As per Intent Market Research, the Generative AI in Chemical Market was valued at USD 0.3 billion in 2024-e and will surpass USD 1.3 billion by 2030; growing at a CAGR of 26.7% during 2025 - 2030.

The integration of generative AI in the chemical market is revolutionizing traditional operations, driving innovation, and enhancing efficiencies across applications, deployment modes, industries, and regions. By leveraging advanced algorithms, the industry is addressing complex challenges such as product design, process optimization, and sustainability. This market's growth is driven by increasing investments in AI-powered tools and a growing need for data-driven decision-making. Below is an analysis of the largest or fastest-growing subsegments within key market segments.

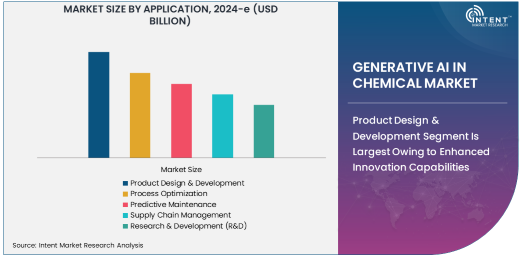

Product Design & Development Segment Is Largest Owing to Enhanced Innovation Capabilities

Generative AI has transformed product design and development in the chemical industry, enabling companies to innovate faster and more effectively. By using AI-driven algorithms, chemical manufacturers can simulate molecular interactions, predict properties of new materials, and identify optimal formulations. This has reduced development cycles, cut costs, and increased precision in designing advanced chemical solutions for various applications, including energy storage and lightweight materials.

The adoption of generative AI in this subsegment is fueled by its ability to streamline experimentation and prototype generation. Leading companies are integrating AI to address market demands for sustainable and high-performance materials, thus positioning this as the largest segment in the market.

Cloud-Based Deployment Mode Is Fastest Growing Owing to Scalability

Cloud-based generative AI solutions are gaining traction in the chemical market due to their scalability, cost-effectiveness, and accessibility. Cloud platforms allow companies to deploy AI algorithms without significant infrastructure investments, enabling seamless collaboration and data sharing.

The shift towards remote operations and real-time decision-making has driven the adoption of cloud-based solutions, making it the fastest-growing deployment mode. This trend is expected to continue as companies increasingly rely on cloud AI for innovation and efficiency.

Specialty Chemicals Segment Is Largest Owing to Tailored Solutions

Specialty chemicals, which cater to niche markets, benefit immensely from generative AI's ability to design customized formulations and improve product performance. AI-driven insights enable manufacturers to create high-value chemicals with specific properties for applications in coatings, adhesives, and performance materials.

This subsegment's dominance is attributed to its reliance on innovation and precision, which generative AI enhances significantly. Companies are leveraging AI tools to meet the growing demand for environmentally friendly and high-performance specialty chemicals.

Simulation & Modeling Segment Is Largest Owing to Real-Time Insights

Simulation and modeling are critical functionalities enabled by generative AI, allowing chemical companies to predict the behavior of complex systems. AI-powered simulations optimize reaction pathways, material properties, and production processes, reducing trial-and-error approaches.

This subsegment leads due to its applicability across various domains, from materials science to process engineering. The integration of AI into simulation tools has significantly enhanced efficiency, accuracy, and sustainability in chemical manufacturing.

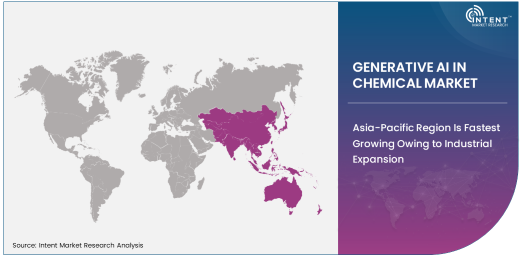

Asia-Pacific Region Is Fastest Growing Owing to Industrial Expansion

Asia-Pacific is the fastest-growing region in the generative AI in chemical market due to rapid industrialization, significant investments in AI technology, and the region's leadership in chemical manufacturing. Countries like China, India, and Japan are driving adoption through government initiatives and private sector investments.

The region's dynamic market landscape and growing demand for innovative and sustainable chemical solutions make it a key hub for AI-driven transformation. Companies are increasingly establishing R&D centers and collaborations in Asia-Pacific to leverage its growth potential.

Competitive Landscape and Leading Companies

The competitive landscape of the generative AI in chemical market is marked by the presence of key players such as BASF SE, Dow Inc., and SABIC, alongside emerging startups specializing in AI-driven solutions. Companies are focusing on partnerships, acquisitions, and technological advancements to enhance their market position.

Collaboration between chemical manufacturers and AI technology providers is intensifying, driving innovation and expanding application areas. As the market evolves, competitive dynamics will be shaped by companies' ability to leverage AI for sustainable growth and operational excellence.

Recent Developments:

- BASF SE expanded its AI-based digital solutions for chemical process optimization, launching a new platform designed to enhance R&D efficiency.

- Dow Chemical Company announced a strategic partnership with a leading AI tech company to integrate generative AI models for real-time predictive analytics in petrochemical production.

- Microsoft Corporation launched a new AI-powered tool designed for chemical companies to automate supply chain management, improving forecasting and demand planning.

- ExxonMobil Corporation recently introduced AI-driven solutions for predictive maintenance in its refinery operations, reducing downtime and improving operational efficiency.

- Honeywell International unveiled a new AI-powered system for chemical manufacturing plants aimed at improving safety and reducing energy consumption through process optimization.

List of Leading Companies:

- BASF SE

- Dow Inc.

- ExxonMobil Chemical Company

- SABIC

- LyondellBasell Industries

- Arkema

- Clariant

- Evonik Industries AG

- Mitsubishi Chemical Corporation

- DuPont

- Covestro AG

- Huntsman Corporation

- Eastman Chemical Company

- Solvay

- AI Chemist

Report Scope:

|

Report Features |

Description |

|

Market Size (2024-e) |

USD 0.3 Billion |

|

Forecasted Value (2030) |

USD 1.3 Billion |

|

CAGR (2025 – 2030) |

26.7% |

|

Base Year for Estimation |

2024-e |

|

Historic Year |

2023 |

|

Forecast Period |

2025 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Generative AI in Chemical Market by Application (Product Design & Development, Process Optimization, Predictive Maintenance, Supply Chain Management, Research & Development), By Deployment Mode (Cloud-Based, On-Premises), By End-Use Industry (Specialty Chemicals, Petrochemicals, Polymers & Plastics, Agrochemicals, Pharmaceuticals), By Functionality (Data Analysis & Pattern Recognition, Machine Learning Models, Language Processing & Reporting, Simulation & Modeling) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

BASF SE, Dow Inc., ExxonMobil Chemical Company, SABIC, LyondellBasell Industries, Arkema, Clariant, Evonik Industries AG, Mitsubishi Chemical Corporation, DuPont, Covestro AG, Huntsman Corporation, Eastman Chemical Company, Solvay, AI Chemist |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Generative AI In Chemical Market, by Application (Market Size & Forecast: USD Million, 2023 – 2030) |

|

4.1. Product Design & Development |

|

4.2. Process Optimization |

|

4.3. Predictive Maintenance |

|

4.4. Supply Chain Management |

|

4.5. Research & Development (R&D) |

|

5. Generative AI In Chemical Market, by Deployment Mode (Market Size & Forecast: USD Million, 2023 – 2030) |

|

5.1. Cloud-Based |

|

5.2. On-Premises |

|

6. Generative AI In Chemical Market, by End-Use Industry (Market Size & Forecast: USD Million, 2023 – 2030) |

|

6.1. Specialty Chemicals |

|

6.2. Petrochemicals |

|

6.3. Polymers & Plastics |

|

6.4. Agrochemicals |

|

6.5. Pharmaceuticals |

|

7. Generative AI In Chemical Market, by Functionality (Market Size & Forecast: USD Million, 2023 – 2030) |

|

7.1. Data Analysis & Pattern Recognition |

|

7.2. Machine Learning Models |

|

7.3. Language Processing & Reporting |

|

7.4. Simulation & Modeling |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2023 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Generative AI In Chemical Market, by Application |

|

8.2.7. North America Generative AI In Chemical Market, by Deployment Mode |

|

8.2.8. North America Generative AI In Chemical Market, by End-Use Industry |

|

8.2.9. North America Generative AI In Chemical Market, by Functionality |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Generative AI In Chemical Market, by Application |

|

8.2.10.1.2. US Generative AI In Chemical Market, by Deployment Mode |

|

8.2.10.1.3. US Generative AI In Chemical Market, by End-Use Industry |

|

8.2.10.1.4. US Generative AI In Chemical Market, by Functionality |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. BASF SE |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Dow Inc. |

|

10.3. ExxonMobil Chemical Company |

|

10.4. SABIC |

|

10.5. LyondellBasell Industries |

|

10.6. Arkema |

|

10.7. Clariant |

|

10.8. Evonik Industries AG |

|

10.9. Mitsubishi Chemical Corporation |

|

10.10. DuPont |

|

10.11. Covestro AG |

|

10.12. Huntsman Corporation |

|

10.13. Eastman Chemical Company |

|

10.14. Solvay |

|

10.15. AI Chemist |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Generative AI in Chemical Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Generative AI in Chemical Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Generative AI in Chemical Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA