As per Intent Market Research, the Flight Data Monitoring and Analysis Market was valued at USD 2.6 billion in 2023 and will surpass USD 7.1 billion by 2030; growing at a CAGR of 15.6% during 2024 - 2030.

The flight data monitoring and analysis market plays a pivotal role in enhancing aviation safety, optimizing operational performance, and ensuring regulatory compliance. With the increasing complexity of air traffic, airlines and aviation authorities rely heavily on flight data monitoring systems to provide real-time and post-flight analysis for better decision-making. This technology enables the tracking of critical flight data, such as altitude, speed, engine performance, and flight path, which is crucial for improving flight safety, reducing operational costs, and complying with stringent aviation regulations.

The market for flight data monitoring and analysis is witnessing significant growth due to increasing air traffic, the adoption of advanced data analytics technologies, and the ongoing emphasis on enhancing flight safety. Regulatory requirements are also contributing to the market’s expansion, as authorities worldwide push for more stringent monitoring of flight data to ensure safety standards are met. Furthermore, the growing trend of data-driven insights for operational optimization is propelling the demand for both real-time and post-flight monitoring systems across different aviation sectors.

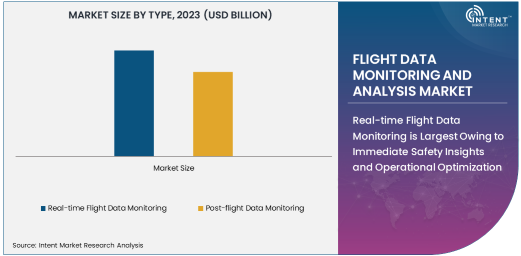

Real-time Flight Data Monitoring is Largest Owing to Immediate Safety Insights and Operational Optimization

Real-time flight data monitoring is the largest segment in the flight data monitoring and analysis market. This is due to the critical need for instant access to flight data during operations to ensure immediate safety alerts, maintenance alerts, and operational adjustments. Real-time data monitoring systems continuously track aircraft performance, enabling ground crews and flight crews to respond quickly to any irregularities or technical issues during flight. This ability to make on-the-spot decisions enhances safety and minimizes risks associated with aviation.

The growing focus on flight safety monitoring is a key driver for the prominence of real-time monitoring solutions. These systems help detect potential safety hazards in real time, thereby improving the response time for critical interventions. Moreover, real-time monitoring systems provide continuous data streams that are used for operational performance optimization, allowing airlines to make adjustments that improve fuel efficiency, reduce costs, and enhance overall fleet management. As a result, real-time flight data monitoring is expected to continue dominating the market in the coming years.

Cloud-based Deployment Mode is Fastest Growing Due to Scalability and Cost Efficiency

The cloud-based deployment mode is the fastest-growing segment in the flight data monitoring and analysis market. Cloud solutions offer enhanced scalability, cost efficiency, and easy access to data for aviation organizations. Unlike on-premises systems, cloud-based platforms allow airlines and aviation authorities to store, analyze, and access vast amounts of flight data remotely, facilitating better collaboration and decision-making across geographically dispersed teams.

As cloud-based solutions offer flexibility and the ability to scale operations with ease, they are increasingly preferred by airlines seeking to optimize their operations while keeping infrastructure costs low. Moreover, cloud platforms enable the integration of advanced data analytics and artificial intelligence tools, allowing for predictive maintenance, performance optimization, and better decision-making. The growing adoption of cloud technologies within the aviation sector is expected to further fuel the growth of this deployment mode.

Flight Safety Monitoring Application is Largest Due to Regulatory Pressures and Focus on Safety

Flight safety monitoring is the largest application segment in the flight data monitoring and analysis market. Safety is paramount in aviation, and the continuous monitoring of flight data to detect potential risks and hazards is critical for ensuring the safety of passengers and crew members. Flight safety monitoring systems track critical parameters like speed, altitude, engine performance, and system health, providing real-time alerts and post-flight analysis to identify potential safety threats.

The increasing number of air travel passengers and the growing focus on regulatory compliance and safety protocols are driving the demand for advanced flight safety monitoring systems. Regulatory agencies worldwide are setting higher standards for data collection and analysis to prevent accidents and enhance overall aviation safety. As the aviation industry continues to prioritize safety and as regulations become stricter, the demand for flight safety monitoring solutions is expected to rise significantly in the coming years.

Commercial Aviation End-User is Largest Owing to Growing Air Traffic and Safety Concerns

The commercial aviation end-user segment represents the largest share of the flight data monitoring and analysis market. The continued growth in air travel worldwide, coupled with the increasing importance of safety and operational efficiency, has made commercial aviation a key driver of this market. Airlines rely on flight data monitoring systems to ensure safety compliance, optimize fuel consumption, and enhance overall operational performance.

The increasing number of commercial flights, especially in emerging economies, is contributing to the need for more advanced data monitoring systems to manage flight operations more efficiently. Additionally, airlines are focusing on data analytics to optimize their fleet management, reduce delays, and minimize operational costs. As commercial aviation remains the dominant sector in the global air travel industry, the demand for flight data monitoring systems tailored to this segment is expected to maintain strong growth throughout the forecast period.

North America is Largest Region Owing to Technological Advancements and Robust Aviation Infrastructure

North America is the largest region in the flight data monitoring and analysis market, driven by its advanced aviation infrastructure, strong presence of key market players, and ongoing technological advancements. The United States, as the home of major airlines and aviation companies, has been a leader in adopting advanced flight data monitoring technologies. Regulatory bodies, such as the Federal Aviation Administration (FAA), have implemented stringent regulations that encourage the use of data monitoring systems to ensure flight safety.

Additionally, North American airlines are at the forefront of leveraging cloud-based solutions, artificial intelligence, and predictive analytics to optimize operations and improve safety. As air travel continues to increase and new technologies are adopted, the North American market is expected to maintain its leadership position in the global flight data monitoring and analysis market.

Competitive Landscape and Leading Companies

The flight data monitoring and analysis market is highly competitive, with major players such as Honeywell International Inc., Thales Group, Collins Aerospace, General Electric Company, and L3 Technologies dominating the market. These companies are investing heavily in research and development to introduce innovative solutions that improve flight safety, operational efficiency, and regulatory compliance. Partnerships, acquisitions, and collaborations with airline operators and aviation authorities are common strategies employed by these companies to expand their market presence and enhance their product offerings.

The competitive landscape is evolving as companies focus on cloud-based platforms, artificial intelligence, and predictive analytics to offer more integrated and automated solutions. With a strong emphasis on improving aviation safety, reducing operational costs, and meeting regulatory standards, the leading companies are well-positioned to maintain their dominance in the market. The shift toward more data-driven and AI-powered flight data monitoring systems is expected to define the next phase of growth in the aviation industry.

Recent Developments:

- Honeywell International Inc. recently announced the launch of its advanced flight data analysis solution for the aviation industry, focusing on safety and operational efficiency.

- Rockwell Collins (Collins Aerospace) has unveiled a new cloud-based flight data monitoring platform to enhance operational insights for airlines and aircraft operators.

- Thales Group expanded its flight data monitoring services, integrating advanced analytics to optimize real-time flight data processing and improve aviation safety.

- L3 Technologies entered into a strategic partnership with a leading airline to provide real-time flight data analysis solutions that enhance operational decision-making.

- GE Aviation announced the introduction of an innovative flight data analysis tool that utilizes machine learning algorithms for predictive maintenance and performance optimization.

List of Leading Companies:

- Honeywell International Inc.

- Rockwell Collins (Collins Aerospace)

- Thales Group

- L3 Technologies

- Garmin Ltd.

- FLIR Systems, Inc.

- Rada Electronics Industries Ltd.

- Sita Inc.

- FlightAware

- FDM Group

- GE Aviation

- AeroData, Inc.

- Ametek Inc.

- Teledyne Controls

- Indra Sistemas S.A.

Report Scope:

|

Report Features |

Description |

|

Market Size (2023) |

USD 2.6 Billion |

|

Forecasted Value (2030) |

USD 7.1 Billion |

|

CAGR (2024 – 2030) |

15.6% |

|

Base Year for Estimation |

2023 |

|

Historic Year |

2022 |

|

Forecast Period |

2024 – 2030 |

|

Report Coverage |

Market Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

|

Segments Covered |

Flight Data Monitoring and Analysis Market by Type (Real-time Flight Data Monitoring, Post-flight Data Monitoring), by Deployment Mode (Cloud-based, On-premises), by Application (Flight Safety Monitoring, Operational Performance Monitoring, Regulatory Compliance), by End-User (Commercial Aviation, Military Aviation, Cargo Airlines, General Aviation) |

|

Regional Analysis |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, Australia, India, and Rest of Asia-Pacific), Latin America (Brazil, Argentina, and Rest of Latin America), Middle East & Africa (Saudi Arabia, UAE, Rest of Middle East & Africa) |

|

Major Companies |

Honeywell International Inc., Rockwell Collins (Collins Aerospace), Thales Group, L3 Technologies, Garmin Ltd., FLIR Systems, Inc., Sita Inc., FlightAware, FDM Group, GE Aviation, AeroData, Inc., Ametek Inc., Indra Sistemas S.A. |

|

Customization Scope |

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements |

|

1. Introduction |

|

1.1. Market Definition |

|

1.2. Scope of the Study |

|

1.3. Research Assumptions |

|

1.4. Study Limitations |

|

2. Research Methodology |

|

2.1. Research Approach |

|

2.1.1. Top-Down Method |

|

2.1.2. Bottom-Up Method |

|

2.1.3. Factor Impact Analysis |

|

2.2. Insights & Data Collection Process |

|

2.2.1. Secondary Research |

|

2.2.2. Primary Research |

|

2.3. Data Mining Process |

|

2.3.1. Data Analysis |

|

2.3.2. Data Validation and Revalidation |

|

2.3.3. Data Triangulation |

|

3. Executive Summary |

|

3.1. Major Markets & Segments |

|

3.2. Highest Growing Regions and Respective Countries |

|

3.3. Impact of Growth Drivers & Inhibitors |

|

3.4. Regulatory Overview by Country |

|

4. Flight Data Monitoring and Analysis Market, by Type (Market Size & Forecast: USD Million, 2022 – 2030) |

|

4.1. Real-time Flight Data Monitoring |

|

4.2. Post-flight Data Monitoring |

|

5. Flight Data Monitoring and Analysis Market, by Deployment Mode (Market Size & Forecast: USD Million, 2022 – 2030) |

|

5.1. Cloud-based |

|

5.2. On-premises |

|

6. Flight Data Monitoring and Analysis Market, by Application (Market Size & Forecast: USD Million, 2022 – 2030) |

|

6.1. Flight Safety Monitoring |

|

6.2. Operational Performance Monitoring |

|

6.3. Regulatory Compliance |

|

7. Flight Data Monitoring and Analysis Market, by End-User (Market Size & Forecast: USD Million, 2022 – 2030) |

|

7.1. Commercial Aviation |

|

7.2. Military Aviation |

|

7.3. Cargo Airlines |

|

7.4. General Aviation |

|

8. Regional Analysis (Market Size & Forecast: USD Million, 2022 – 2030) |

|

8.1. Regional Overview |

|

8.2. North America |

|

8.2.1. Regional Trends & Growth Drivers |

|

8.2.2. Barriers & Challenges |

|

8.2.3. Opportunities |

|

8.2.4. Factor Impact Analysis |

|

8.2.5. Technology Trends |

|

8.2.6. North America Flight Data Monitoring and Analysis Market, by Type |

|

8.2.7. North America Flight Data Monitoring and Analysis Market, by Deployment Mode |

|

8.2.8. North America Flight Data Monitoring and Analysis Market, by Application |

|

8.2.9. North America Flight Data Monitoring and Analysis Market, by End-User |

|

8.2.10. By Country |

|

8.2.10.1. US |

|

8.2.10.1.1. US Flight Data Monitoring and Analysis Market, by Type |

|

8.2.10.1.2. US Flight Data Monitoring and Analysis Market, by Deployment Mode |

|

8.2.10.1.3. US Flight Data Monitoring and Analysis Market, by Application |

|

8.2.10.1.4. US Flight Data Monitoring and Analysis Market, by End-User |

|

8.2.10.2. Canada |

|

8.2.10.3. Mexico |

|

*Similar segmentation will be provided for each region and country |

|

8.3. Europe |

|

8.4. Asia-Pacific |

|

8.5. Latin America |

|

8.6. Middle East & Africa |

|

9. Competitive Landscape |

|

9.1. Overview of the Key Players |

|

9.2. Competitive Ecosystem |

|

9.2.1. Level of Fragmentation |

|

9.2.2. Market Consolidation |

|

9.2.3. Product Innovation |

|

9.3. Company Share Analysis |

|

9.4. Company Benchmarking Matrix |

|

9.4.1. Strategic Overview |

|

9.4.2. Product Innovations |

|

9.5. Start-up Ecosystem |

|

9.6. Strategic Competitive Insights/ Customer Imperatives |

|

9.7. ESG Matrix/ Sustainability Matrix |

|

9.8. Manufacturing Network |

|

9.8.1. Locations |

|

9.8.2. Supply Chain and Logistics |

|

9.8.3. Product Flexibility/Customization |

|

9.8.4. Digital Transformation and Connectivity |

|

9.8.5. Environmental and Regulatory Compliance |

|

9.9. Technology Readiness Level Matrix |

|

9.10. Technology Maturity Curve |

|

9.11. Buying Criteria |

|

10. Company Profiles |

|

10.1. Honeywell International Inc. |

|

10.1.1. Company Overview |

|

10.1.2. Company Financials |

|

10.1.3. Product/Service Portfolio |

|

10.1.4. Recent Developments |

|

10.1.5. IMR Analysis |

|

*Similar information will be provided for other companies |

|

10.2. Rockwell Collins (Collins Aerospace) |

|

10.3. Thales Group |

|

10.4. L3 Technologies |

|

10.5. Garmin Ltd. |

|

10.6. FLIR Systems, Inc. |

|

10.7. Rada Electronics Industries Ltd. |

|

10.8. Sita Inc. |

|

10.9. FlightAware |

|

10.10. FDM Group |

|

10.11. GE Aviation |

|

10.12. AeroData, Inc. |

|

10.13. Ametek Inc. |

|

10.14. Teledyne Controls |

|

10.15. Indra Sistemas S.A. |

|

11. Appendix |

A comprehensive market research approach was employed to gather and analyze data on the Flight Data Monitoring and Analysis Market. In the process, the analysis was also done to analyze the parent market and relevant adjacencies to measure the impact of them on the Flight Data Monitoring and Analysis Market. The research methodology encompassed both secondary and primary research techniques, ensuring the accuracy and credibility of the findings.

.jpg)

Secondary Research

Secondary research involved a thorough review of pertinent industry reports, journals, articles, and publications. Additionally, annual reports, press releases, and investor presentations of industry players were scrutinized to gain insights into their market positioning and strategies.

Primary Research

Primary research involved conducting in-depth interviews with industry experts, stakeholders, and market participants across the E-Waste Management ecosystem. The primary research objectives included:

- Validating findings and assumptions derived from secondary research

- Gathering qualitative and quantitative data on market trends, drivers, and challenges

- Understanding the demand-side dynamics, encompassing end-users, component manufacturers, facility providers, and service providers

- Assessing the supply-side landscape, including technological advancements and recent developments

Market Size Assessment

A combination of top-down and bottom-up approaches was utilized to analyze the overall size of the Flight Data Monitoring and Analysis Market. These methods were also employed to assess the size of various subsegments within the market. The market size assessment methodology encompassed the following steps:

- Identification of key industry players and relevant revenues through extensive secondary research

- Determination of the industry's supply chain and market size, in terms of value, through primary and secondary research processes

- Calculation of percentage shares, splits, and breakdowns using secondary sources and verification through primary sources

.jpg)

Data Triangulation

To ensure the accuracy and reliability of the market size, data triangulation was implemented. This involved cross-referencing data from various sources, including demand and supply side factors, market trends, and expert opinions. Additionally, top-down and bottom-up approaches were employed to validate the market size assessment.

NA