As per Intent Market Research, the Gas Fired Food Processing Boiler Market was valued at USD 0.9 billion in 2023 and will surpass USD 1.4 billion by 2030; growing at a CAGR of 5.4% during 2024 - 2030.

The gas-fired food processing boiler market has been witnessing steady growth due to the increasing demand for energy-efficient, reliable, and eco-friendly steam and hot water solutions within the food and beverage industry. Boilers play a critical role in food processing, providing the necessary steam for various applications such as cooking, cleaning, and packaging. The need for high-quality food products, coupled with a growing focus on sustainability, has prompted manufacturers to adopt gas-fired boilers, which are more environmentally friendly than their oil or coal-fired counterparts.

As the food processing sector continues to expand, particularly in emerging markets, the demand for gas-fired boilers that can efficiently handle large-scale operations has also risen. The shift towards natural gas as a preferred fuel due to its cost-efficiency, reduced emissions, and availability is further fueling the growth of this market. Food processing companies are increasingly investing in advanced technologies such as condensing boilers, which offer higher efficiency and lower operational costs, making them more appealing for long-term use in the food and beverage industry.

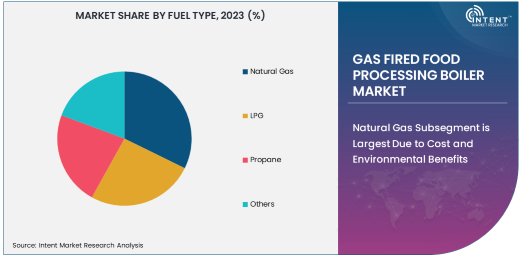

Natural Gas Subsegment is Largest Due to Cost and Environmental Benefits

Natural gas is the dominant fuel type in the gas-fired food processing boiler market, primarily due to its cost-effectiveness, widespread availability, and lower environmental impact compared to other fuel types such as LPG or propane. As food processing companies are under increasing pressure to reduce energy costs and minimize their carbon footprints, natural gas has become the fuel of choice for industrial boilers. Compared to LPG and propane, natural gas is more affordable and produces fewer greenhouse gas emissions, making it the most sustainable option for food processing operations that require constant steam generation.

Furthermore, natural gas-fired boilers benefit from a well-established infrastructure for distribution, which ensures a steady supply and reduces the risk of operational disruptions. This, combined with natural gas’s lower cost relative to oil and its efficiency in terms of energy output, has made it the preferred fuel type in the market, particularly in large-scale operations where fuel efficiency is a significant consideration. The continued global push towards sustainability and reducing energy consumption is expected to maintain natural gas's dominance in the food processing boiler market.

Fire Tube Boilers Lead in Popularity Due to Simplicity and Reliability

Fire tube boilers are the most commonly used type in the gas-fired food processing boiler market, driven by their simplicity, reliability, and cost-effectiveness. These boilers are particularly popular in small to medium-sized food processing operations due to their ease of maintenance, compact design, and ability to efficiently generate the required steam. Fire tube boilers operate by passing hot gases from the combustion process through tubes that are submerged in water, allowing for efficient heat transfer.

The demand for fire tube boilers is especially high in meat and poultry processing, dairy processing, and bakery applications, where continuous steam is necessary for cooking, sterilization, and cleaning purposes. Due to their straightforward design and relatively low operational costs, fire tube boilers are ideal for facilities looking for reliable and cost-effective steam generation solutions. As the food processing industry seeks more efficient and scalable systems, fire tube boilers continue to be a significant segment within the market, particularly for medium-capacity food processing operations.

1-5 MW Capacity Subsegment is Largest Due to Versatility

The 1-5 MW capacity range is the largest subsegment in the gas-fired food processing boiler market, as it caters to the needs of medium-sized food processing plants. Boilers in this capacity range provide an optimal balance between steam output and operational cost, making them a popular choice among food processors that require consistent and reliable steam without the need for extremely large-scale systems. These boilers are commonly used in applications such as dairy processing, meat processing, and beverage production, where steam is required for various stages of production.

This capacity range is ideal for mid-sized food and beverage companies that do not require the vast amounts of steam associated with larger plants, yet still need a reliable and energy-efficient solution. The 1-5 MW boilers are versatile, capable of handling the varying demands of food processing operations, making them a practical choice for a broad range of applications. As food processing operations continue to grow and scale, the demand for boilers in this capacity range is expected to remain strong, offering a cost-effective solution for medium-scale operations.

Beverage Production is the Fastest Growing Application Due to Industry Expansion

Beverage production is the fastest-growing application segment in the gas-fired food processing boiler market, driven by the increasing global demand for bottled and canned beverages, especially in developing markets. The need for efficient steam generation in beverage production processes—such as brewing, pasteurization, and sterilization—is pushing the demand for reliable gas-fired boilers. Boilers play a critical role in these processes, providing the necessary heat to ensure product quality and safety.

As beverage consumption continues to rise worldwide, particularly in emerging economies where the market for packaged beverages is expanding rapidly, the demand for boilers in this segment is expected to grow significantly. The beverage industry is also witnessing a shift towards more energy-efficient and environmentally friendly solutions, driving the adoption of high-efficiency gas-fired boilers. Condensing boilers, which offer increased energy efficiency, are becoming particularly popular in the beverage sector as companies seek to reduce energy costs and minimize their environmental impact.

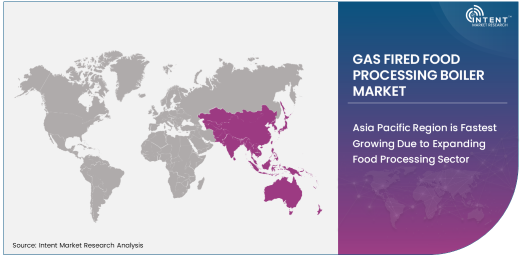

Asia Pacific Region is Fastest Growing Due to Expanding Food Processing Sector

The Asia Pacific region is the fastest-growing market for gas-fired food processing boilers, driven by rapid industrialization, urbanization, and a growing food and beverage sector. As countries like China, India, and Southeast Asian nations experience an increase in food processing activities to meet rising consumer demand, the adoption of gas-fired boilers is also on the rise. The region's expanding population and growing middle class are contributing to an increased need for packaged food and beverages, which in turn drives the demand for more efficient and sustainable boiler systems.

In addition to economic growth, governments in the Asia Pacific region are focusing on improving energy efficiency and promoting cleaner technologies, which further supports the adoption of gas-fired boilers. With natural gas being relatively more affordable and accessible in many parts of the region, its adoption for food processing applications is expected to continue growing. As Asia Pacific becomes a key hub for global food processing operations, the demand for advanced, energy-efficient gas-fired boilers will remain robust, positioning the region as a major player in the market.

Leading Companies and Competitive Landscape

The gas-fired food processing boiler market is highly competitive, with key players offering a wide range of products to meet the diverse needs of the food processing industry. Prominent companies in the market include Bosch Thermotechnology, Babcock & Wilcox, Fulton Companies, and Miura Co. These companies are known for their innovative boiler solutions, particularly those that focus on improving energy efficiency and reducing environmental impact. Leading manufacturers are also investing heavily in R&D to develop high-efficiency, low-emission boilers that meet the increasing demand for sustainable energy solutions in the food processing sector.

The competitive landscape in the market is driven by technological advancements, product innovations, and strategic partnerships. Companies are increasingly focusing on expanding their product portfolios to cater to various capacity requirements and application types. In addition to global players, regional manufacturers are also capitalizing on local market demands, offering tailored solutions that meet specific regulatory requirements and energy efficiency standards. As the market continues to grow, competition will intensify, with companies striving to provide the most efficient, cost-effective, and eco-friendly solutions to their clients.

Recent Developments:

- In December 2024, Bosch Thermotechnology launched a new line of high-efficiency gas-fired condensing boilers for the food processing industry, designed to reduce energy consumption and emissions.

- In November 2024, Viessmann Group expanded its product range with advanced gas-fired boilers, incorporating smart control features to optimize heating processes in food production facilities.

- In October 2024, Fulton Boiler Works introduced a new series of fire tube boilers for food processing, focused on increasing thermal efficiency and reducing operational downtime.

- In September 2024, Thermax Limited launched an innovative gas-fired boiler that combines water tube and condensing technology to cater to the food industry's need for sustainable energy solutions.

- In August 2024, Aalborg Engineering unveiled a range of low-pressure gas-fired boilers specifically designed for the beverage production and canning industries, providing cost-effective and efficient heating solutions.

List of Leading Companies:

- Bosch Thermotechnology

- Viessmann Group

- Fulton Boiler Works

- Cleaver-Brooks

- Babcock & Wilcox Enterprises

- Mitsubishi Heavy Industries

- Hurst Boiler & Welding Co., Inc.

- Thermax Limited

- Aalborg Engineering

- Laars Heating Systems

- Zurn Industries, Inc.

- MHI Group

- Ariston Thermo Group

- Raypak, Inc.

- Rheem Manufacturing Company

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 0.9 billion |

|

Forecasted Value (2030) |

USD 1.4 billion |

|

CAGR (2024 – 2030) |

5.4% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Gas Fired Food Processing Boiler Market By Fuel Type (Natural Gas, LPG, Propane), By Boiler Type (Fire Tube Boilers, Water Tube Boilers, Condensing Boilers), By Application (Meat & Poultry Processing, Dairy Processing, Bakery & Confectionery, Beverage Production, Canning & Packaging), By Capacity (Below 1 MW, 1-5 MW, 5-10 MW, Above 10 MW) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Bosch Thermotechnology, Viessmann Group, Fulton Boiler Works, Cleaver-Brooks, Babcock & Wilcox Enterprises, Mitsubishi Heavy Industries, Hurst Boiler & Welding Co., Inc., Thermax Limited, Aalborg Engineering, Laars Heating Systems, Zurn Industries, Inc., MHI Group, Ariston Thermo Group, Raypak, Inc., Rheem Manufacturing Company |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Gas Fired Food Processing Boiler Market, by Fuel Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Natural Gas |

|

4.2. LPG |

|

4.3. Propane |

|

4.4. Others |

|

5. Gas Fired Food Processing Boiler Market, by Boiler Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Fire Tube Boilers |

|

5.2. Water Tube Boilers |

|

5.3. Condensing Boilers |

|

6. Gas Fired Food Processing Boiler Market, by Application (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Meat & Poultry Processing |

|

6.2. Dairy Processing |

|

6.3. Bakery & Confectionery |

|

6.4. Beverage Production |

|

6.5. Canning & Packaging |

|

6.6. Others |

|

7. Gas Fired Food Processing Boiler Market, by Capacity (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Below 1 MW |

|

7.2. 1-5 MW |

|

7.3. 5-10 MW |

|

7.4. Above 10 MW |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Gas Fired Food Processing Boiler Market, by Fuel Type |

|

8.2.7. North America Gas Fired Food Processing Boiler Market, by Boiler Type |

|

8.2.8. North America Gas Fired Food Processing Boiler Market, by Application |

|

8.2.9. North America Gas Fired Food Processing Boiler Market, by Capacity |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Gas Fired Food Processing Boiler Market, by Fuel Type |

|

8.2.10.1.2. US Gas Fired Food Processing Boiler Market, by Boiler Type |

|

8.2.10.1.3. US Gas Fired Food Processing Boiler Market, by Application |

|

8.2.10.1.4. US Gas Fired Food Processing Boiler Market, by Capacity |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Bosch Thermotechnology |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Viessmann Group |

|

10.3. Fulton Boiler Works |

|

10.4. Cleaver-Brooks |

|

10.5. Babcock & Wilcox Enterprises |

|

10.6. Mitsubishi Heavy Industries |

|

10.7. Hurst Boiler & Welding Co., Inc. |

|

10.8. Thermax Limited |

|

10.9. Aalborg Engineering |

|

10.10. Laars Heating Systems |

|

10.11. Zurn Industries, Inc. |

|

10.12. MHI Group |

|

10.13. Ariston Thermo Group |

|

10.14. Raypak, Inc. |

|

10.15. Rheem Manufacturing Company |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Gas Fired Food Processing Boiler Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Gas Fired Food Processing Boiler Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Gas Fired Food Processing Boiler Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA