As per Intent Market Research, the Food Release Agents Market was valued at USD 1.4 billion in 2023 and will surpass USD 2.2 billion by 2030; growing at a CAGR of 7.0% during 2024 - 2030.

The food release agents market is experiencing notable growth, driven by increasing demand for efficient and high-quality food production solutions. Release agents, which prevent food products from sticking to surfaces during processing, play a crucial role in bakery, confectionery, and processed food manufacturing. With advancements in food processing technology and the growing preference for clean-label and plant-based ingredients, the market is evolving to meet diverse industrial needs.

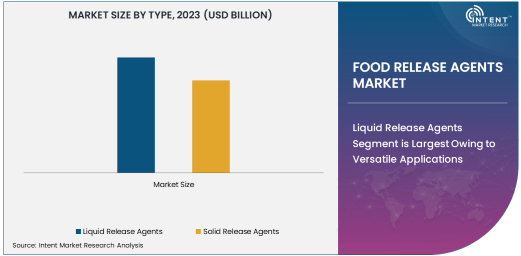

Liquid Release Agents Segment is Largest Owing to Versatile Applications

The liquid release agents segment dominates the market due to its wide-ranging applications and superior performance in preventing sticking during food processing. These agents are extensively used in bakery and confectionery products, offering precise application and consistent results.

Liquid release agents are preferred for their ease of use and uniform coverage, making them suitable for large-scale production environments. Their ability to work effectively with different formulations, including non-stick baking molds and trays, has driven their adoption among food manufacturers. The segment's growth is further supported by the increasing demand for premium-quality baked goods and processed foods.

Lecithin Segment is Fastest Growing Owing to Its Natural and Functional Benefits

Lecithin, derived from soy or sunflower, is the fastest-growing ingredient type in the food release agents market. Its natural origin and multifunctional properties, including emulsification and release capabilities, align with the rising demand for clean-label and allergen-free products.

The shift towards plant-based ingredients in food manufacturing has bolstered lecithin's popularity. It is particularly favored in the bakery industry for its ability to improve texture and prevent sticking without altering the taste or appearance of final products. As consumers prioritize transparency and sustainability, the lecithin segment is poised for accelerated growth.

Bakery and Confectionery Segment is Largest Owing to High Usage in Baked Goods

The bakery and confectionery segment holds the largest share in the food release agents market. These agents are essential for ensuring the smooth release of cakes, cookies, pastries, and other baked products from molds and trays, thereby maintaining their structural integrity and visual appeal.

As the global bakery industry grows, fueled by consumer demand for artisanal and premium baked goods, the need for reliable release agents has surged. Innovations in non-stick technologies and the development of allergen-free solutions are further driving growth in this segment, catering to evolving consumer preferences.

Processed Foods Segment is Fastest Growing Owing to Expanding Ready-to-Eat Market

The processed foods segment is the fastest-growing application area for food release agents. As consumers increasingly opt for convenience foods, manufacturers are adopting advanced release agents to streamline production and improve product quality.

From frozen meals to snack foods, release agents ensure consistent product shaping and surface finish, enhancing the overall appeal. The segment’s growth is supported by innovations in packaging and processing technologies, as well as the global trend towards ready-to-eat and minimally processed food options.

Food Manufacturers Segment is Largest Owing to High Production Volumes

Among end-user industries, food manufacturers represent the largest segment in the food release agents market. The reliance on release agents for mass production of bakery goods, confectionery items, and processed foods underscores their critical role in the industry.

Manufacturers benefit from the operational efficiency and cost savings provided by effective release agents, which minimize waste and reduce cleaning requirements. As food production scales up to meet global demand, the dominance of this segment is expected to persist.

North America Leads Owing to Advanced Food Processing Industry

North America holds the largest share of the food release agents market, driven by its well-established food processing and bakery industries. The region's stringent food safety regulations and emphasis on product quality have spurred the adoption of high-performance release agents.

Consumer demand for premium baked goods and processed foods, coupled with the prevalence of large-scale food manufacturers, supports the market's growth in North America. Ongoing innovations in clean-label and sustainable release agent solutions further strengthen the region's leadership position.

Competitive Landscape and Leading Companies

The food release agents market is highly competitive, with major players such as AAK AB, Cargill Inc., Archer Daniels Midland (ADM), and Lonza Group AG leading the industry. These companies focus on innovation, offering sustainable, allergen-free, and plant-based solutions to meet evolving consumer demands.

Collaborations between ingredient suppliers and food manufacturers are common, aimed at developing customized solutions for specific applications. With the growing focus on transparency and clean-label products, market players are investing in research and development to enhance the functionality and eco-friendliness of their offerings, ensuring sustained market growth.

Recent Developments:

- Archer Daniels Midland Company launched a new line of non-GMO food release agents tailored for bakery applications, improving adhesion and texture.

- Cargill, Incorporated acquired a regional food processing company to expand its footprint in food release solutions, enhancing its global portfolio.

- Kerry Group introduced a plant-based food release agent designed for vegan and allergen-free applications, catering to growing consumer demand.

- Dow Inc. announced a strategic partnership with a bakery equipment manufacturer to develop integrated release agent systems for industrial baking.

- AAK AB unveiled a sustainable food release product line using renewable vegetable oils to reduce environmental impact.

List of Leading Companies:

- AAK AB

- Archer Daniels Midland Company

- Avatar Corporation

- Cargill, Incorporated

- Corbion NV

- Dow Inc.

- DuPont de Nemours, Inc.

- Kerry Group

- Mallet & Company, Inc.

- Masterol Foods Pty Ltd

- MÜNZING Chemie GmbH

- Par-Way Tryson Company

- Puratos Group

- Sonneveld Group BV

- Zeelandia International BV

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 1.4 Billion |

|

Forecasted Value (2030) |

USD 2.2 Billion |

|

CAGR (2024 – 2030) |

7.0% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Food Release Agents Market by Type (Liquid Release Agents, Solid Release Agents), by Ingredient Type (Vegetable Oils, Waxes, Lecithin), by Application (Bakery and Confectionery, Processed Foods, Meat and Poultry Products), by End-User Industry (Food Manufacturers, Food Service Providers) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

AAK AB, Archer Daniels Midland Company, Avatar Corporation, Cargill, Incorporated, Corbion NV, Dow Inc., Kerry Group, Mallet & Company, Inc., Masterol Foods Pty Ltd, MÜNZING Chemie GmbH, Par-Way Tryson Company, Puratos Group, Zeelandia International BV |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Food Release Agents Market, by Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Liquid Release Agents |

|

4.2. Solid Release Agents |

|

5. Food Release Agents Market, by Ingredient Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Vegetable Oils |

|

5.2. Waxes |

|

5.3. Lecithin |

|

5.4. Others |

|

6. Food Release Agents Market, by Application (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Bakery and Confectionery |

|

6.2. Processed Foods |

|

6.3. Meat and Poultry Products |

|

6.4. Others |

|

7. Food Release Agents Market, by End-User Industry (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Food Manufacturers |

|

7.2. Food Service Providers |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Food Release Agents Market, by Type |

|

8.2.7. North America Food Release Agents Market, by Ingredient Type |

|

8.2.8. North America Food Release Agents Market, by Application |

|

8.2.9. North America Food Release Agents Market, by End-User Industry |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Food Release Agents Market, by Type |

|

8.2.10.1.2. US Food Release Agents Market, by Ingredient Type |

|

8.2.10.1.3. US Food Release Agents Market, by Application |

|

8.2.10.1.4. US Food Release Agents Market, by End-User Industry |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. AAK AB |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Archer Daniels Midland Company |

|

10.3. Avatar Corporation |

|

10.4. Cargill, Incorporated |

|

10.5. Corbion NV |

|

10.6. Dow Inc. |

|

10.7. DuPont de Nemours, Inc. |

|

10.8. Kerry Group |

|

10.9. Mallet & Company, Inc. |

|

10.10. Masterol Foods Pty Ltd |

|

10.11. MÜNZING Chemie GmbH |

|

10.12. Par-Way Tryson Company |

|

10.13. Puratos Group |

|

10.14. Sonneveld Group BV |

|

10.15. Zeelandia International BV |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Food Release Agents Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Food Release Agents Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Food Release Agents Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA