-based Generative Design |

|

6.2. On-premise Generative Design |

|

7. Generative Design Market, by End-User Industry (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Automotive |

|

7.2. Aerospace & Defense |

|

7.3. Healthcare |

|

7.4. Industrial Manufacturing |

|

7.5. Consumer Electronics |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Generative Design Market, by Application |

|

8.2.7. North America Generative Design Market, by Deployment Mode |

|

8.2.8. North America Generative Design Market, by Technology |

|

8.2.9. North America Generative Design Market, by End-User Industry |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Generative Design Market, by Application |

|

8.2.10.1.2. US Generative Design Market, by Deployment Mode |

|

8.2.10.1.3. US Generative Design Market, by Technology |

|

8.2.10.1.4. US Generative Design Market, by End-User Industry |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Autodesk, Inc. |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Siemens AG |

|

10.3. PTC Inc. |

|

10.4. Dassault Systèmes |

|

10.5. Altair Engineering, Inc. |

|

10.6. nTopology, Inc. |

|

10.7. ANSYS, Inc. |

|

10.8. Hexagon AB |

|

10.9. Bentley Systems, Inc. |

|

10.10. Evolver, Inc. |

|

10.11. Materialise NV |

|

10.12. Frustum Inc. |

|

10.13. Dassault Systèmes |

|

10.14. Voxeljet AG |

|

10.15. Zebra Medical Vision |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Generative Design Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Generative Design Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Generative Design Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA