As per Intent Market Research, the Food Traceability Market was valued at USD 15.5 Billion in 2023 and will surpass USD 28.9 Billion by 2030; growing at a CAGR of 9.3% during 2024 - 2030.

The food traceability market has become a pivotal element in ensuring food safety, enhancing transparency, and improving efficiency across the global food supply chain. As consumer awareness around food safety, origin, and sustainability increases, businesses are seeking solutions to monitor and track the journey of food products from farm to table. The rise in foodborne illness outbreaks and regulatory pressures are further driving the adoption of advanced traceability technologies. By leveraging real-time tracking systems, the food traceability market plays a vital role in reducing waste, increasing operational efficiency, and providing greater transparency to consumers. This market is expected to grow significantly as food safety regulations become stricter, and consumer demand for safe, authentic food continues to rise.

The adoption of innovative technologies such as Radio Frequency Identification (RFID), barcodes, and GPS-based systems is transforming food traceability. These technologies help ensure the authenticity and safety of food products and enable businesses to respond swiftly to recalls or contamination events. Furthermore, as companies across the food industry realize the advantages of implementing traceability systems—such as improved operational efficiency, reduced fraud, and enhanced consumer confidence—the demand for these solutions is projected to increase over the coming years.

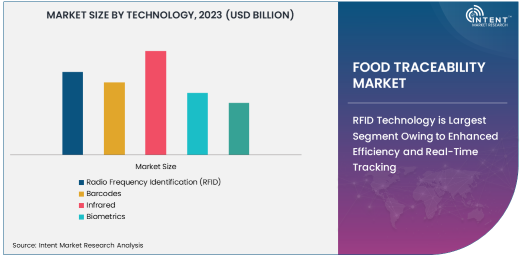

RFID Technology is Largest Segment Owing to Enhanced Efficiency and Real-Time Tracking

Radio Frequency Identification (RFID) is the largest segment in the food traceability market due to its ability to provide highly efficient and accurate tracking throughout the food supply chain. RFID systems use electromagnetic fields to track food products in real time, providing businesses with greater visibility and control over their inventory. Unlike barcodes, RFID tags do not require direct line-of-sight scanning and can store a larger amount of information, making them ideal for fast-moving and high-volume food sectors.

RFID is especially valuable in industries such as meat, dairy, and seafood, where traceability is critical due to stringent food safety standards and regulations. With RFID, producers, processors, and retailers can trace the journey of food products from farm to consumer, ensuring quality and safety. The increasing focus on improving food safety, reducing food fraud, and ensuring supply chain transparency has driven the widespread adoption of RFID technology, making it the dominant choice in the market.

Barcodes Segment is Fastest Growing Owing to Cost-Effectiveness and Ease of Use

While RFID dominates in terms of market share, the barcodes segment is the fastest growing within the food traceability market. Barcodes are widely used across the food industry for their simplicity, affordability, and ease of integration. Barcodes require a line-of-sight scan but offer a cost-effective solution for businesses looking to implement traceability without a significant upfront investment. With increasing demand for transparency in the food supply chain, barcodes are gaining popularity, especially among small and medium-sized food producers.

Barcodes are particularly prevalent in the retail sector, where packaged food products are labeled for tracking from the manufacturer to the consumer. The adoption of barcode-based solutions is growing rapidly as more retailers seek to enhance food safety practices, meet regulatory requirements, and offer consumers the ability to access product information quickly and efficiently. With further advancements in 2D barcodes and QR codes, the barcodes segment is expected to continue its rapid growth in the coming years.

Fresh Produce & Seeds Segment is Largest Application Owing to Consumer Demand for Safe, Organic Food

The fresh produce & seeds segment represents the largest application for food traceability technologies, driven by rising consumer demand for fresh, organic, and locally grown food products. The need to ensure the origin and safety of fresh produce has become a top priority for growers, distributors, and retailers. Traceability systems help to manage food safety risks, mitigate contamination events, and improve the overall quality of produce. In addition, traceability solutions help to maintain sustainable practices, such as minimizing food waste and ensuring the integrity of organic certifications.

Fresh produce is highly susceptible to contamination, which makes it imperative to have reliable traceability systems in place. Technologies like RFID and barcodes are being used to track the movement of produce from farms to distribution centers, ensuring compliance with food safety regulations. With growing concerns over foodborne illnesses and a shift towards more sustainable sourcing practices, the fresh produce & seeds segment is expected to continue to lead the way in food traceability adoption.

Retail Industry is Largest End-Use Industry Owing to Consumer Expectations for Transparency

The retail industry is the largest end-user of food traceability technologies, driven by increasing consumer expectations for transparency and food safety. Retailers are under constant pressure to ensure that the food they sell meets high safety standards and is sourced from reliable, ethical producers. Traceability systems, including RFID and barcodes, help retailers provide detailed information about the origin and journey of food products, from production to point-of-sale.

Consumers today are more conscious of where their food comes from and how it is handled, and this trend is reshaping the retail landscape. With food recalls, sustainability concerns, and ethical sourcing becoming major issues, retailers are increasingly turning to traceability systems to meet these challenges. These systems enable retailers to build consumer trust, streamline operations, and ensure compliance with food safety regulations. As consumer demand for food transparency continues to rise, the retail sector will remain the largest end-user of food traceability technologies.

North America is Largest Region Owing to Strong Regulatory Framework and Technological Adoption

North America is the largest region in the food traceability market, driven by the strong regulatory framework and widespread adoption of advanced technologies. In the United States, food safety regulations, including the Food Safety Modernization Act (FSMA), require food companies to implement traceability systems to ensure product safety and quality. Additionally, the region is home to many leading food producers, retailers, and technology providers, which accelerates the adoption of food traceability solutions.

North America's advanced infrastructure and technological capabilities have contributed to its dominant position in the global market. The region's high level of regulatory oversight and consumer demand for safe, high-quality food products have made food traceability a priority. With ongoing efforts to enhance food safety, reduce food fraud, and improve supply chain transparency, North America will continue to lead the market in the coming years.

Competitive Landscape and Leading Companies

The food traceability market is highly competitive, with a wide range of companies offering innovative solutions for the food industry. Key players include Zebra Technologies, Honeywell International Inc., Tetra Pak, IBM Corporation, and Oracle Corporation. These companies are focusing on product innovation, such as the integration of blockchain technology, real-time monitoring, and data analytics, to provide enhanced food traceability solutions. Strategic partnerships and acquisitions are also common in the industry as companies seek to expand their product offerings and market presence.

The competitive landscape is expected to remain dynamic, with both established players and emerging startups driving innovation. As the demand for food traceability technologies continues to grow, leading companies will focus on developing solutions that not only meet regulatory requirements but also enhance operational efficiency, reduce costs, and improve the overall food safety and transparency experience for consumers.

Recent Developments:

- The FDA introduced new tools and FAQs to help stakeholders comply with the Food Traceability Rule, effective in 2026.

- ReposiTrak added 50 new produce suppliers to its Traceability Network, enhancing compliance with FDA regulations.

- FoodLogiQ has partnered with Walmart to implement a blockchain-based traceability solution across its supply chain.

- IBM and Maersk launched a new blockchain platform aimed at improving food traceability and reducing fraud in the supply chain.

- GS1 has updated its global standards for food traceability, facilitating improved product tracking and transparency across the food supply chain.

List of Leading Companies:

- AGRIVI

- Aptean

- Bumble Bee Foods LLC

- C.H. Robinson Worldwide, Inc.

- Cognex Corporation

- Dock Labs AG

- Honeywell International Inc.

- iFooDS

- Optel Group

- SAP

- Stevens Traceability Systems Ltd

- Trace Food

- TraceX Technologies Private Limited

- Trustwell

- Zebra Technologies Corp.

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 15.5 Billion |

|

Forecasted Value (2030) |

USD 28.9 Billion |

|

CAGR (2024 – 2030) |

9.3% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Food Traceability Market by Technology (Radio Frequency Identification [RFID], Barcodes, Infrared, Biometrics, Global Positioning Systems [GPS]), by Application (Meat & Livestock, Fresh Produce & Seeds, Dairy, Beverages, Fisheries), by End-Use Industry (Retail, Foodservice, Healthcare, Agriculture, Logistics and Transportation) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

AGRIVI, Aptean, Bumble Bee Foods LLC, C.H. Robinson Worldwide, Inc., Cognex Corporation, Dock Labs AG, iFooDS, Optel Group, SAP, Stevens Traceability Systems Ltd, Trace Food, TraceX Technologies Private Limited and Zebra Technologies Corp. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Food Traceability Market, by Technology (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Radio Frequency Identification (RFID) |

|

4.2. Barcodes |

|

4.3. Infrared |

|

4.4. Biometrics |

|

4.5. Global Positioning Systems (GPS) |

|

5. Food Traceability Market, by Application (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Meat & Livestock |

|

5.2. Fresh Produce & Seeds |

|

5.3. Dairy |

|

5.4. Beverages |

|

5.5. Fisheries |

|

5.6. Others |

|

6. Food Traceability Market, by End-Use Industry (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Retail |

|

6.2. Foodservice |

|

6.3. Healthcare |

|

6.4. Agriculture |

|

6.5. Logistics and Transportation |

|

7. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Regional Overview |

|

7.2. North America |

|

7.2.1. Regional Trends & Growth Drivers |

|

7.2.2. Barriers & Challenges |

|

7.2.3. Opportunities |

|

7.2.4. Factor Impact Analysis |

|

7.2.5. Technology Trends |

|

7.2.6. North America Food Traceability Market, by Technology |

|

7.2.7. North America Food Traceability Market, by Application |

|

7.2.8. North America Food Traceability Market, by End-Use Industry |

|

7.2.9. By Country |

|

7.2.9.1. US |

|

7.2.9.1.1. US Food Traceability Market, by Technology |

|

7.2.9.1.2. US Food Traceability Market, by Application |

|

7.2.9.1.3. US Food Traceability Market, by End-Use Industry |

|

7.2.9.2. Canada |

|

7.2.9.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

7.3. Europe |

|

7.4. Asia-Pacific |

|

7.5. Latin America |

|

7.6. Middle East & Africa |

|

8. Competitive Landscape |

|

8.1. Overview of the Key Players |

|

8.2. Competitive Ecosystem |

|

8.2.1. Level of Fragmentation |

|

8.2.2. Market Consolidation |

|

8.2.3. Product Innovation |

|

8.3. Company Share Analysis |

|

8.4. Company Benchmarking Matrix |

|

8.4.1. Strategic Overview |

|

8.4.2. Product Innovations |

|

8.5. Start-up Ecosystem |

|

8.6. Strategic Competitive Insights/ Customer Imperatives |

|

8.7. ESG Matrix/ Sustainability Matrix |

|

8.8. Manufacturing Network |

|

8.8.1. Locations |

|

8.8.2. Supply Chain and Logistics |

|

8.8.3. Product Flexibility/Customization |

|

8.8.4. Digital Transformation and Connectivity |

|

8.8.5. Environmental and Regulatory Compliance |

|

8.9. Technology Readiness Level Matrix |

|

8.10. Technology Maturity Curve |

|

8.11. Buying Criteria |

|

9. Company Profiles |

|

9.1. AGRIVI |

|

9.1.1. Company Overview |

|

9.1.2. Company Financials |

|

9.1.3. Product/Service Portfolio |

|

9.1.4. Recent Developments |

|

9.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

9.2. Aptean |

|

9.3. Bumble Bee Foods LLC |

|

9.4. C.H. Robinson Worldwide, Inc. |

|

9.5. Cognex Corporation |

|

9.6. Dock Labs AG |

|

9.7. Honeywell International Inc. |

|

9.8. iFooDS |

|

9.9. Optel Group |

|

9.10. SAP |

|

9.11. Stevens Traceability Systems Ltd |

|

9.12. Trace Food |

|

9.13. TraceX Technologies Private Limited |

|

9.14. Trustwell |

|

9.15. Zebra Technologies Corp. |

|

10. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Food Traceability Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Food Traceability Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Food Traceability Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA