As per Intent Market Research, the Generative AI In Pharmaceutical Market was valued at USD 2.4 billion in 2024-e and will surpass USD 53.7 billion by 2030; growing at a CAGR of 55.8% during 2025 - 2030.

The generative AI market in pharmaceuticals is experiencing rapid growth as organizations look to leverage artificial intelligence to expedite drug discovery, optimize clinical trials, and personalize medicine. AI-powered algorithms are helping pharmaceutical companies analyze complex biological data, predict drug efficacy, and enhance clinical trial designs. With a rising focus on precision medicine and improving patient outcomes, the integration of generative AI into pharmaceutical workflows is becoming increasingly essential. AI technologies enable pharma companies to simulate molecular behavior, accelerate drug design, and address the growing demand for personalized treatments.

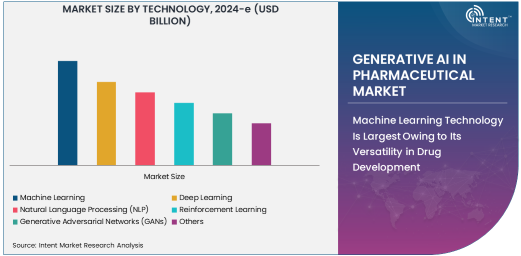

Machine Learning Technology Is Largest Owing to Its Versatility in Drug Development

Machine learning (ML) is the largest and most widely adopted AI technology in the pharmaceutical industry. Its ability to process and analyze large datasets, identify patterns, and improve over time makes it a core tool in drug discovery and development. Machine learning algorithms can predict drug efficacy, optimize clinical trial designs, and streamline the drug development process. As a result, pharmaceutical companies are investing heavily in machine learning to enhance productivity and reduce the time it takes to bring new drugs to market. The vast amount of biological data available today makes machine learning essential for transforming raw data into actionable insights that drive the creation of new therapeutic solutions.

Machine learning’s ability to make data-driven decisions based on patient demographics, genetic information, and medical histories also plays a crucial role in advancing personalized medicine. By accurately predicting individual responses to specific treatments, ML models help create tailored therapies, improving patient outcomes and reducing adverse effects. This broad applicability is what makes machine learning the dominant force in AI technologies for pharmaceutical applications, and its importance will continue to grow as data availability and computational power increase.

Drug Discovery Is Fastest Growing Application Due to Increased Demand for New Therapeutics

The drug discovery segment is the fastest growing application of generative AI in pharmaceuticals. AI’s ability to predict molecular interactions and simulate drug responses has transformed the drug discovery process. Traditional drug discovery methods are time-consuming and costly, often taking years before a potential candidate is identified. However, with AI, pharmaceutical companies can accelerate the discovery phase, identify promising compounds faster, and predict their effectiveness and toxicity. This has drastically reduced time and costs associated with early-stage drug development.

AI-powered generative models, especially deep learning algorithms, are able to generate novel molecular structures with the desired therapeutic properties. These algorithms can rapidly analyze chemical databases, search for patterns, and identify molecules that fit specific criteria. As a result, the pharmaceutical industry is seeing a surge in AI-based drug discovery platforms, making it an essential component of the pharmaceutical research process. The demand for new therapeutics, particularly in areas like oncology and rare diseases, is driving the rapid adoption of AI technologies in drug discovery, and this segment is expected to continue growing rapidly.

Pharmaceutical Companies Are Largest End-User Industry Owing to the Focus on Drug Development

Pharmaceutical companies are the largest end-user industry in the generative AI market within the pharmaceutical sector. These companies are increasingly incorporating AI technologies into various stages of the drug development process. With AI models capable of identifying potential drug candidates, predicting clinical trial outcomes, and optimizing manufacturing processes, pharmaceutical firms are using AI to enhance R&D efficiency and reduce costs. As the healthcare industry faces pressure to develop new treatments more rapidly, AI has become a key enabler for pharmaceutical companies aiming to stay competitive.

The large-scale data analytics capabilities of AI are crucial for pharmaceutical companies, as they rely on vast amounts of data for drug discovery, patient clinical trials, and post-market surveillance. By leveraging AI, these companies can process and analyze this data in real-time, making more informed decisions about drug candidates and clinical trial designs. As pharmaceutical companies strive to bring innovative therapies to market faster and more efficiently, the integration of AI technologies into their operations is a strategic necessity.

North America Is the Largest Region Due to Strong R&D and Technology Adoption

North America is the largest region in the generative AI in pharmaceutical market, driven by significant investments in research and development and widespread adoption of AI technologies in the healthcare sector. The region boasts several leading pharmaceutical companies and research institutions that are at the forefront of AI innovation. The United States, in particular, is home to major pharmaceutical firms, tech companies, and healthcare providers that are accelerating AI adoption to improve drug discovery and development processes. The presence of advanced infrastructure, high computational power, and large datasets further supports AI initiatives in North America.

In addition, North America benefits from favorable regulatory frameworks that encourage innovation in biotechnology and healthcare, which has spurred investments in AI-based drug development. As AI technologies continue to advance, North America is expected to maintain its leadership position in the pharmaceutical sector, with pharmaceutical companies, research institutions, and healthcare providers continuing to leverage generative AI for groundbreaking discoveries and personalized treatments.

Leading Companies Drive Innovation and Competitive Landscape

Leading companies in the generative AI in pharmaceutical market include industry giants such as IBM, Microsoft, Google DeepMind, and NVIDIA. These companies are actively developing AI-driven platforms and solutions for pharmaceutical applications, ranging from drug discovery to clinical trial optimization. For example, IBM’s Watson for Drug Discovery uses AI to analyze scientific literature and clinical trial data, helping researchers identify potential drug candidates. Google DeepMind’s AlphaFold, which predicts protein structures with remarkable accuracy, is another example of AI’s transformative role in pharmaceutical research.

The competitive landscape in the generative AI pharmaceutical market is characterized by significant collaboration between technology companies and pharmaceutical firms. Partnerships are essential for combining domain-specific expertise in drug development with cutting-edge AI technologies. In addition to global tech firms, pharmaceutical companies like Pfizer, Roche, and Moderna are investing heavily in AI to drive their drug discovery and development pipelines. As the market continues to grow, innovation and strategic collaborations between tech companies and pharmaceutical firms will play a pivotal role in shaping the future of drug development.

Recent Developments:

- Pfizer and IBM collaboration – Pfizer announced its partnership with IBM to integrate Generative AI into their drug discovery processes, aiming to enhance the speed and accuracy of identifying potential drug candidates.

- Google DeepMind's breakthrough – Google’s DeepMind AI system successfully predicted the structure of nearly every known protein, a significant development in pharmaceutical applications like drug discovery.

- Moderna AI platform – Moderna expanded its use of AI-driven platforms in its drug development pipeline, speeding up the creation of mRNA vaccines and therapeutics.

- Sanofi AI initiative – Sanofi invested in a new AI-focused platform aimed at revolutionizing early-stage drug discovery, which includes integrating AI models to predict patient responses.

- Microsoft and Merck M&A – Microsoft’s acquisition of an AI-driven biopharma company aims to further integrate machine learning and generative models into Merck's drug discovery and development processes, enhancing precision medicine capabilities.

List of Leading Companies:

- IBM

- Microsoft Corporation

- Google DeepMind

- NVIDIA Corporation

- Moderna Inc.

- Roche Pharmaceuticals

- Pfizer Inc.

- Sanofi S.A.

- GlaxoSmithKline plc

- AstraZeneca

- Merck & Co.

- Bayer AG

- Novartis International AG

- Johnson & Johnson

- AbbVie Inc.

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 2.4 Billion |

|

Forecasted Value (2030) |

USD 53.7 Billion |

|

CAGR (2025 – 2030) |

55.8% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Generative AI in Pharmaceutical Market By Technology (Machine Learning, Deep Learning, Natural Language Processing, Reinforcement Learning, Generative Adversarial Networks), By Application (Drug Discovery, Personalized Medicine, Drug Development Process Optimization, Clinical Trials, Drug Repurposing), By End-User Industry (Pharmaceutical Companies, Biotechnology Firms, Contract Research Organizations, Academic & Research Institutions, Healthcare Technology Companies) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

IBM, Microsoft Corporation, Google DeepMind, NVIDIA Corporation, Moderna Inc., Roche Pharmaceuticals, Pfizer Inc., Sanofi S.A., GlaxoSmithKline plc, AstraZeneca, Merck & Co., Bayer AG, Novartis International AG, Johnson & Johnson, AbbVie Inc. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Generative AI In Pharmaceutical Market, by Technology (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Machine Learning |

|

4.2. Deep Learning |

|

4.3. Natural Language Processing (NLP) |

|

4.4. Reinforcement Learning |

|

4.5. Generative Adversarial Networks (GANs) |

|

4.6. Others |

|

5. Generative AI In Pharmaceutical Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Drug Discovery |

|

5.2. Personalized Medicine |

|

5.3. Drug Development Process Optimization |

|

5.4. Clinical Trials |

|

5.5. Drug Repurposing |

|

5.6. Others |

|

6. Generative AI In Pharmaceutical Market, by End-User Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Pharmaceutical Companies |

|

6.2. Biotechnology Firms |

|

6.3. Contract Research Organizations (CROs) |

|

6.4. Academic & Research Institutions |

|

6.5. Healthcare Technology Companies |

|

6.6. Others |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Generative AI In Pharmaceutical Market, by Technology |

|

7.2.7. North America Generative AI In Pharmaceutical Market, by Application |

|

7.2.8. By Country |

|

7.2.8.1. US |

|

7.2.8.1.1. US Generative AI In Pharmaceutical Market, by Technology |

|

7.2.8.1.2. US Generative AI In Pharmaceutical Market, by Application |

|

7.2.8.2. Canada |

|

7.2.8.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. IBM |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Microsoft Corporation |

|

9.3. Google DeepMind |

|

9.4. NVIDIA Corporation |

|

9.5. Moderna Inc. |

|

9.6. Roche Pharmaceuticals |

|

9.7. Pfizer Inc. |

|

9.8. Sanofi S.A. |

|

9.9. GlaxoSmithKline plc |

|

9.10. AstraZeneca |

|

9.11. Merck & Co. |

|

9.12. Bayer AG |

|

9.13. Novartis International AG |

|

9.14. Johnson & Johnson |

|

9.15. AbbVie Inc. |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Generative AI in Pharmaceutical Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Generative AI in Pharmaceutical Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Generative AI in Pharmaceutical Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA