As per Intent Market Research, the Generative AI In Insurance Market was valued at USD 1.6 billion in 2024-e and will surpass USD 32.3 billion by 2030; growing at a CAGR of 54.0% during 2025 - 2030.

The integration of generative AI in the insurance industry has brought significant advancements across various segments, such as underwriting, fraud detection, claims processing, and customer service. With the growing reliance on data-driven insights and automation, AI technologies like machine learning, deep learning, and natural language processing (NLP) have become key enablers of efficiency and innovation in the sector. AI's potential in enhancing risk management, improving personalized offerings, and optimizing customer interactions has made it a crucial tool for insurance companies worldwide. As the industry continues to evolve, the adoption of AI is poised to further disrupt traditional processes and provide solutions to modern challenges, such as fraud and customer retention.

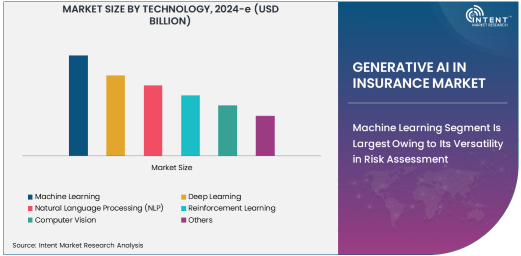

Machine Learning Segment Is Largest Owing to Its Versatility in Risk Assessment

Machine learning remains the largest subsegment in the generative AI technology landscape within insurance. Its ability to process large amounts of data and make predictions based on patterns has transformed the way insurers assess risk, underwrite policies, and manage claims. Machine learning algorithms are leveraged for risk prediction models, identifying trends in customer data, and streamlining the underwriting process. By analyzing historical data, machine learning can provide more accurate risk assessments, leading to better pricing models and more reliable decision-making in underwriting.

Additionally, machine learning plays a pivotal role in fraud detection, where AI models can detect unusual patterns and flag potentially fraudulent activities in real-time. This reduces the operational burden on human teams and accelerates claims processing. As the technology continues to evolve, its applications in the insurance sector are expanding, enhancing the industry’s ability to respond to complex and dynamic risk environments.

Claims Processing & Fraud Detection Is Fastest Growing Owing to Increasing Fraud Cases

Claims processing and fraud detection have emerged as one of the fastest-growing application areas of generative AI in insurance. The increasing complexity and frequency of fraudulent claims, coupled with the massive volume of claims data, have made it a significant challenge for insurers to manually review and assess claims. AI-powered systems, especially machine learning and deep learning, enable insurers to streamline this process by automatically validating claims and detecting discrepancies.

Fraudulent claims, which can cost the insurance industry billions of dollars annually, are now being addressed through AI’s ability to analyze patterns, identify red flags, and predict potentially fraudulent behavior based on historical data. These systems have significantly reduced false claims, improving profitability for insurers while ensuring a more accurate and fair claims process for policyholders. With the rise of digital transactions and a global push towards automation, claims processing and fraud detection will continue to see robust growth in the coming years.

Life Insurance Segment Is Largest Owing to Demand for Personalized Solutions

Among the various end-user industries, life insurance stands as the largest segment utilizing generative AI technologies. This growth can be attributed to the increasing demand for personalized insurance plans and better risk assessment capabilities. Life insurance companies are turning to AI to enhance their underwriting processes, offering more tailored policies that meet individual customer needs and preferences. By leveraging AI, insurers can analyze vast amounts of customer data, including health records and personal behavior patterns, to create dynamic, personalized life insurance offerings.

The ability to provide customized policies not only improves customer satisfaction but also strengthens customer retention in a highly competitive market. Life insurance is also increasingly leveraging AI for customer engagement, improving communication, and offering valuable insights throughout the policyholder’s journey. As the demand for personalized and affordable life insurance grows, AI’s role in transforming the sector continues to expand.

North America Region Is Largest Owing to Technological Advancements and Market Penetration

North America holds the largest share of the generative AI in the insurance market, driven primarily by technological advancements and the early adoption of AI technologies across industries. The region is home to some of the biggest insurance providers globally, and the widespread adoption of AI tools for underwriting, claims management, and customer service has paved the way for AI-driven transformation in the sector. Companies in the United States and Canada are leading the charge in AI integration, supported by robust digital infrastructure, a well-established tech ecosystem, and significant investments in AI research and development.

Furthermore, regulatory bodies in North America have begun to embrace AI innovations, providing a favorable environment for its growth. The insurance industry in this region is also highly competitive, pushing companies to leverage AI technologies to differentiate themselves in terms of customer experience and operational efficiency.

Competitive Landscape: Leading Companies and Their Strategic Initiatives

The generative AI in the insurance market is highly competitive, with major players focusing on enhancing their AI capabilities and providing innovative solutions to meet the evolving needs of insurers. Leading companies such as IBM, Microsoft, Google Cloud, and Accenture are driving AI advancements, offering solutions that help insurers automate underwriting, improve risk prediction, and enhance fraud detection. These companies have invested heavily in machine learning and AI research, helping to bring cutting-edge technologies to market.

In addition, several Insurtech companies like Lemonade and Zebra are also leveraging AI to disrupt traditional insurance models, offering fully automated claims processing and personalized pricing through data-driven insights. As the market continues to grow, mergers and acquisitions in the AI space are expected to increase, with companies seeking to enhance their AI portfolios and expand their customer base. Competitive pressure and regulatory considerations will push insurers to continue adopting and refining AI technologies, making it a central focus of industry transformation

List of Leading Companies:

- IBM

- Google Cloud

- Microsoft

- Amazon Web Services (AWS)

- Cognizant

- Accenture

- Oracle

- Capgemini

- DXC Technology

- Salesforce

- SAS Institute

- Infosys

- SAP

- TCS (Tata Consultancy Services)

- CureMetrix

Recent Developments:

- IBM and AXA Partnership: IBM's AI technology is being integrated into AXA’s operations to streamline claims processing and improve customer service with predictive analytics.

- Google Cloud Announces AI-Based Insurance Solutions: Google Cloud has partnered with several insurers to offer AI-driven tools aimed at improving risk assessment and underwriting capabilities.

- Accenture and Allianz Collaboration: Accenture and Allianz launched a new AI-driven solution designed to improve the efficiency and accuracy of insurance claims processing.

- Microsoft’s AI Expansion in Insurance: Microsoft launched a new AI product specifically for insurers, designed to optimize customer engagement and policyholder experience with personalized recommendations.

- Amazon Web Services (AWS) in Insurance: AWS has launched a new machine learning tool for the insurance industry to better analyze and predict claims data, further expanding its market presence in the sector.

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 1.6 Billion |

|

Forecasted Value (2030) |

USD 32.3 Billion |

|

CAGR (2025 – 2030) |

54.0% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Generative AI in Insurance Market by Technology (Machine Learning, Deep Learning, NLP, Reinforcement Learning, Computer Vision), Application (Risk Assessment & Underwriting, Claims Processing, Customer Service, Personalized Plans, Policy Administration), End-User Industry (Life, Health, Property & Casualty, Reinsurance, Commercial Insurance) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

IBM, Google Cloud, Microsoft, Amazon Web Services (AWS), Cognizant, Accenture, Oracle, Capgemini, DXC Technology, Salesforce, SAS Institute, Infosys, SAP, TCS (Tata Consultancy Services), CureMetrix |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Generative AI In Insurance Market, by Technology (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Machine Learning |

|

4.2. Deep Learning |

|

4.3. Natural Language Processing (NLP) |

|

4.4. Reinforcement Learning |

|

4.5. Computer Vision |

|

4.6. Others |

|

5. Generative AI In Insurance Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Risk Assessment & Underwriting |

|

5.2. Claims Processing & Fraud Detection |

|

5.3. Customer Service & Chatbots |

|

5.4. Personalized Insurance Plans |

|

5.5. Policy Administration & Management |

|

5.6. Others |

|

6. Generative AI In Insurance Market, by End-User Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Life Insurance |

|

6.2. Health Insurance |

|

6.3. Property & Casualty Insurance |

|

6.4. Reinsurance |

|

6.5. Commercial Insurance |

|

6.6. Others |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Generative AI In Insurance Market, by Technology |

|

7.2.7. North America Generative AI In Insurance Market, by Application |

|

7.2.8. By Country |

|

7.2.8.1. US |

|

7.2.8.1.1. US Generative AI In Insurance Market, by Technology |

|

7.2.8.1.2. US Generative AI In Insurance Market, by Application |

|

7.2.8.2. Canada |

|

7.2.8.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. IBM |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Google Cloud |

|

9.3. Microsoft |

|

9.4. Amazon Web Services (AWS) |

|

9.5. Cognizant |

|

9.6. Accenture |

|

9.7. Oracle |

|

9.8. Capgemini |

|

9.9. DXC Technology |

|

9.10. Salesforce |

|

9.11. SAS Institute |

|

9.12. Infosys |

|

9.13. SAP |

|

9.14. TCS (Tata Consultancy Services) |

|

9.15. CureMetrix |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Generative AI in Insurance Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Generative AI in Insurance Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Generative AI in Insurance Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA