As per Intent Market Research, the Floor Coatings Market was valued at USD 3.8 billion in 2023 and will surpass USD 17.0 billion by 2030; growing at a CAGR of 23.9% during 2024 - 2030.

The floor coatings market is experiencing significant growth, driven by increasing demand for durable, aesthetic, and easy-to-maintain flooring solutions across various sectors. Floor coatings are critical for protecting surfaces from wear, corrosion, and chemical damage while enhancing the visual appeal of floors. Industries such as manufacturing, healthcare, food & beverage, and aviation are increasingly adopting advanced floor coatings to meet safety standards and operational efficiency. The market is witnessing innovations in coating technologies to meet the rising demand for environmentally friendly and high-performance products.

The growth of the market is further supported by rising construction activities in residential, commercial, and industrial sectors worldwide. Rapid industrialization, stringent safety regulations, and increased investments in infrastructure development are driving the adoption of floor coatings. As end-use industries emphasize productivity, safety, and aesthetics, the floor coatings market is expected to grow steadily over the forecast period.

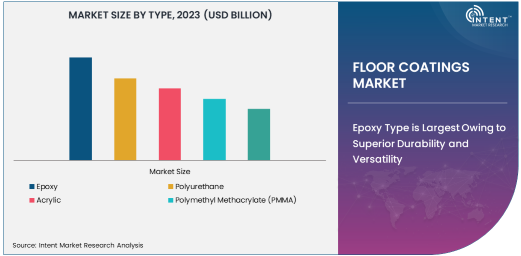

Epoxy Type is Largest Owing to Superior Durability and Versatility

The epoxy segment is the largest in the floor coatings market, primarily due to its superior durability, chemical resistance, and cost-effectiveness. Epoxy coatings are widely used across industrial, commercial, and residential applications for their ability to provide a strong, protective layer that withstands heavy loads, abrasions, and harsh chemicals. These coatings are particularly popular in manufacturing facilities, warehouses, and garages, where robust floor protection is essential.

Epoxy floor coatings are also versatile and customizable, with options for anti-slip, anti-static, and decorative finishes. The ease of application and low maintenance requirements further enhance their popularity across various industries. Growing industrialization and the demand for high-performance flooring solutions are driving the adoption of epoxy coatings globally. With advancements in technology, eco-friendly epoxy coatings with reduced volatile organic compounds (VOCs) are also gaining traction, supporting market growth.

Double Component Segment is Largest Owing to High Performance and Durability

The double component segment dominates the floor coatings market due to its ability to deliver enhanced durability, performance, and resistance to wear and tear. Double component coatings, typically composed of resin and hardener, offer superior adhesion, chemical resistance, and mechanical strength compared to single-component systems. This makes them ideal for industrial and commercial applications where floors are subjected to heavy traffic, chemicals, and extreme conditions.

Industries such as manufacturing, aviation, and healthcare prefer double component floor coatings for their ability to create long-lasting and robust surfaces. These coatings are particularly favored for areas requiring stringent hygiene and safety standards, such as food & beverage processing plants and healthcare facilities. The segment’s growth is further supported by innovations in formulation technology, which are enhancing curing times, durability, and environmental compatibility.

Industrial Application is Largest Owing to High Demand for Durable and Resistant Flooring

The industrial segment holds the largest share in the floor coatings market, driven by the need for durable, chemical-resistant, and easy-to-clean flooring solutions in industrial settings. Industries such as manufacturing, chemical processing, and automotive require high-performance coatings to protect floors from heavy machinery loads, chemical spills, and abrasion. Floor coatings in industrial facilities also help improve safety by providing anti-slip surfaces and enhancing visibility through color-coded coatings.

The increasing pace of industrialization and infrastructure development worldwide is fueling demand for floor coatings in the industrial sector. As industries focus on enhancing operational efficiency and meeting safety regulations, the adoption of advanced floor coatings is expected to rise. The segment’s growth is further supported by the growing trend of sustainable and eco-friendly coatings that offer performance benefits without compromising environmental standards.

Manufacturing End-Use Industry is Largest Owing to Rising Industrialization and Safety Requirements

The manufacturing segment is the largest end-use industry in the floor coatings market, primarily driven by the rapid growth of industrial facilities worldwide. Manufacturing plants require floor coatings that can withstand heavy traffic, chemical exposure, and mechanical impacts while maintaining safety and hygiene standards. Epoxy and polyurethane coatings are particularly favored in manufacturing environments for their durability, chemical resistance, and low maintenance requirements.

As industries prioritize workplace safety and operational efficiency, the demand for floor coatings that meet strict safety and regulatory standards is increasing. Additionally, manufacturers are adopting coatings with anti-static and anti-slip properties to reduce the risk of accidents and equipment damage. The rising investments in manufacturing infrastructure, particularly in emerging economies, are further fueling the growth of this segment.

Asia-Pacific is the Fastest Growing Region Owing to Infrastructure Development and Industrialization

The Asia-Pacific region is the fastest growing in the floor coatings market, driven by rapid industrialization, urbanization, and infrastructure development in countries like China, India, and Southeast Asia. The region’s growing manufacturing sector, increasing construction activities, and expanding commercial spaces are driving the demand for advanced floor coatings. Rising investments in industrial infrastructure, coupled with government initiatives to support smart cities and urban development, are further propelling market growth.

The Asia-Pacific market is also witnessing increasing adoption of eco-friendly and high-performance coatings due to rising environmental awareness and regulatory pressure. With a booming population, rapid economic growth, and increasing demand for durable and cost-effective flooring solutions, the region is expected to continue its dominance in the global floor coatings market in the coming years.

Competitive Landscape and Leading Companies

The floor coatings market is highly competitive, with key players focusing on innovation, product differentiation, and expansion into emerging markets. Leading companies in the market include PPG Industries, Sherwin-Williams, BASF SE, AkzoNobel N.V., and RPM International, among others. These companies are investing in research and development to introduce advanced, sustainable, and VOC-free coatings that align with evolving environmental regulations.

Strategic partnerships, acquisitions, and product launches are common strategies employed by market leaders to strengthen their market position. The growing demand for specialized coatings in industrial, commercial, and residential applications is prompting companies to offer customized solutions that cater to specific end-user requirements. As the market continues to evolve, innovation and sustainability will remain key focus areas for companies to gain a competitive edge.

Recent Developments:

- Sherwin-Williams launched a sustainable low-VOC epoxy coating for industrial and commercial applications.

- PPG Industries announced a new production line to increase its manufacturing capacity of epoxy and polyurethane coatings.

- BASF launched a high-performance industrial floor coating system designed for heavy-duty manufacturing environments.

- Sika AG completed the acquisition of MBCC Group, enhancing its market position in high-performance floor coating solutions.

- Jotun opened a state-of-the-art production facility in Asia to meet growing regional demand for decorative and industrial floor coatings.

List of Leading Companies:

- PPG Industries, Inc.

- Sherwin-Williams Company

- Akzo Nobel N.V.

- BASF SE

- RPM International Inc.

- Axalta Coating Systems

- Nippon Paint Holdings Co., Ltd.

- Sika AG

- Jotun Group

- Kansai Paint Co., Ltd.

- Behr Process Corporation

- Hempel A/S

- Tikkurila Oyj

- Teknos Group

- Berger Paints

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 3.8 Billion |

|

Forecasted Value (2030) |

USD 17.0 Billion |

|

CAGR (2024 – 2030) |

23.9% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Floor Coatings Market by Type (Epoxy, Polyurethane, Acrylic, Polymethyl Methacrylate (PMMA), Others), by Component (Single Component, Double Component, Multi-Component), by Application (Residential, Commercial, Industrial, Institutional), by End-Use Industry (Manufacturing, Aviation & Transportation, Food & Beverage, Healthcare, Others) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

PPG Industries, Inc., Sherwin-Williams Company, Akzo Nobel N.V., BASF SE, RPM International Inc., Axalta Coating Systems, Sika AG, Jotun Group, Kansai Paint Co., Ltd., Behr Process Corporation, Hempel A/S, Tikkurila Oyj and Berger Paints |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Floor Coatings Market, by Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Epoxy |

|

4.2. Polyurethane |

|

4.3. Acrylic |

|

4.4. Polymethyl Methacrylate (PMMA) |

|

4.5. Others |

|

5. Floor Coatings Market, by Component (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Single Component |

|

5.2. Double Component |

|

5.3. Multi-Component |

|

6. Floor Coatings Market, by Application (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Residential |

|

6.2. Commercial |

|

6.3. Industrial |

|

6.4. Institutional |

|

7. Floor Coatings Market, by End-Use Industry (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Manufacturing |

|

7.2. Aviation & Transportation |

|

7.3. Food & Beverage |

|

7.4. Healthcare |

|

7.5. Others |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Floor Coatings Market, by Type |

|

8.2.7. North America Floor Coatings Market, by Component |

|

8.2.8. North America Floor Coatings Market, by Application |

|

8.2.9. North America Floor Coatings Market, by End-Use Industry |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Floor Coatings Market, by Type |

|

8.2.10.1.2. US Floor Coatings Market, by Component |

|

8.2.10.1.3. US Floor Coatings Market, by Application |

|

8.2.10.1.4. US Floor Coatings Market, by End-Use Industry |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. PPG Industries, Inc. |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Sherwin-Williams Company |

|

10.3. Akzo Nobel N.V. |

|

10.4. BASF SE |

|

10.5. RPM International Inc. |

|

10.6. Axalta Coating Systems |

|

10.7. Nippon Paint Holdings Co., Ltd. |

|

10.8. Sika AG |

|

10.9. Jotun Group |

|

10.10. Kansai Paint Co., Ltd. |

|

10.11. Behr Process Corporation |

|

10.12. Hempel A/S |

|

10.13. Tikkurila Oyj |

|

10.14. Teknos Group |

|

10.15. Berger Paints |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Floor Coatings Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Floor Coatings Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Floor Coatings Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA