As per Intent Market Research, the Generative AI In Telecom Market was valued at USD 1.3 billion in 2024-e and will surpass USD 27.4 billion by 2030; growing at a CAGR of 54.7% during 2025 - 2030.

The generative AI market in telecom is rapidly growing as telecommunications companies seek to leverage advanced AI technologies for optimizing operations, enhancing customer experiences, and maintaining competitive advantage. From network optimization to predictive maintenance and personalized marketing, generative AI is proving to be a transformative force across the sector. As telecom companies move towards more automated, efficient, and data-driven operations, AI technologies such as machine learning, natural language processing (NLP), and computer vision are being increasingly integrated into their business models. In this dynamic market, key segments such as technology type, deployment type, application, and business size are evolving rapidly, driven by both large enterprises and innovative small and medium enterprises (SMEs).

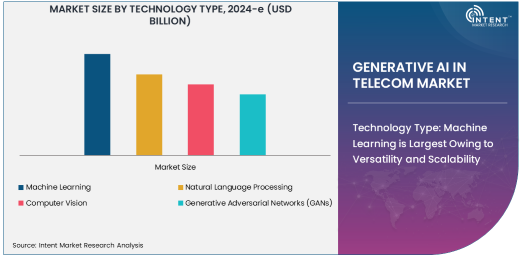

Technology Type: Machine Learning is Largest Owing to Versatility and Scalability

Machine learning (ML) remains the largest subsegment within the generative AI in telecom market, owing to its versatility in tackling a wide array of telecom challenges. ML algorithms enable telecom companies to extract valuable insights from large datasets, make real-time predictions, and optimize network performance. Whether it’s for enhancing customer support through chatbots, detecting fraud, or predicting network failures, machine learning is at the heart of these AI applications, providing the scalability and adaptability needed by telecom companies.

The ability to learn from historical data and improve over time has made machine learning indispensable in optimizing telecom operations. Its usage in areas such as network traffic management, customer behavior prediction, and predictive maintenance is expected to grow rapidly, as it helps companies enhance efficiency while lowering costs. Machine learning also allows telecom companies to adapt quickly to changing market conditions, further driving its widespread adoption in the sector.

Deployment Type: Cloud-Based Solutions Are Fastest Growing Due to Flexibility and Scalability

Cloud-based solutions are the fastest-growing subsegment in the generative AI in telecom market. The transition to cloud-based platforms offers telecom operators greater flexibility, scalability, and cost efficiency. By utilizing cloud infrastructure, telecom companies can deploy AI-driven solutions more easily and with fewer upfront costs compared to on-premise solutions. Additionally, cloud platforms enable real-time data analytics and enhanced collaboration across geographies, which is crucial in today’s fast-paced telecom environment.

As telecom companies strive for more agile and scalable operations, the cloud offers a compelling value proposition. Cloud-based solutions allow for quicker adoption of new technologies, including AI, and help telecom companies streamline network management and customer support. The growing demand for 5G networks, combined with the need for rapid data processing and network management, has further accelerated the adoption of cloud-based AI platforms in telecom. This shift is expected to continue as more telecom companies prioritize digital transformation and cloud migration.

Application: Network Optimization is Largest Owing to Industry Demand

Network optimization is the largest application of generative AI in the telecom market, driven by the increasing need for efficient network management. Telecom operators are under constant pressure to enhance the quality of service, reduce operational costs, and maximize the utilization of their network resources. AI-powered network optimization tools use data from various network touchpoints to predict traffic patterns, optimize bandwidth allocation, and ensure seamless communication services for end users.

The demand for higher network efficiency has intensified with the rise of 5G technology and the increasing reliance on mobile data. AI-driven network optimization helps telecom companies ensure smooth operations while reducing downtime, improving customer satisfaction, and avoiding unnecessary infrastructure investments. As the complexity of telecom networks grows, generative AI will continue to be central to optimizing resources, improving network reliability, and meeting the high expectations of customers in an increasingly digital world.

End-Use Industry: Telecom Service Providers Are Largest Users of AI Solutions

Telecom service providers are the largest end-users of generative AI in the telecom market. These companies are implementing AI-driven solutions to improve network performance, enhance customer service, and streamline operations. Telecom service providers use AI for various applications, including predictive maintenance, fraud detection, and network optimization, which are critical to maintaining high service levels and reducing operational costs.

With telecom service providers at the forefront of digital transformation, the adoption of generative AI technologies is accelerating. AI helps these companies make more accurate business forecasts, automate customer interactions through chatbots, and improve network efficiency. The growing demand for 5G services and the increasing complexity of telecom networks are further driving the use of generative AI in this segment, cementing telecom service providers as the largest consumer of AI technologies in the sector.

Solution Type: Software Solutions Are Dominating the Market

Software solutions are the dominant subsegment in the generative AI in telecom market, accounting for a substantial portion of the overall market share. AI-powered software platforms provide telecom companies with advanced tools for managing network operations, customer support, and fraud detection, among others. These platforms often combine machine learning, natural language processing, and data analytics to deliver more intelligent and automated solutions.

Telecom companies are increasingly adopting AI software to enhance their decision-making capabilities and improve operational efficiency. From predictive maintenance tools to real-time fraud detection systems, AI software is enabling telecom operators to address key industry challenges. As the demand for automation and enhanced data analysis grows, the market for AI software solutions in the telecom industry is expected to continue to expand, with more companies looking to streamline operations and improve customer experience through AI-driven tools.

Business Size: Large Enterprises are Leading the Adoption

Large enterprises are the primary drivers of generative AI adoption in the telecom market. With their substantial resources and complex operational needs, large telecom companies are more likely to invest in advanced AI technologies. These organizations are leveraging AI to optimize network performance, enhance customer support, and streamline operational processes across their global operations. The need for high-quality, scalable AI solutions makes large enterprises the largest adopters of generative AI in telecom.

As these enterprises continue to expand their digital transformation initiatives, the adoption of AI technologies such as machine learning, predictive maintenance, and network optimization is set to increase. Large telecom operators are also the first movers in embracing innovations such as 5G and AI-driven customer service models, making them key contributors to the growth of the generative AI market in telecom.

Region: North America is the Largest Market for Generative AI in Telecom

North America holds the largest share of the generative AI in telecom market, driven by the region’s robust technological infrastructure, advanced telecom services, and the presence of leading AI technology providers. The United States, in particular, has witnessed a significant rise in AI adoption across telecom operators, driven by the growing demand for 5G services, automation, and customer-centric solutions. North American telecom companies are keen to harness the power of AI to improve network management, customer service, and reduce operational costs.

The region is also home to some of the largest global technology companies, including IBM, Microsoft, and Google, who are supplying AI-driven solutions to telecom operators. As the demand for AI in telecom continues to rise, North America is expected to remain a leader in the market, with further growth anticipated from continued digital transformation and innovation in AI applications.

Competitive Landscape and Leading Companies

The competitive landscape in the generative AI in telecom market is characterized by the presence of both established telecom operators and global technology firms. Leading companies include IBM, Microsoft, Huawei, Nokia, and Ericsson, who are providing advanced AI-driven solutions for network optimization, customer service automation, and predictive maintenance. These companies are actively innovating and partnering with telecom operators to integrate AI technologies into their operations.

Smaller, specialized firms such as Ciena and Juniper Networks are also making significant strides in offering AI-powered network solutions. The competition is expected to intensify as telecom companies focus on reducing operational costs, improving service reliability, and enhancing customer experience through AI. The ongoing innovation and integration of AI technologies across telecom networks will continue to drive market dynamics, ensuring a highly competitive and rapidly evolving landscape.

Recent Developments:

- IBM Corporation launched an AI-driven predictive maintenance solution for telecom operators, designed to reduce network downtime and improve overall service reliability.

- Google Cloud expanded its partnership with telecom service providers, offering enhanced AI tools for network optimization and customer experience improvement.

- Ericsson introduced a new generative AI-powered tool to help telecom companies improve their 5G network management, optimizing bandwidth and network capacity.

- TCS (Tata Consultancy Services) announced a collaboration with a leading telecom provider to develop AI-powered chatbots that enhance customer service and reduce operational costs.

- Huawei Technologies unveiled a new cloud-based AI platform aimed at improving fraud detection and network security for telecom companies.

List of Leading Companies:

- IBM Corporation

- Microsoft Corporation

- Google Cloud

- Huawei Technologies

- Ericsson

- Cisco Systems

- Accenture

- TCS (Tata Consultancy Services)

- Infosys

- Capgemini

- AT&T

- Verizon Communications

- Nokia Corporation

- Oracle Corporation

- SAP SE

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 1.3 Million |

|

Forecasted Value (2030) |

USD 27.4 Million |

|

CAGR (2025 – 2030) |

54.7% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Generative AI in Telecom Market By Technology Type (Machine Learning, Natural Language Processing, Computer Vision, Generative Adversarial Networks), By Deployment Type (On-premise, Cloud-based), By Application (Network Optimization, Customer Support and Chatbots, Predictive Maintenance, Fraud Detection, Personalized Marketing, Demand Forecasting), By End-use Industry (Telecom Service Providers, Equipment Manufacturers, Network Operators), By Solution Type (Software, Services), By Business Size (Large Enterprises, SMEs) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

IBM Corporation, Microsoft Corporation, Google Cloud, Huawei Technologies, Ericsson, Cisco Systems, Accenture, TCS (Tata Consultancy Services), Infosys, Capgemini, AT&T, Verizon Communications, Nokia Corporation, Oracle Corporation, SAP SE |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Generative AI In Telecom Market, by Technology Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Machine Learning |

|

4.2. Natural Language Processing |

|

4.3. Computer Vision |

|

4.4. Generative Adversarial Networks (GANs) |

|

5. Generative AI In Telecom Market, by Deployment Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. On-premise |

|

5.2. Cloud-based |

|

6. Generative AI In Telecom Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Network Optimization |

|

6.2. Customer Support and Chatbots |

|

6.3. Predictive Maintenance |

|

6.4. Fraud Detection |

|

6.5. Personalized Marketing |

|

6.6. Demand Forecasting |

|

7. Generative AI In Telecom Market, by End-use Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Telecom Service Providers |

|

7.2. Equipment Manufacturers |

|

7.3. Network Operators |

|

8. Generative AI In Telecom Market, by Solution Type (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Software |

|

8.2. Services |

|

9. Generative AI In Telecom Market, by Business Size (Market Size & Forecast: USD Million, 2023 – 2030) |

|

9.1. Large Enterprises |

|

9.2. SMEs (Small and Medium Enterprises) |

|

10. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

10.1. Regional Overview |

|

10.2. North America |

|

10.2.1. Regional Trends & Growth Drivers |

|

10.2.2. Barriers & Challenges |

|

10.2.3. Opportunities |

|

10.2.4. Factor Impact Analysis |

|

10.2.5. Technology Trends |

|

10.2.6. North America Generative AI In Telecom Market, by Technology Type |

|

10.2.7. North America Generative AI In Telecom Market, by Deployment Type |

|

10.2.8. North America Generative AI In Telecom Market, by Application |

|

10.2.9. North America Generative AI In Telecom Market, by End-use Industry |

|

10.2.10. North America Generative AI In Telecom Market, by Solution Type |

|

10.2.11. North America Generative AI In Telecom Market, by Business Size |

|

10.2.12. By Country |

|

10.2.12.1. US |

|

10.2.12.1.1. US Generative AI In Telecom Market, by Technology Type |

|

10.2.12.1.2. US Generative AI In Telecom Market, by Deployment Type |

|

10.2.12.1.3. US Generative AI In Telecom Market, by Application |

|

10.2.12.1.4. US Generative AI In Telecom Market, by End-use Industry |

|

10.2.12.1.5. US Generative AI In Telecom Market, by Solution Type |

|

10.2.12.1.6. US Generative AI In Telecom Market, by Business Size |

|

10.2.12.2. Canada |

|

10.2.12.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

10.3. Europe |

|

10.4. Asia-Pacific |

|

10.5. Latin America |

|

10.6. Middle East & Africa |

|

11. Competitive Landscape |

|

11.1. Overview of the Key Players |

|

11.2. Competitive Ecosystem |

|

11.2.1. Level of Fragmentation |

|

11.2.2. Market Consolidation |

|

11.2.3. Product Innovation |

|

11.3. Company Share Analysis |

|

11.4. Company Benchmarking Matrix |

|

11.4.1. Strategic Overview |

|

11.4.2. Product Innovations |

|

11.5. Start-up Ecosystem |

|

11.6. Strategic Competitive Insights/ Customer Imperatives |

|

11.7. ESG Matrix/ Sustainability Matrix |

|

11.8. Manufacturing Network |

|

11.8.1. Locations |

|

11.8.2. Supply Chain and Logistics |

|

11.8.3. Product Flexibility/Customization |

|

11.8.4. Digital Transformation and Connectivity |

|

11.8.5. Environmental and Regulatory Compliance |

|

11.9. Technology Readiness Level Matrix |

|

11.10. Technology Maturity Curve |

|

11.11. Buying Criteria |

|

12. Company Profiles |

|

12.1. IBM Corporation |

|

12.1.1. Company Overview |

|

12.1.2. Company Financials |

|

12.1.3. Product/Service Portfolio |

|

12.1.4. Recent Developments |

|

12.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

12.2. Microsoft Corporation |

|

12.3. Google Cloud |

|

12.4. Huawei Technologies |

|

12.5. Ericsson |

|

12.6. Cisco Systems |

|

12.7. Accenture |

|

12.8. TCS (Tata Consultancy Services) |

|

12.9. Infosys |

|

12.10. Capgemini |

|

12.11. AT&T |

|

12.12. Verizon Communications |

|

12.13. Nokia Corporation |

|

12.14. Oracle Corporation |

|

12.15. SAP SE |

|

13. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Generative AI in Telecom Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Generative AI in Telecom Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Generative AI in Telecom Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA