As per Intent Market Research, the Flush Mounted Low Voltage Distribution Panel Market was valued at USD 5.3 billion in 2023 and will surpass USD 8.1 billion by 2030; growing at a CAGR of 6.3% during 2024 - 2030.

The flush mounted low voltage distribution panel market is witnessing significant growth as demand for efficient, space-saving, and reliable power distribution systems increases across residential, commercial, and industrial sectors. These panels are critical in distributing electrical power, managing circuit loads, and ensuring protection against electrical faults. Flush mounted panels, which are installed directly into walls, offer a sleek, space-efficient solution while maintaining the necessary functionality for power management. They are widely used in both new construction and renovation projects, particularly in urban areas where maximizing space is a key consideration.

As the global push for sustainable and energy-efficient building solutions accelerates, flush mounted low voltage distribution panels are being increasingly adopted. These panels are integral to modern electrical systems, providing solutions for power distribution, circuit protection, and control systems in diverse environments. This demand is driven by rising electricity consumption, urbanization, and the continued expansion of residential, commercial, and industrial infrastructures, necessitating advanced and efficient power distribution solutions.

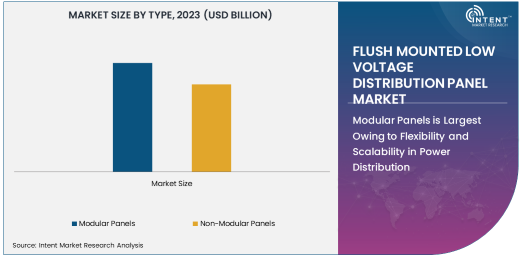

Modular Panels is Largest Owing to Flexibility and Scalability in Power Distribution

Modular panels represent the largest segment within the flush mounted low voltage distribution panel market due to their flexibility and scalability in handling electrical systems of varying sizes and complexity. Modular panels are highly customizable, allowing users to adjust and expand the configuration based on specific power distribution needs. This adaptability makes them ideal for commercial and industrial applications, where power requirements can change over time or need to be distributed across large areas with multiple circuits.

In industrial and commercial sectors, modular panels are essential as they provide the ability to manage large-scale electrical systems efficiently while maintaining flexibility in design. The growing trend of automation and smart infrastructure in these sectors is driving the need for modular distribution panels that can accommodate the integration of advanced technologies. Additionally, their scalability ensures that businesses can expand their power distribution systems as their energy needs grow, making modular panels the preferred choice in the market.

Wall-Mounted Panels is Largest Installation Type Owing to Space-Saving Features

Wall-mounted installation remains the largest installation type in the flush mounted low voltage distribution panel market due to its space-saving design and ease of installation. These panels are mounted directly onto the wall, offering a clean and streamlined look while minimizing the use of floor space, which is especially important in residential, commercial, and industrial buildings where maximizing usable space is a priority. The flush-mounted design ensures that the distribution panels are hidden from view, contributing to the aesthetic value of the building.

In addition to their aesthetic appeal, wall-mounted flush panels are highly functional, providing easy access for maintenance and repair. This makes them particularly suitable for high-traffic environments, such as commercial buildings, offices, and industrial facilities. As urbanization increases and space in residential and commercial buildings becomes more limited, the demand for wall-mounted flush panels is expected to continue to rise. Their compact design and practical benefits make them the most popular installation type in the market.

Below 400V Voltage Rating is Largest Owing to Broad Adoption in Residential and Commercial Sectors

The below 400V voltage rating segment holds the largest share in the flush mounted low voltage distribution panel market, primarily due to its widespread use in residential and commercial applications. Panels with a voltage rating below 400V are typically used in smaller, low-power applications, including lighting systems, appliances, and basic electrical systems in homes, apartments, and small offices. These panels provide essential power distribution and circuit protection while ensuring safety and compliance with electrical regulations.

The continued growth of residential and commercial construction, coupled with the increasing demand for efficient and safe electrical systems, drives the demand for low-voltage distribution panels below 400V. In addition, as buildings become smarter and energy-efficient technologies are integrated, the need for reliable and safe low-voltage systems remains critical, contributing to the market's growth. The segment's dominance is expected to continue as smart homes and energy-efficient buildings become more prevalent across regions.

Power Distribution is Largest Application Owing to Need for Efficient Energy Management

The power distribution application is the largest segment in the flush mounted low voltage distribution panel market, driven by the growing need for efficient management and control of electrical energy across residential, commercial, and industrial buildings. Power distribution panels play a crucial role in ensuring that electricity is safely and efficiently delivered to various parts of a building or facility, protecting circuits and electrical components from overloads and faults. As energy demand continues to rise globally, the need for efficient power distribution systems has become increasingly important.

In addition to traditional power distribution, modern power distribution panels also facilitate the integration of renewable energy sources, such as solar power, into the electrical grid. This trend, along with the growing emphasis on energy efficiency and sustainability, is driving the demand for advanced power distribution systems. The flush mounted low voltage distribution panel’s ability to manage multiple electrical circuits, protect against power surges, and support smart building technologies makes it essential for efficient power management in various applications.

Industrial is Largest End-User Industry Owing to High Power Requirements

The industrial end-user industry is the largest segment in the flush mounted low voltage distribution panel market, driven by the high power requirements of industrial applications. Industries such as manufacturing, oil and gas, chemical processing, and mining rely on robust and efficient power distribution systems to run heavy machinery, production lines, and industrial operations. Flush mounted low voltage distribution panels are integral to managing the complex electrical networks in these settings, ensuring safe and reliable power distribution while minimizing downtime and reducing operational risks.

As industries continue to expand and adopt more energy-intensive technologies, the need for advanced power distribution systems in industrial settings will grow. These panels not only provide essential power management but also support automation, data integration, and energy optimization, which are critical in modern industrial operations. This trend is expected to drive the continuous growth of the industrial segment within the market.

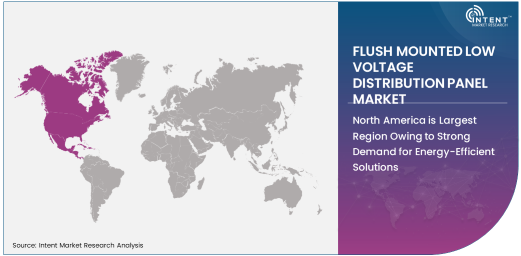

North America is Largest Region Owing to Strong Demand for Energy-Efficient Solutions

North America holds the largest market share in the flush mounted low voltage distribution panel market, driven by the region’s well-established infrastructure and high demand for energy-efficient electrical systems. The United States and Canada, in particular, are seeing significant investments in construction, commercial development, and industrial expansion, all of which require reliable and efficient power distribution systems. The increasing trend toward smart buildings, automation, and renewable energy integration in the region is further fueling the demand for flush mounted low voltage distribution panels.

North America is also home to several leading manufacturers and has stringent safety standards and regulations for electrical installations, which bolsters the adoption of high-quality, reliable distribution panels. As the focus on energy efficiency and sustainability intensifies, North America is expected to maintain its dominance in the global flush mounted low voltage distribution panel market.

Competitive Landscape and Leading Companies

The flush mounted low voltage distribution panel market is highly competitive, with several key players offering innovative and efficient solutions to meet the growing demand across various industries. Leading companies in the market include Schneider Electric, Siemens AG, Eaton Corporation, ABB Ltd., and General Electric. These companies focus on product innovation, technological advancements, and expanding their product offerings to cater to the evolving needs of industries such as construction, residential, and industrial.

The competitive landscape is marked by a strong emphasis on energy-efficient solutions, sustainability, and smart grid technologies. Companies are integrating IoT capabilities, advanced control systems, and automation features into their distribution panels to enhance functionality and improve energy management. Strategic collaborations, acquisitions, and mergers are common in the market as companies seek to expand their market presence and offer integrated electrical solutions. The market is expected to remain competitive, with increased focus on customization, energy efficiency, and regulatory compliance.

Recent Developments:

- Schneider Electric has launched an innovative range of flush-mounted low voltage distribution panels featuring smart monitoring capabilities, aimed at improving energy efficiency in commercial buildings.

- Siemens AG announced the expansion of its flush-mounted low voltage distribution panel portfolio to meet the growing demand for smart home integration and enhanced electrical safety.

- Eaton Corporation revealed a new product line of energy-efficient low voltage distribution panels designed for industrial applications, focusing on reducing energy consumption and improving power management.

- ABB Ltd. partnered with a leading construction company to provide custom flush-mounted low voltage distribution panels for a large-scale residential project, enhancing energy efficiency and safety.

- Legrand introduced a series of modular flush-mounted electrical panels for commercial buildings, featuring integrated circuit protection and IoT-enabled monitoring for smarter electrical management.

List of Leading Companies:

- Schneider Electric

- Siemens AG

- Eaton Corporation

- ABB Ltd.

- Legrand

- Honeywell International Inc.

- General Electric

- Mitsubishi Electric

- Larsen & Toubro Limited

- C&S Electric Limited

- Hager Group

- Chint Group

- Cameco

- C&S Electric

- Rockwell Automation, Inc.

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 5.3 Billion |

|

Forecasted Value (2030) |

USD 8.1 Billion |

|

CAGR (2024 – 2030) |

6.3% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Flush Mounted Low Voltage Distribution Panel Market by Type (Modular Panels, Non-Modular Panels), by Installation Type (Wall-Mounted, Flush-Mounted), by Voltage Rating (Below 400V, 400V-800V), by Application (Power Distribution, Circuit Protection, Control Systems), by End-Use Industry (Residential, Commercial, Industrial) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Schneider Electric, Siemens AG, Eaton Corporation, ABB Ltd., Legrand, Honeywell International Inc., Mitsubishi Electric, Larsen & Toubro Limited, C&S Electric Limited, Hager Group, Chint Group, Cameco, Rockwell Automation, Inc. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Flush Mounted Low Voltage Distribution Panel Market, by Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Modular Panels |

|

4.2. Non-Modular Panels |

|

5. Flush Mounted Low Voltage Distribution Panel Market, by Installation Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Wall-Mounted |

|

5.2. Flush-Mounted |

|

6. Flush Mounted Low Voltage Distribution Panel Market, by Voltage Rating (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Below 400V |

|

6.2. 400V-800V |

|

7. Flush Mounted Low Voltage Distribution Panel Market, by Application (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Power Distribution |

|

7.2. Circuit Protection |

|

7.3. Control Systems |

|

8. Flush Mounted Low Voltage Distribution Panel Market, by End-User Industry (Market Size & Forecast: USD Million, 2022 – 2030) |

|

8.1. Residential |

|

8.2. Commercial |

|

8.3. Industrial |

|

9. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

9.1. Regional Overview |

|

9.2. North America |

|

9.2.1. Regional Trends & Growth Drivers |

|

9.2.2. Barriers & Challenges |

|

9.2.3. Opportunities |

|

9.2.4. Factor Impact Analysis |

|

9.2.5. Technology Trends |

|

9.2.6. North America Flush Mounted Low Voltage Distribution Panel Market, by Type |

|

9.2.7. North America Flush Mounted Low Voltage Distribution Panel Market, by Installation Type |

|

9.2.8. North America Flush Mounted Low Voltage Distribution Panel Market, by Voltage Rating |

|

9.2.9. North America Flush Mounted Low Voltage Distribution Panel Market, by Application |

|

9.2.10. North America Flush Mounted Low Voltage Distribution Panel Market, by End-User Industry |

|

9.2.11. By Country |

|

9.2.11.1. US |

|

9.2.11.1.1. US Flush Mounted Low Voltage Distribution Panel Market, by Type |

|

9.2.11.1.2. US Flush Mounted Low Voltage Distribution Panel Market, by Installation Type |

|

9.2.11.1.3. US Flush Mounted Low Voltage Distribution Panel Market, by Voltage Rating |

|

9.2.11.1.4. US Flush Mounted Low Voltage Distribution Panel Market, by Application |

|

9.2.11.1.5. US Flush Mounted Low Voltage Distribution Panel Market, by End-User Industry |

|

9.2.11.2. Canada |

|

9.2.11.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

9.3. Europe |

|

9.4. Asia-Pacific |

|

9.5. Latin America |

|

9.6. Middle East & Africa |

|

10. Competitive Landscape |

|

10.1. Overview of the Key Players |

|

10.2. Competitive Ecosystem |

|

10.2.1. Level of Fragmentation |

|

10.2.2. Market Consolidation |

|

10.2.3. Product Innovation |

|

10.3. Company Share Analysis |

|

10.4. Company Benchmarking Matrix |

|

10.4.1. Strategic Overview |

|

10.4.2. Product Innovations |

|

10.5. Start-up Ecosystem |

|

10.6. Strategic Competitive Insights/ Customer Imperatives |

|

10.7. ESG Matrix/ Sustainability Matrix |

|

10.8. Manufacturing Network |

|

10.8.1. Locations |

|

10.8.2. Supply Chain and Logistics |

|

10.8.3. Product Flexibility/Customization |

|

10.8.4. Digital Transformation and Connectivity |

|

10.8.5. Environmental and Regulatory Compliance |

|

10.9. Technology Readiness Level Matrix |

|

10.10. Technology Maturity Curve |

|

10.11. Buying Criteria |

|

11. Company Profiles |

|

11.1. Schneider Electric |

|

11.1.1. Company Overview |

|

11.1.2. Company Financials |

|

11.1.3. Product/Service Portfolio |

|

11.1.4. Recent Developments |

|

11.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

11.2. Siemens AG |

|

11.3. Eaton Corporation |

|

11.4. ABB Ltd. |

|

11.5. Legrand |

|

11.6. Honeywell International Inc. |

|

11.7. General Electric |

|

11.8. Mitsubishi Electric |

|

11.9. Larsen & Toubro Limited |

|

11.10. C&S Electric Limited |

|

11.11. Hager Group |

|

11.12. Chint Group |

|

11.13. Cameco |

|

11.14. C&S Electric |

|

11.15. Rockwell Automation, Inc. |

|

12. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Flush Mounted Low Voltage Distribution Panel Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Flush Mounted Low Voltage Distribution Panel Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Flush Mounted Low Voltage Distribution Panel Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA